Bitcoin: a new economic system or a new religion?

fpoi.orgLast update: January 11, 2024

Index

Introduction

The title of this article is deliberately provocative, but the aim is precisely to make the reader reflect on how Bitcoin and almost all cryptocurrencies are much closer to a new religion than to a new payment and/or economic system, a new iteration of the Web (the Web3) and the various 'revolutionary' promises that are more or less explicitly present in whitepapers.

Technological aspects

CAP Theorem: is a theorem in theoretical computer science according to which any distributed computer system can only simultaneously provide two of the following three properties: consistency (C), availability (A) and partition tolerance (P). A blockchain is a distributed database without a central authority that is managed by N nodes using a consensus algorithm that establishes the validity of a block to be added to the chain. The consensus algorithm, Proof-of-Work (PoW) or Proof-of-Stake (PoS), determines partition tolerance, i.e. the ability to operate in the presence of inactive and/or malicious nodes. An attacker is able to attack the network and alter the blocks by controlling 51% of the computing power in the PoW (Nakamoto consensus), 51% of the stake in the PoS (Nakamoto consensus) or 67% of the stake in the PoS (BFT consensus), in this case 33% of the stake is needed to block the production of the blocks. According to the CAP theorem for a blockchain there is the consistency-availability dilemma; consistency is related to the finality of a valid block which can be probabilistic or absolute. In the first case, Nakamoto consensus, the deeper a transaction is in the chain, the less likely it is that there will be a change (the longer fork wins). In the second case, BFT consensus, a transaction is considered immediately final as soon as it is included in a block and added to the chain (there are no forks). AP blockchains are designed to operate under conditions of dynamic participation, favor liveness over safety and provide availability. CP blockchains are designed to operate in conditions of partial synchrony, favour safety over liveness and provide consistency. To improve availability, many CP blockchains include a slashing mechanism that penalises nodes with poor participation and performance. Categories, block and finality times for some popular blockchains:

- Bitcoin: PoW, AP, Nakamoto consensus, block time 10 minutes, finality time 60 minutes (6 confirmation blocks).

- Ethereum: PoS, AP, mixed consensus with BFT finality, block time 12 seconds, finality time 12-16 minutes (70-80 confirmation blocks).

- Solana: PoS, AP, mixed consensus with BFT finality, block time 0.4 seconds, finality time 6.4-12.8 seconds (16-32 confirmation blocks).

- Forkless blockchain: PoS, CP, BFT consensus, the block time (almost) coincides with the finality time. Some examples of this category are: Algorand with a block and finality time of 3.3 seconds and TON with a block time of 5 seconds and a finality time of 6 seconds.

Trilemma: the blockchain trilemma states that a blockchain is only capable of satisfying two of three properties simultaneously: scalability, decentralization and security. The trilemma was formulated by the founder of Ethereum, Vitalik Buterin, and is currently unsolved even though some blockchains claim otherwise.

Scalability: is the ability of a system to scale up or down according to need and availability. The scalability of a blockchain is measured by the number of transactions per second (TPS) and the finality time of a transaction. Scalability for some popular blockchains:

- Bitcoin: 7 TPS (10,000,000 TPS via off-chain Lightning Network), finality time 60 minutes.

- Ethereum: 20 TPS (100,000 TPS via off-chain rollups), finality time 12-16 minutes.

- Solana: 50,000 TPS (700,000 TPS), finality time 6.4-12.8 seconds.

- Algorand: 10,000 TPS (46,000 TPS), finality time 3.3 seconds.

- TON: 100,000 TPS (10,000,000 TPS), finality time 6 seconds.

Note: current payment systems such as VISA are able to process tens of thousands of transactions per second (65,000 TPS) and have a finality time in the order of seconds. Layer 2 such as Lightning Network or rollups allow to improve the scalability of the underlying blockchain by sacrificing decentralisation and security as they are off-chain protocols that require trust in centralised intermediaries (watchtower and sequencer).

Decentralisation: is the ability of the nodes of a distributed computer system to achieve a common goal without the need for a central authority. The decentralisation of a blockchain is measured by the Nakamoto's coefficient, i.e. the smallest number of independent entities that can act collectively to block the consensus, and thus quantifies its ability to resist censorship. In the PoW case this number is equal to 51% of the computing power of the miners while in the PoS case it is equal to 51% of the stake (Nakamoto consensus) or 33% of the stake (BFT consensus) of the validators. Decentralisation for some popular blockchains:

- Bitcoin: PoW, 50-60 miners and 2 mining pools. Minimum miner requirements: theoretical 1 H/s ~ 0,01 $, real 0.44-4.38 EH/s ~ 33.46-334.57 millions $ (this is an estimate as the distribution of computing power among miners is unknown).

- Ethereum: PoS with slashing, 10 validators and 2 staking pools. Minimum validator requirements: theoretical 32 coins ~ 82,144 $, real 443,552 coins ~ 1,138.60 millions $.

- Solana: PoS, 21 validators. Minimum validator requirements: theoretical 401.5 coins ~ 40,335 $, real 700,474 coins ~ 70.37 millions $.

- Algorand: PoS, 22 validators. Minimum validator requirements: theoretical 0.1 coins ~ 0.02 $, real 28,143,812 coins ~ 5.63 millions $.

- TON: PoS con slashing, 73 validators. Minimum validator requirements: theoretical 400,000 coins ~ 0.89 millions $, real 705,544 coins ~ 1.58 millions $.

Note: the actual minimum requirements represent the minimum amount of computing power for the miner (miner determining 51%) and stake for the validator (validator determining 51% or 67%) to be able to actively participate in the production of blocks. The feasibility of an attack on a blockchain depends mainly on the economic factor, i.e. the money needed to obtain 51% of the computing power or 51% or 33% of the stake. According to this research, it is economically more difficult to attack Bitcoin than almost all PoS blockchains; however, the majority of them implement slashing mechanisms that penalise even to the point of excluding from validation validators who act against the interests of the network from validation.

Security: is the set of means, technologies and procedures that aim to protect computer systems. The security of a blockchain depends on its fault or error tolerance and is related to Byzantine Fault Tolerance (BFT); it is the most important property of the three as it guarantees the integrity of the distributed ledger against various types of attacks (double spending, DoS, phishing, spam, Sybil, majority consensus, etc.). Blockchains are distributed computer systems designed according to the secure by design paradigm and based on open source software; however, they are not free of bugs and vulnerabilities like all existing software. Below are the most important attacks and known vulnerabilities for the most popular blockchains:

- Bitcoin: uptime 99.98% in 15 years, three problems: value overflow incident CVE-2010-5139 high level, critical inflation CVE-2018-17144 high level and chain split CVE-2013-3220 medium level. Security and privacy issues and several critical vulnerabilities for Lightning Network. CVE vulnerabilities according to the NIST NVD database: 1 critical level, 17 high level and 22 medium level.

- Ethereum: several major problems in over 8 years: The DAO fork 2016, DoS Attack 2016, chain split 2020, chain split CVE-2021-39137 high level and performance degradation 2023. CVE vulnerabilities according to the NIST NVD database: 2 critical level, 23 high level and 9 medium level.

- Solana: many downtimes and performance degradations in just 4 years, it is one of the least reliable blockchains. CVE vulnerability according to the NIST NVD database: 1 critical level.

- Algorand: 100% uptime in over 4 years. CVE vulnerabilities according to the NIST NVD database: no known vulnerabilities.

- TON: 100% uptime in over 4 years, performance degradation 2023. CVE vulnerabilities according to the NIST NVD database: no known vulnerabilities.

Note: Bitcoin has a smaller attack surface than other blockchains because it does not have a Turing-complete virtual machine to execute smart contracts. This makes it simpler and potentially more secure, but at the same time it lacks many of the features offered by other blockchains to realise the Web3. The severity of known vulnerabilities does not guarantee the presence or absence of future vulnerabilities, but it is a good indicator of the quality of design and implementation of a software.

Conclusion: the analysis of the technological aspects clearly shows that Bitcoin is not capable of realising a P2P electronic cash system as envisioned by the 2008 whitepaper. Bitcoin is a first-generation blockchain that has not received significant improvements during its history; Lightning Network is a layer 2 payment protocol proposed by a 2015 whitepaper with the aim of solving the scalability problem of the network provided that intermediaries and trust in their operations were reintroduced. However, after more than 8 years, it is still scarcely used and unable to solve any problems other than being insecure. Bitcoin is considered a secure and decentralised blockchain: the first aspect is confirmed by the data while the second is not as the PoW consensus is managed by 50-60 miners and the 'one CPU-one vote' principle in the whitepaper has been invalidated first by the use of GPUs and then ASICs and the emergence of mining farms.

{kind=link}

Economical aspects

Wealth distribution: is a comparison of the wealth of various members or groups in a society and shows an aspect of economic inequality or economic heterogeneity. The wealth distribution of a blockchain depends on the number of on-chain wallets (on the blockchain) and their balance; in particular, it is measured by the distribution of coins among the N richest wallets (rich list), which follows Zipf's law (Pareto distribution), and by the Gini coefficient. The distribution of wealth for some popular blockchains:

- Bitcoin: number of wallets ~ 52.54 M, top N wallet-% coins (10-5.56%, 50-11.16% and 100-13.99%). Gini coefficient: 0.466. Distribution via mining.

- Ethereum: number of wallets ~ 254.94 M, top N wallet-% coins (10-39.79%, 50-47.07% and 100-52.15%). Gini coefficient: 0.499. Distribution via ICO, mining and tokenomics.

- Solana: number of wallets ~ 9.15 M, top N wallet-% coins (10-9.69%, 50-24.93% and 100-33.41%). Gini coefficient: unknown. Distribution via ICO and tokenomics.

- Algorand: number of wallets ~ 37.85 M, top N wallet-% coins (10-21.44%, 50-43.18% and 100-61.00%). Gini coefficient: unknown. Distribution via ICO and tokenomics.

- TON: number of wallets ~ 1.17 M, top N wallet-% coins (10-62.67%, 50-87.51% and 100-95.44%). Gini coefficient: unknown. Distribution via mining and tokenomics.

Note: the number of wallets is not equivalent to the number of persons, natural or legal, as several wallets can belong to the same person. For instance, the alleged inventor of Bitcoin, Satoshi Nakamoto, owns approximately 1 M coins contained in about 20,000 wallets. Furthermore, intermediaries, such as exchanges or staking pools, are centralised entities that hold coins on behalf of people and require trust in the management of wealth. A fundamental aspect of PoS blockchain is the initial distribution of coins among the various entities of the network since it determines consensus. In theory the fairest distribution is via mining as anyone can participate according to the 'one CPU-one vote' principle, in practice mining is only accessible in the early stages before the arrival of mining farms. Finally, according to this research the wealth concentration of Bitcoin, the longest running blockchain with one of the best Gini coefficients, is significantly higher than the wealth distribution of the US population which is extremely centralised.

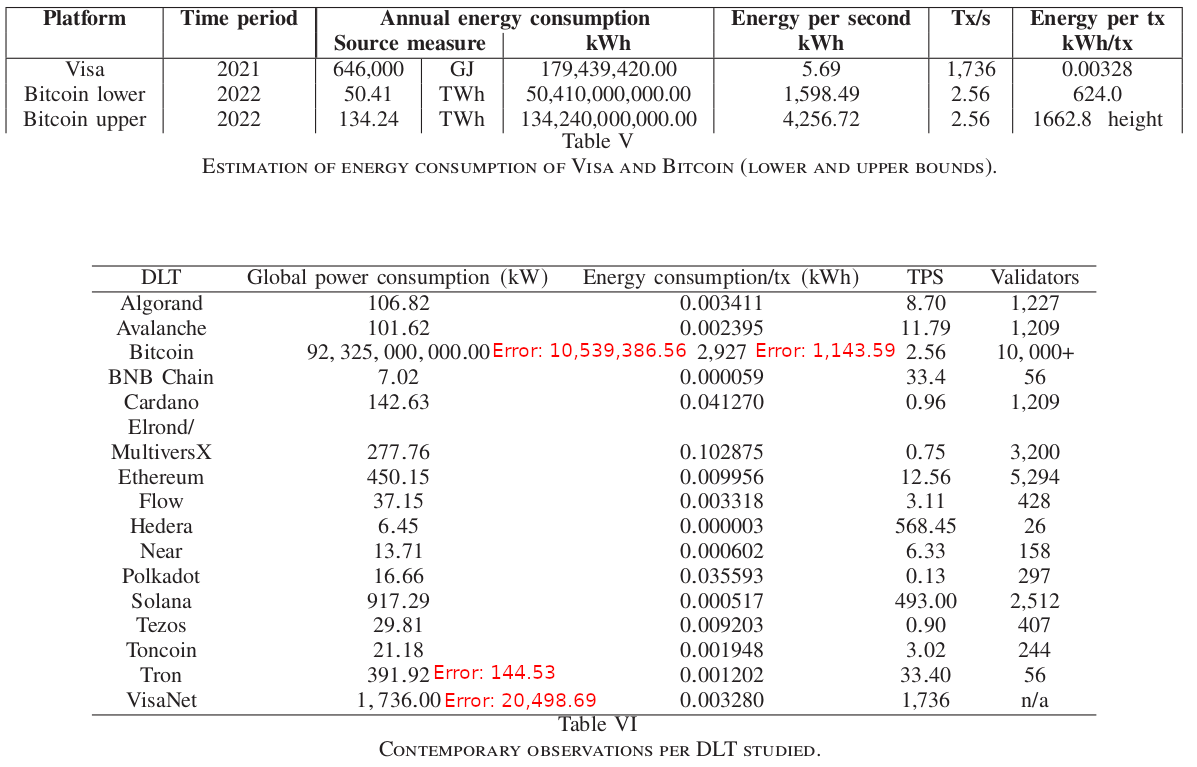

Resource utilisation: is the amount of natural resources used by a system to achieve a goal. The resource utilisation of a blockchain is measured by the efficiency of the consensus algorithm in terms of computing power used (CPU, GPU or ASIC, RAM and mass storage). In particular, resource utilisation depends on the amount of energy and hardware required to keep the blockchain running. The energy consumption and hardware usage (estimate) for some popular blockchains:

{kind=link}

- Bitcoin: global energy consumption 10,539,386.56 kWh, energy per transaction 1,143.59 kWh, hardware 5.37 million high-end ASICs.

- Ethereum: global energy consumption 450.15 kWh, energy per transaction 0.009956 kWh, hardware 896,688 low-end and mid-range servers.

- Solana: global energy consumption 917.29 kWh, energy per transaction 0.000517 kWh, hardware 1,988 high-end servers.

- Algorand: global energy consumption 106.82 kWh, energy per transaction 0.003411 kWh, hardware 1,193 mid-range servers.

- TON: global energy consumption 21.18 kWh, energy per transaction 0.001948 kWh, hardware 308 mid-range servers.

Note: current payment systems such as VISA have a global energy consumption of 20,498.69 kWh and an energy consumption per transaction of 0.003280 kWh. Blockchains whose PoW or PoS consensus algorithm has a probabilistic finality generate forks and waste energy in validating blocks of orphan chains. Furthermore, PoW blockchains, with a few exceptions, require high-end hardware (GPUs and ASICs) which has a high obsolescence rate and a short life cycle. According to this research, PoS blockchains have comparable or higher energy efficiency than the VISA payment system and negligible energy consumption compared to PoW blockchains (in line with other sources). Finally, the resources needed by a PoW blockchain to maintain consensus grow indefinitely over time and are independent of performance, i.e. the number of transactions processed; conversely, for a PoS blockchain, the resources needed to maintain consensus are limited and, in general, performance depends on them.

Functions of money: a money has four functions: medium of exchange, unit of account, standard of deferred payment and store of value. A fiat currency is a legal tender that is not backed by reserves of other materials (gold reserves) and therefore has no intrinsic value, which is determined by the strength of the state of the central bank that issues it. A cryptocurrency is a form of digital currency that uses blockchain technology and is also without backing and intrinsic value which is determined by the participants' trust in the network.

Medium of exchange: represents the transfer of a good or service in exchange for money with the aim of satisfying the needs of the parties involved. The possibility of using a blockchain as a payment system depends on the technological aspects of scalability and security and the economic aspect of transactions fees. The fees for some popular blockchains:

- Bitcoin: transactions fees for miners: average 0.00022 BTC ~ $ 10.04, maximum 0.001128 BTC ~ $ 62.78.

- Ethereum: variable transactions fees for validators: average 0.0039 ETH ~ $ 10.01, maximum 0.0708 ETH ~ $ 196.68.

- Solana: 50% of transactions fees for validators: average 0.000070761 SOL ~ $ 0.0071, maximum unknown.

- Algorand: transactions fees for validators: average 0.001 ALGO ~ $ 0.0001, maximum unknown.

- TON: 50% of transactions fees for validators: average 0.0055 TON ~ $ 0.0123, maximum unknown.

Note: current payment systems such as VISA have average transactions fees of 2.24%. The economic sustainability of a blockchain depends on transactions fees, which not only reward miners and validators, but also protect the network from DoS and spam attacks. Layers 2 such as the Lightning Network or rollups significantly reduce transactions fees, but in addition to sacrificing decentralisation and security, being off-chain protocols, they reduce the economic sustainability of the network.

Unit of account: is a standard numerical unit for measuring the market value of goods, services and other transactions. Money is a basis for quoting and trading prices and is necessary to develop efficient accounting systems.

Note: the unit of account requires fungibility so that accounts of any amount can be readily settled. In economics, money is considered as a stable unit of measure with respect to its real value, but this hypothesis rarely occurs since its value fluctuates due to inflation and deflation. Fiat currencies and cryptocurrencies, being fungible, are usable as units of account and their value is influenced by inflation and deflation.

Standard of deferred payment: it is the function of being a widely accepted means of evaluating a debt in order to allow the purchase of goods and services in the present and their payment in the future. The possibility of using a blockchain as a system for deferred payments depends on the volatility of the corresponding cryptocurrency. Volatility for some popular blockchains:

- Bitcoin: historical 3.51%, last 90 days 3.06%.

- Ethereum: historical 9.41%, last 90 days 3.42%.

- Solana: last 90 days 6.86%.

- Algorand: last 90 days 5.33%.

- TON: unknown.

Note: the volatility of the main fiat currencies ($, €, £, etc.) or the main precious metals (gold, silver, palladium, etc.) is generally less than 1-2% and exceeds these values only in exceptional periods. Cryptocurrencies are fairly recent assets and for many of them there is not yet enough historical data for a meaningful analysis; Bitcoin is the longest running blockchain and has volatility values significantly higher than fiat currencies and precious metals, but decreasing over time and with a long-term trend to that of other assets.

Store of value: is the ability of an asset (currency, precious metal, real estate, government bond, jewel, artwork, etc.) to retain purchasing power in the future, especially during economic and financial crises because it has intrinsic value. Inflation is the main factor responsible for reducing the purchasing power of a currency and represents the sustained increase in the prices of goods and services within an economy. According to the most widespread thesis among economists, sustained inflation occurs when the growth of the money supply exceeds the economic growth of a state. The monetary parameters (circulating, total and maximum supply, money issuance) for some popular blockchains:

- Bitcoin: circulating and total supply 19.59 million (93.31%), maximum supply 21 million in 132 years (2140), decimal places 8 (21*10^14 units). Money issuance with decreasing rate to 0%, currently 1.69%.

- Ethereum: circulating and total supply 120.18 million, unlimited maximum supply, decimal places 18 (120.18*10^24 units). Money issuance with variable rate of 0.52% and burning mechanism.

- Solana: circulating supply 432.49 million (76.23%) and total 566.89 million, unlimited maximum supply, decimal places 9 (566.89*10^15 units). Money issuance with decreasing rate to 1.5%, currently 4.5% and burning mechanism.

- Algorand: circulating and total supply 8.04 billion (80.41%), maximum supply 10 billion in 10 years (2030), decimal places 6 (10*10^15 units). Money issuance with decreasing rate to 0%, currently 3.46%.

- TON: circulating supply 3.45 billion (67.76%) and total 5.10 billion, unlimited maximum supply, decimal places 9 (5.10*10^18 units). Money issuance with variable rate of 0.3-0.6% and burning mechanism.

Note: after the end of the gold standard (1970), the main fiat currencies ($, €, £, etc.) have an unlimited and unpredictable maximum money supply that has grown steadily over time and particularly over the last 20-30 years. The continuous money issuance was not accompanied by a corresponding economic growth and caused a loss of purchasing power of 87.75% for the dollar (since 1970 with average annual inflation 3.96%) and 45.05% for the euro (since 1997 with average annual inflation 2.32%). The monetary parameters of a blockchain are defined by its tokenomics and their modification requires the consensus of the network nodes. The money issuance allows to reward miners and validators and is fundamental for the economic sustainability of a blockchain, especially when the network is scarcely used. In general, blockchains whose maximum supply is limited are considered 'sound money', i.e. as forms of protection against inflation, albeit more volatile, than those whose maximum supply is unlimited which are subject to inflation, but more suitable for mass adoption. Finally, blockchains whose money issuance can become negative and thus maximum supply deflationary, thanks to a burning mechanism of transactions fees and sufficiently high network utilisation, are considered 'ultra sound money'.

Conclusion: the analysis of the economic aspects confirms that of the technological aspects and clearly shows that Bitcoin is not capable of realising a P2P electronic cash system as envisioned by the 2008 whitepaper. Bitcoin is an non-scalable and inefficient blockchain: for this reason it is only suitable for transferring large amounts of value due to often prohibitive transactions fees, it is unable to implement financial inclusion for those without access to banks and unable to redistribute wealth fairly among network participants. Moreover, the intrinsic inefficiency of the PoW consensus algorithm results in a huge waste of natural resources and the possible use of renewable energy is only a palliative. Bitcoin was born as an alternative to the banking system that caused the financial crisis of 2007-2008, it is considered by many (not all) as 'digital gold' for its ability to counteract economic and financial adversity, and is the best investment-speculative tool of the last 10 years despite its high volatility. However, especially in recent years its value trend has followed that of the stock market and traditional finance, i.e. it has behaved in the opposite way to the reasons for which it was created.

FAQ

Is the blockchain capable of realising an alternative payment system?

The characteristics of a good payment system are: speed, security, decentralisation, tamper resistance, energy efficiency and cost-effectiveness. The analysis shows that Bitcoin is unable to achieve this while other blockchains such as Algorand, Solana and TON can.

Is the blockchain capable of realising the Web3?

Web3 is a proposal for a new iteration of the WWW aimed at realising a decentralised ecosystem based on the blockchain. However, at the moment it is only a buzzword used as marketing; in fact, its realisation requires the same characteristics of a payment system as well as greater scalability and distribution of resources (computing and monetary) to accommodate Web2 users. The analysis highlights that probably only the blockchain TON is capable of realising it.

Is the blockchain economically sustainable?

The economic sustainability of a blockchain derives from tokenomics and transaction fees. The analysis reveals that blockchains whose maximum supply depends on network usage, Ethereum, Solana and TON, are more sustainable than those whose maximum supply is limited, Algorand and Bitcoin.

Does blockchain comply with data protection laws (GDPR)?

The GDPR is based on the concepts of centralisation, limitation and erasure that are in stark contrast to those of blockchain decentralisation, distribution and immutability. Therefore, in general, blockchain does not comply with the GDPR.

Is the blockchain a Ponzi scheme?

Currently, blockchain has no real utility, does not solve any concrete problems and can often be replaced by a more efficient traditional distributed database. However, it is an excellent speculative tool that people believe in, with the hope of making a profit, and become its main promoters. So, based on the duck test, blockchain is probably a Ponzi scheme.

Conclusion

Bitcoin is a cult, a new religion. The proof is left as a trivial exercise for the reader.

References

License

This document is released under the license Creative Commons Attribution-ShareAlike CC BY-SA.