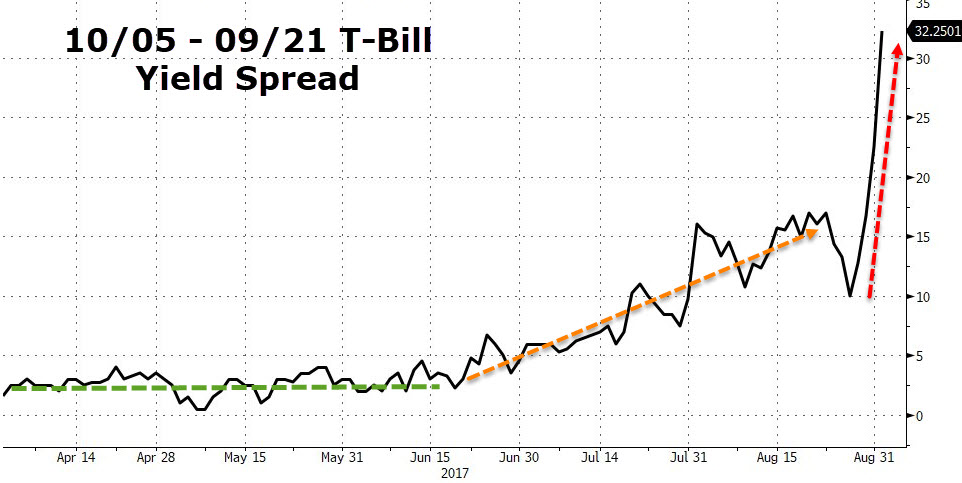

Yield Spread

🛑 ALL INFORMATION CLICK HERE 👈🏻👈🏻👈🏻

Yield Spread

^ Macro Musings Blog. 26 November 2008. What Corporate Bond Yield Spreads Tell Us

This page was last edited on 9 August 2020, at 23:01

Basis of this page is in Wikipedia . Text is available under the CC BY-SA 3.0 Unported License . Non-text media are available under their specified licenses. Wikipedia® is a registered trademark of the Wikimedia Foundation, Inc. WIKI 2 is an independent company and has no affiliation with Wikimedia Foundation.

To install click the Add extension button. That's it.

The source code for the WIKI 2 extension is being checked by specialists of the Mozilla Foundation, Google, and Apple. You could also do it yourself at any point in time.

In finance , the yield spread or credit spread is the difference between the quoted rates of return on two different investments , usually of different credit qualities but similar maturities. It is often an indication of the risk premium for one investment product over another. The phrase is a compound of yield and spread .

The "yield spread of X over Y" is generally the annualized percentage yield to maturity (YTM) of financial instrument X minus the YTM of financial instrument Y.

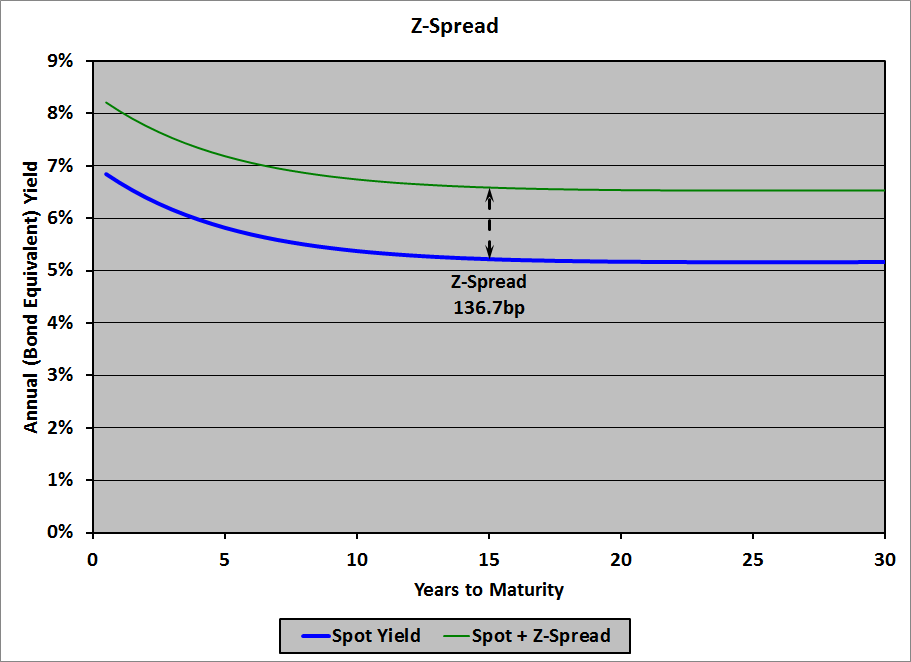

There are several measures of yield spread relative to a benchmark yield curve , including interpolated spread ( I-spread ), zero-volatility spread ( Z-spread ), and option-adjusted spread (OAS).

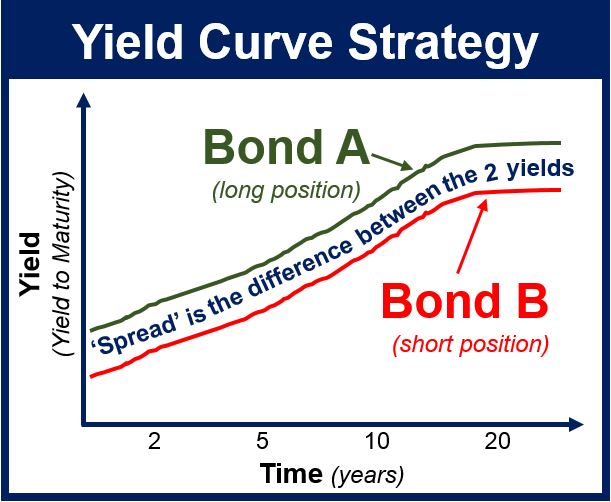

It is also possible to define a yield spread between two different maturities of otherwise comparable bonds. For example, if a certain bond with a 10-year maturity yields 8% and a comparable bond from the same issuer with a 5-year maturity yields 5%, then the term premium between them may be quoted as 8% – 5% = 3%.

Yield spread analysis involves comparing the yield, maturity, liquidity and creditworthiness of two instruments, or of one security relative to a benchmark, and tracking how particular patterns vary over time.

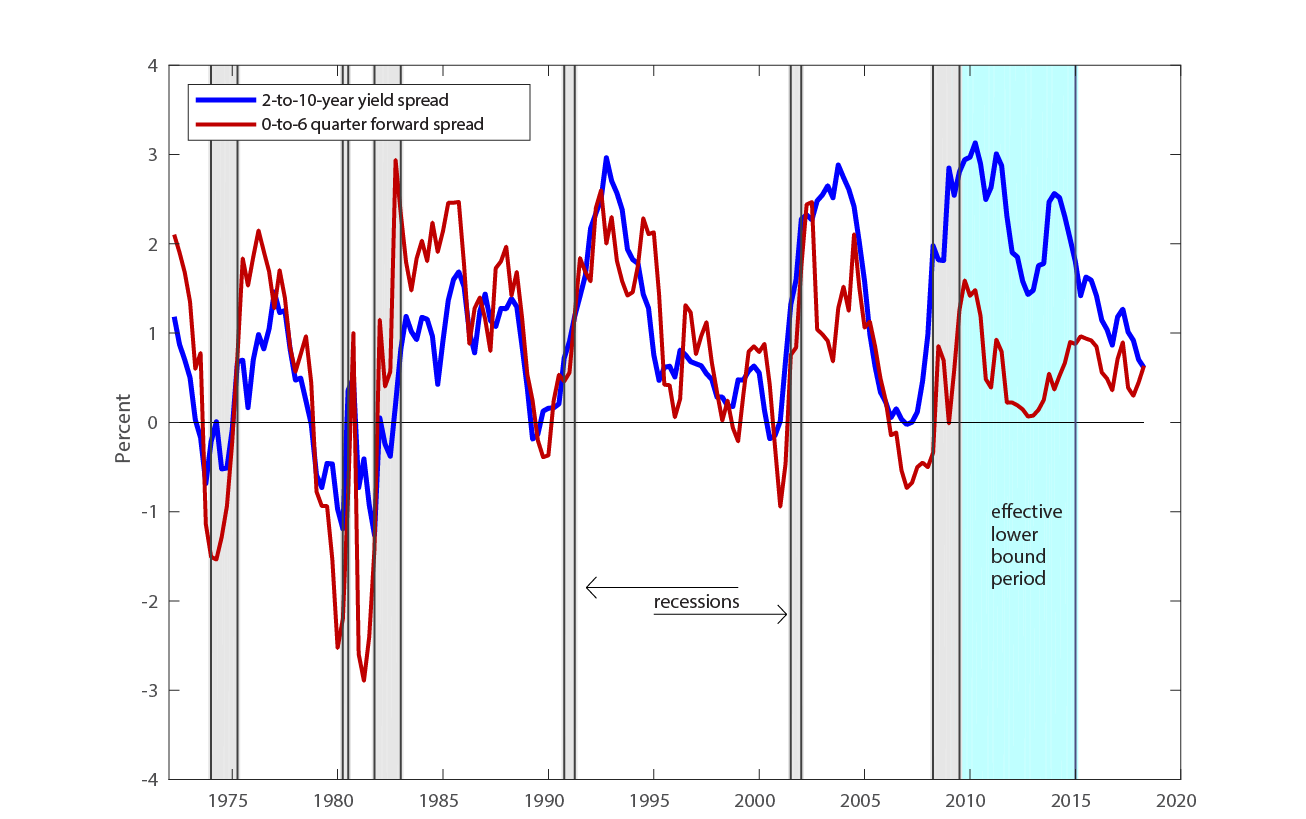

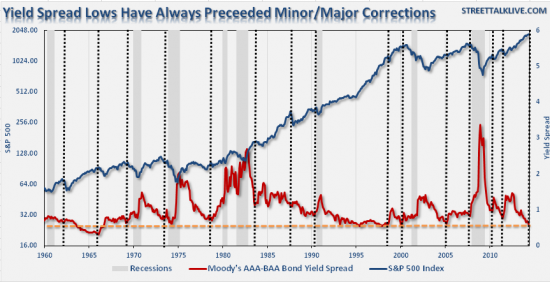

When yield spreads widen between bond categories with different credit ratings, all else equal, it implies that the market is factoring more risk of default on the lower-grade bonds. For example, if a risk-free 10-year Treasury note is currently yielding 5% while junk bonds with the same duration are averaging 7%, then the spread between Treasuries and junk bonds is 2%. If that spread widens to 4% (increasing the junk bond yield to 9%), then the market is forecasting a greater risk of default, probably because of weaker economic prospects for the borrowers. A narrowing of yield spreads (between bonds of different risk ratings) implies that the market is factoring in less risk, probably due to an improving economic outlook.

The TED spread is one commonly-quoted credit spread. The difference between Baa-rated ten-year corporate bonds and ten-year Treasuries is another commonly-quoted credit spread. [1]

Yield spread can also be an indicator of profitability for a lender providing a loan to an individual borrower. For consumer loans, particularly home mortgages , an important yield spread is the difference between the interest rate actually paid by the borrower on a particular loan and the (lower) interest rate that the borrower's credit would allow that borrower to pay. For example, if a borrower's credit is good enough to qualify for a loan at 5% interest rate but accepts a loan at 6%, then the extra 1% yield spread (with the same credit risk) translates into additional profit for the lender. As a business strategy, lenders typically offer yield spread premiums to brokers who identify borrowers willing to pay higher yield spreads.

Yield spread — Wikipedia Republished // WIKI 2

Yield Spread - Why Is It Important To Know? (In Detail)

Yield spread | Trader Wiki | Fandom

What Every Investor Should Know About Yield Spread

Yield Spread Definition

Yield Spread- Why Is It Important To Know? (In Detail)

Home » Finance » Blog » Investment Banking Basics » Yield Spread- Why Is It Important To Know? (In Detail)

All in One Financial Analyst Bundle (250+ Courses, 40+ Projects) 250+ Online Courses | 1000+ Hours | Verifiable Certificates | Lifetime Access 4.9 (3,296 ratings)

Course Price $149 $1999 View Course

The terminology Yield Spread is found to be used quite normally. Yield spread is basically the difference of rates of returns of two varied investments which are quoted, mostly of different credit quality. It is used by the bond investors in order to measure how much expensive or cheap a specific bond can be or a group of bond can be. Yield spread is known as credit spread and it is simply the difference in yields between two bonds. The yield spread is a technique of comparing any two financial products. In simple terms, it is a sign of the risk premium for investing in one investment product over another. When spreads expand between bonds with dissimilar quality ratings it denotes that the market is factoring more risk of default on lower grade bonds. For example if one bond is yielding 7% and another bond is yielding 8% then the “spread” is 1% point. If that spread expands to 4%, the market is predicting a greater risk of default which indicates a slowing economy. Spreads are basically stated in “basis points”, which means 1% point spread is usually said to be “100 basis points”. Non – treasury bonds are also estimated on the difference between their yields.

Normally saying, the greater risk a bond or asset class is, the greater its yield spread. Basically, the reason for this variance is that investors need to be paid to take risk. Investors generally don’t need a huge yield to tie up their cash, if an outlay or an investment is seen as being low-risk. But market participants/contributors will claim sufficient reimbursement i.e. a higher yield spread in order to take the chance that their principal could decline and this is only possible if an investment is seen as being higher-risk.

For an example: A bond issued by a huge well established & financially healthy corporates will usually trade at a moderately low spread in relation to Government Treasuries. On the other hand, a bond issued by a small company with a weak financial strength will trade at higher spread comparative to government securities. This states that the yield benefit/advantage of non-investment grade bonds comparative to high-rated investment-grade bonds. It also shows the gap between higher-risk emerging markets and the usually lower risk-risk bonds of the developed markets. Yield spread is used in order to calculate the yield benefit of two or more similar securities with different maturities. Spread is extensively used between the two & ten years treasuries which displays how much additional yield an investor can get by taking on the added risk of investing in long-term bonds.

Naturally yield spreads are not fixed or immovable because bond yield are always in motion, so too are spreads. If the yield difference between the two bonds or sectors is increasing or decreasing than the direction of the yield spread will increase/decrease or widen/narrow.

Generally, knowing that bonds yields will rise as their prices fall and will decline if the prices rises than a rising or growing spread shows that one sector is performing better than another. For an instance: let’s assume that the yield on a high yield bond index moves from 6.0% to 6.5% while the yield on government treasury stays even at 3.0%. Therefore, the spread has moved from 3.0 percentage points i.e. 300 basis points to 3.5 percentage points i.e. 350 basis points which shows that high-yield bonds underperformed government treasuries during this time. Therefore, if a bond or bond fund is paying an extraordinarily high yield this means anyone who hold that investment is also taking on more risk. As a result, investors should be conscious that merely selecting fixed-income investments with the highest yield will result in their taking on more principal risk than they negotiated for.

Yield spread analysis is prepared by associating the maturity, liquidity and creditworthiness of two instruments, or of one security to a standard. While mentioning to the “yield spread of A over B” this states the return on investment percentage from one financial security categorized as A less than the return on investment percentage from another security categorized as B. Therefore simply this means that the yield spread analysis is a procedure to relate or compare any two financial securities for an investor to regulate his options by evaluating risk & return on investment.

When it comes to making investment in several securities, analysis of yield spread helps the investors and interested people to understand the market’s movement. The investor can determine that the market is issuing more risk of default on the lower grade bonds if the spread is huge between bonds of diverse quality ratings. This shows that the economy is slowing down and therefore the market is foreseeing a larger risk of default. Conversely if the market is measured to have predicted a slighter default risk thus the spread is narrowing between dissimilar bonds of bonds of diverse risk ratings and this shows that the economy is expanding. For an instance: the market is normally considered to be issuing/factoring lesser risk of default if the spread between treasury notes & junk bond is four percent historically. Also, the yield spread analysis is advantageous when you are a lender because it can help you regulate your profitability when you provide a loan to a borrower.

For example: when a borrower is adequately proficient to take benefit of a loan at 4% interest rate but will essentially take a loan at 5%, the variance of 1% is the yield spread which is the extra interest that aids as added profit for the lender. As a tactic, several lenders propose premiums to loan brokers who propose loans with yield spreads and this is done to boost the brokers to hunt for borrowers who are willing to pay for the yield spreads.

According to yield spread analysis there exists a normal relationship between the yields for bonds in substitute sectors. In the period of depression and expansion, spreads is seen to be increasing & decreasing. Spreads will be affected by 3 ways:

“Yield-spread premiums” is what creditors call them. Customer groups call them authorized kickbacks. Yield spread premiums are the money that mortgage dealers or lenders get for directing a debtor into a home loan with a higher interest rate. Yield spread premium is the commission (fee) paid to the dealer by the mortgage lender in exchange for a higher interest rate or a beyond market mortgage rate. In industry’s, yield spread premium is known as ‘YSP’. Yet the debtor may be suitable for a mortgage at a definite interest rate, the dealer or loan officer can charge this payment and give the debtor a marginally higher rate to mark more commission. This exercise was formerly proposed as a way to evade charging the debtor any out-of-pocket payments, as dealers could receive their commission and shield final prices with yield spread premium. It is also known as negative points; yield-spread premiums are repayments creditors pay to mortgage dealers or debtors. Yield-spread premiums are a percentage of the principal.

For example: Mortgage creditors often pay up to 2% as a yield spread premium to mortgage dealers, so debtors should request about the yield spread premium way before final price.

For an instance, let’s assume that Mathew needs to derive $200,000 towards purchasing a house. He obtains an estimate for a yield-spread premium credit with a 6% interest rate and -2.136 points, means that he will obtain a $2,136 refund that he can apply to the loan’s final prices.

The substitute and other old-fashioned credit structure for the similar volume might be a 4.5% credit and one point, means that the credit has a minor interest rate but the debtor needs to pay a $2,000 down payment for the loan.

It is significant to remember that mortgage dealers don’t always advise customers about accessible yield-spread premium credits. A mortgage agent might, for an instance, obtain a quotation from a comprehensive financier for a finance that has a 6% interest rate and -2.136 points. On a $200,000 credit, these yield-spread premiums decipher to a $2,136 acclaim that can be functional toward final prices. Anyhow, in order to make money on the deal, the mortgage agent marks up the finance to the customer and estimates a charge of, say, 6% and 0 points, thus recollecting the $2,136 for themselves as reimbursement for brokering the loan.

Yield-spread premium advances commonly have higher interest rates. Hence, debtors who plan to be in their houses for only a short span of time are basically the best applicants for these advances. The additional interest over a moderately short span of time tends total not as much of than the final prices the debtor would have had to pay otherwise.

Learn the juice of this article in just a single minute, Yield Spread Infographics

All in One Financial Analyst Bundle (250+ Courses, 40+ Projects)

© 2020 - EDUCBA. ALL RIGHTS RESERVED. THE CERTIFICATION NAMES ARE THE TRADEMARKS OF THEIR RESPECTIVE OWNERS.

This website or its third-party tools use cookies, which are necessary to its functioning and required to achieve the purposes illustrated in the cookie policy. By closing this banner, scrolling this page, clicking a link or continuing to browse otherwise, you agree to our Privacy Policy

Special Offer - All in One Financial Analyst Bundle (250+ Courses, 40+ Projects) Learn More

Sperm On Clothes

Riding Sex Machine

Naked Wrestling

Bi Sex Oral

Anal Penetration Video

.1566418097341.png)