Three Common Financial Statements - Simple Breakdown (#63)

Kurtis HanniFinancial statements can be intriguing, but they are simple. Today, we are going to breakdown the three most common financial statements that every business has:

1️⃣ Income Statement - are you profitable?

2️⃣ Balance Sheet - are you healthy?

3️⃣ Statement of Cash Flows - where is cash going?

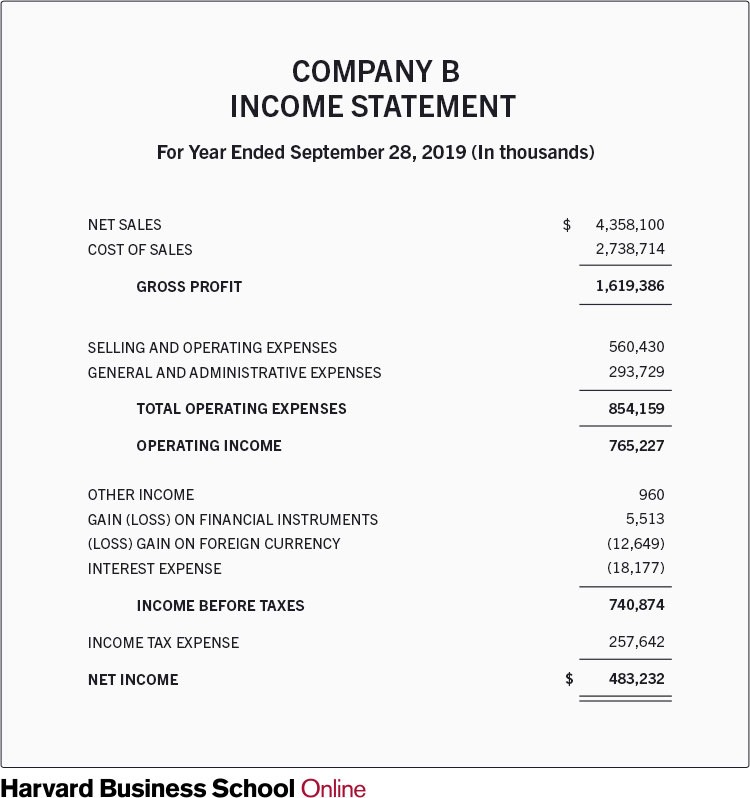

1. Income Statement

This statement tells you whether or not you’ve made a profit over a given period of time.

The formula:

Revenue - Expenses = Profit

Expenses can be further broken down into two buckets:

1) Cost of Goods Sold or COGS

- is cost related to revenue.

2) Overhead expenses

- costs required to run the business, but not directly related to revenue.

The income statement helps you:

👉🏼 Identify how much revenue you’re bringing in

👉🏼 Understand if you’re making money on your product

👉🏼 Identify if your fixed or overhead costs are too high

👉🏼 Itemize your costs to make better decisions

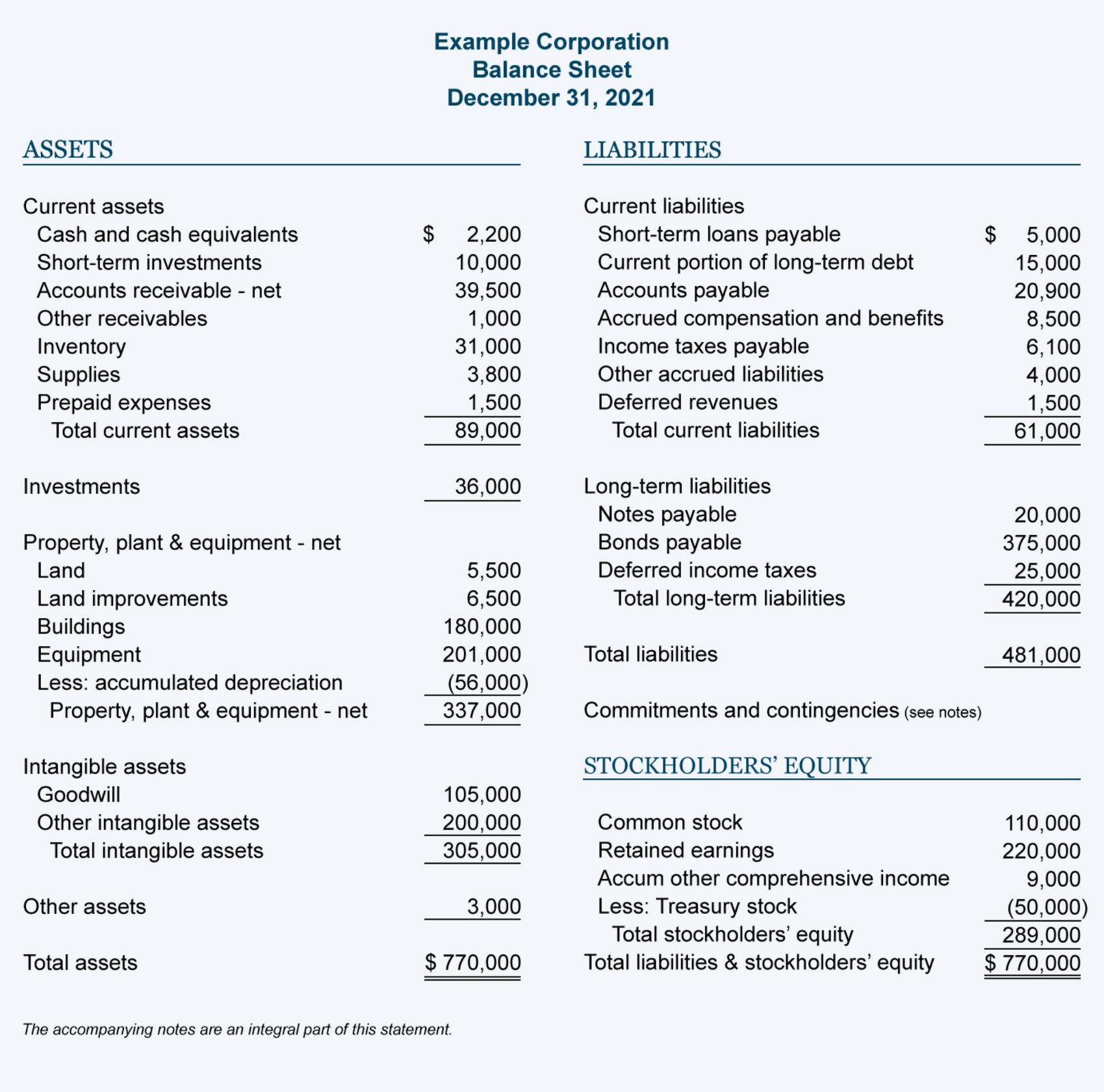

2. Balance Sheet

This statement tells you a company’s financial strength at a specific snapshot in time.

The formula:

Assets = Liabilities + Equity

Asset

- is what you own. Such as:

👉🏼 Cash

👉🏼 Accounts Receivable (money owed to you)

👉🏼 Inventory (product in your possession but not sold)

👉🏼 Fixed Assets (property, equipment, machinery, or vehicles)

👉🏼 Intangible Assets (software, licenses, trademarks, or goodwill)

Liability

- is money that you owe. It can be classified into two:

1) Current Liabilities: are money to be paid in < 1 year.

👉🏼 Accounts Payable (money owed to vendors)

👉🏼 Credit Card Payables (just a different accounts payable)

👉🏼 Short-term debt (obligations to pay)

2) Long-term liabilities: money owed in > 1 year.

Equity

- is how much the company is worth on paper:

👉🏼 Money put in the business

👉🏼 Money taken out of the business

👉🏼 Earnings retained in the company

From the balance sheet you learn:

👉🏼 How strong the business is financially

👉🏼 Whether short-term obligations can be met

👉🏼 The amount of debt a company has

👉🏼 The book value of the company

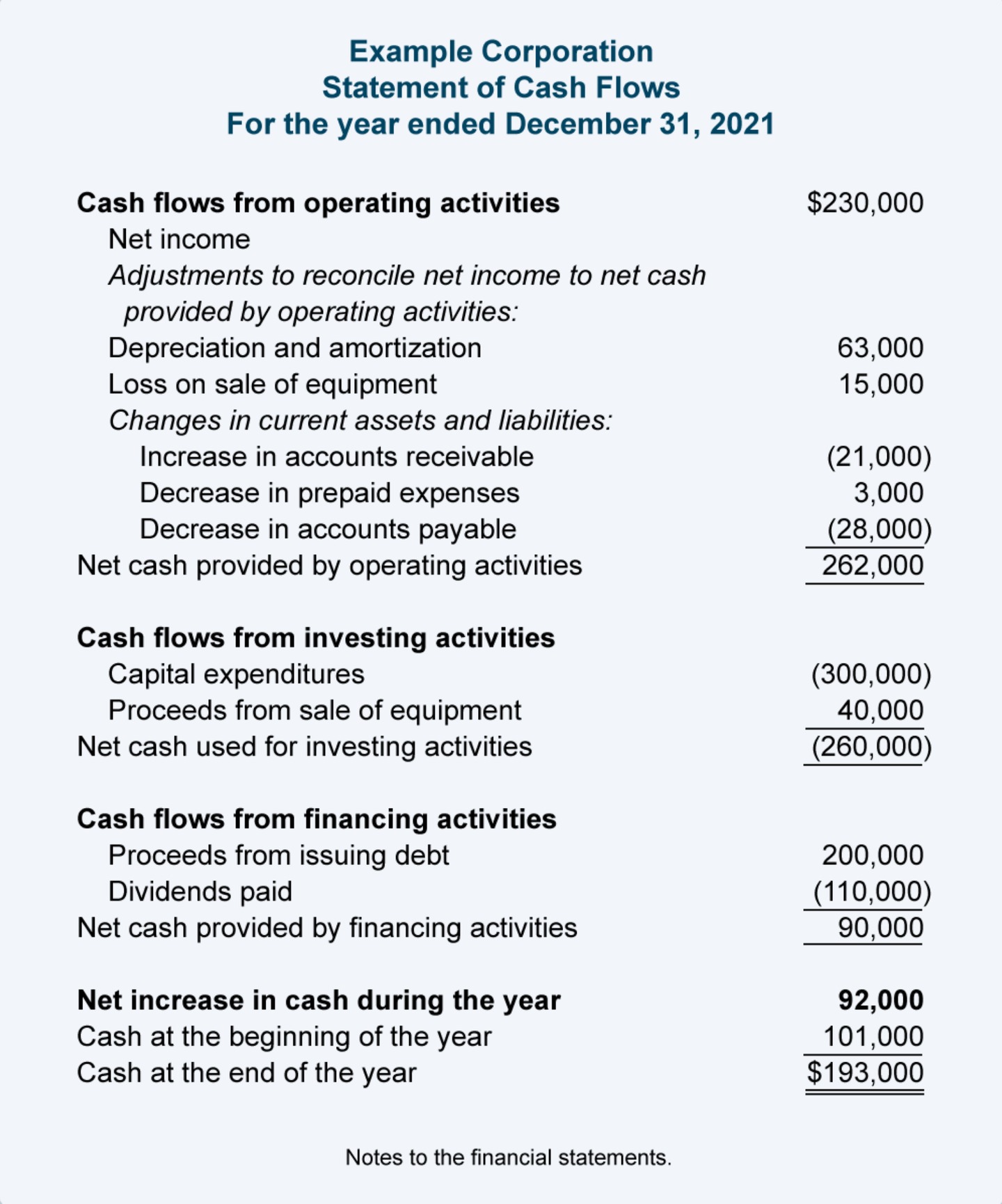

3. Statement of Cash Flows

This statement helps you understand how cash has been spent over a period of time.

The formula:

Net Increase/Decrease of cash during period + Cash at beginning of period = Cash at end of period

The net increase/decrease is broken down into three categories:

1. Operating Activities

- cash collected from sales versus cash paid related to sales.

2. Investing Activities

- new equipment purchased or sold.

3. Financing Activities

- change in debt or inflow of capital.

This statement helps you answer the following questions:

👉🏼 is your cash flow positive or negative?

👉🏼 why your cash flow is positive or negative

👉🏼 whether operations is carrying its weight

👉🏼 what investments or financing is costing

•••

💡Read Next

💰Peter Thiel: 7 Investing Secrets (#62)

Or

➡️ Newsletter 📧

➡️ Twitter 🐦

➡️ Instagram📱

➡️ LinkedIn 🔗

➡️ Telegram 🚀

➡️ Facebook 💻

➡️ YouTube 🎬

➡️ TikTok📱

➡️ E-magazine 📰

➡️ Community 💁♂💁♀

➡️ WebPage 🖥️