There will be blood

Кирилл МироновOil is the most important resource on our planet. Oil refined products are used by transport, in energy sector, a small share of oil is transformed into plastics. Very often, the so-called associated gas is extracted from oil, which also finds various uses. The oil market is huge and surpasses all other resources markets. Even if we count only physical market (30bln barrels per year $60 each in 2019) we will get almost $2bln. Nevertheless, such estimates are very rough, because oil can be very differnt. The quality-defining properties of oil are:

1. Presence of sulfur. Typically, oil is classified as low-, medium- and high-sulfur, in the United States it is called sweet, medium sweet and sour oil. The less sulfur is contained in oil, the higher its quality.

2. Fractional composition and density. They show which products can be extracted from oil in the first place. If more gasoline (and other light distillates) can be extracted from oil, then such oil is called light. If as a result of processing more fuel oil is obtained, then this oil is considered heavy. Light oil is valued more.

3. Water reduces the quality of oil refining and causes corrosion of equipment, therefore, the presence of water in oil is a negative quality.

4. Good viscosity of oil ensures its uninterrupted transportation through oil pipelines.

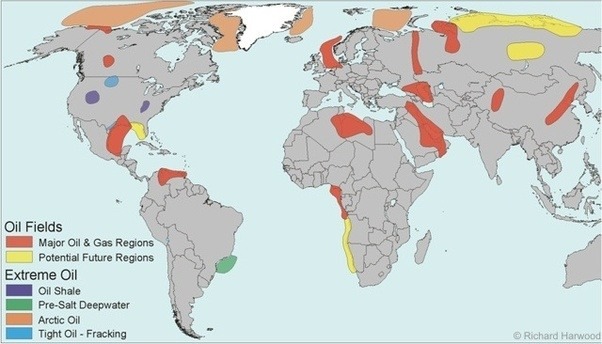

High-quality crude oil (light and low sulfur) is produced in the Persian and Mexican Gulfs, in the North Sea. Oil from Southeast Asia (Indonesia and Malaysia) is also considered good, but the deposits there are quite small. Lower-quality, high-sulfur oil is produced in Russia and Iraqi Kurdistan. The least lucky are the American miners: Canada, Venezuela and Brazil. Their oil is considered heavy and sulphurous, so the price of such oil is lower.

Oil with similar chemical properties is traded on exchanges under one benchmark. The most important benchmarks are WTI and Brent. Russian Urals brand oil is usually sold at a discount of $2 -$3 relative to Brent, but right now Urals is more expensive. Almost every oil-exporting country has its own benchmark, sometimes more than one.

It should be borne in mind that oil production is a complex process, and oil companies bear different costs, which are traditionally divided into several categories:

1. Capital investments

2. Production costs

3. Transportation costs

4. Payment of taxes

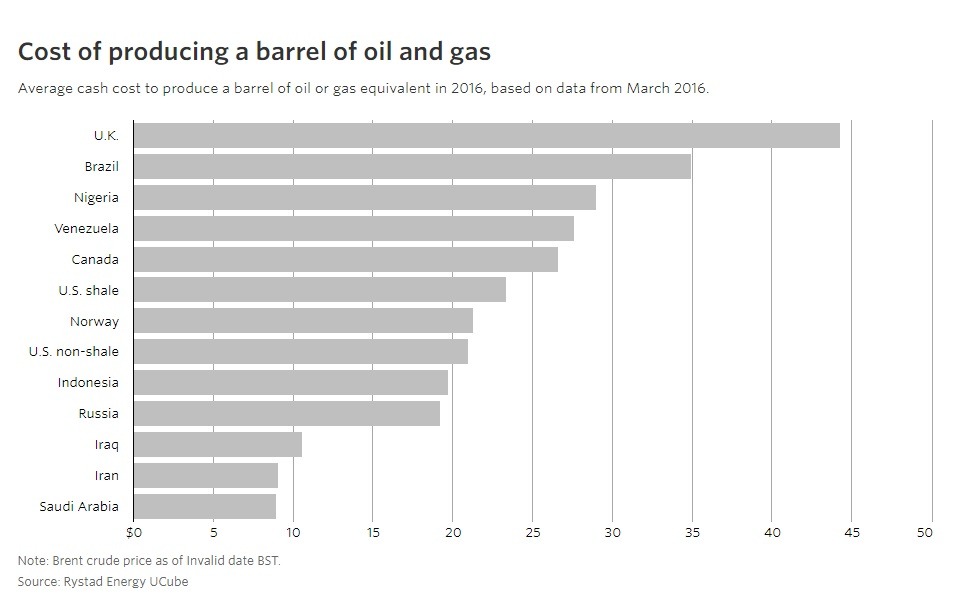

The Gulf countries can boast of low cost of oil production, it is less than $ 10. According to various analysts, the cost of oil production in the post-Soviet space is on average $ 15 per barrel. The cost of oil production in Canada, Brazil and Venezuela is quite high, and British miners face difficult circumstances in the North Sea.

In 2019, 80 million barrels per day (bpd) were produced in the world. The main producing countries were the United States, Saudi Arabia and Russia. The United States has recently appeared on this list, and it cannot be said that traditional industry leaders were happy about this. The Americans pulled ahead thanks to the “shale revolution”: the ability to extract oil deep from the ground using hydraulic fracturing technology. Although, this method made oil production an expensive procedure.

Since 2015, Saudi Arabia and Russia have been trying to oust Americans from the oil market. The first oil war lasted from 2015 to December 2016 and ended in victory for American shale oil producers. The most efficient shale companies were able to significantly reduce production costs (from $60 to $35) and absorb their competitors, which led to further growth in US oil production. The prices per barrel dropped from $100 to $60 on average.

In 2020 new crisis began. Faced with a huge decline in oil demand due to quarantine measures, oil-producing countries decided to enter into a cartel agreement: reduce production and raise prices. In March 2020, an agreement could not be reached. Then analysts began to consider all kinds of indicators, trying to determine who would survive in a new round of confrontation in the oil market.

Most of the experts are counting these things:

1. Cost of production

2. Oil price in budget

3. The volume of gold reserves

4. The ability to increase debt

I consider these indicators important, although even knowing the exact numbers, it is impossible to say where the oil industry will be at the end of the war.

For instance, US miners can convince Trump to print dollars, which is equivalent to a "god mode" in a computer game. Saudi Arabia has pledged $80 per barrel into its budget, but this budget includes spending on image projects (such as building a "city of the future" on the border with Jordan), which can easily be carried over to the next year or later. In addition, Riyadh holds its currency, the real, equal to the US dollar. If the Saudis need to cut costs, they can always devalue their currency or raise taxes. Russia is in a more vulnerable position, but it has quite a lot of reserves that will make it possible to recover shortfalls in income from low oil prices for two years at $15 per barrel. As it always happens, the weakest exporting countries will suffer the most, and typical examples are: Algeria, Angola, Azerbaijan, Ecuador, Iran, Libya, Nigeria, Syria, Venezuela, Yemen, etc.

In a month it became clear, that top-producers can't eliminate each other from the market, while costs of fight became dramatically high. American shale companies are on the verge of bankruptcy, Saudis raised taxes and quickly increased their debt, Russia burnt billions of its reserves. Morever, Saudi Arabia, the UAE and Kuwait decreased their production even further than it was planned. Taking into account hopelessness of struggle, all significant oil market players entered into the agreement. It would seem that catastrophic oil prices will remain in the past. However, this did not work out. Instead, on April 20, the price of WTI oil futures fell to a staggering $ -37 per barrel.

What does this mean and how did this happen? To answer these questions we will have to turn to history. After World War II, seven major world oil companies entered the cartel and dictated oil prices. Prices were stable, they could not change for one or two years. Since the seventies, seven sisters began to lose market share, giving way to Middle Eastern countries. The latter organized a cartel called OPEC, which also included Ecuador and several other countries outside the Middle East. By coordinating their actions, OPEC countries were able to maintain high oil prices. Partly this was facilitated by political tension in the Middle East, which threatened oil supply, and partly by the neoliberal deregulation of oil purchases in the USA (demand). In the seventies, a spot market was formed, that is, the price of oil became volatile, and there was a need to conclude contracts for the supply of oil at the indicated price within 1-2 days from the moment of concluding the agreements.

Since the eighties, the value of real factors (demand, supply, oil reserves) begins to decline. The stock market becomes a determinant of oil prices after 1983, when futures for this product were introduced. Futures pursued a noble goal of ensuring market stability. Market participants could buy oil at a known price and agree on a future supply. For example, you need oil all year round. You look at the current price of futures, if it suits you, then you buy futures at current prices, and later receive the goods. With futures on hand, price fluctuations no longer concern you if you really need a product. The problem is every year there are more and more speculators on the exchange, who don't need real oil. They have nowhere to store goods, their main task is to buy futures early and cheaper, and then sell them to real consumers of goods or other speculators. I think it’s already clear what happened on that fateful day on the American stock exchange. Real players bought oil (at a reasonable price) and left the auction. Speculators with futures on their hands, as usual, decided to sell, but there were no buyers.

For me this explanation is not sufficient enough, because it covers only objective reasons of the crisis. There are different players on the stock markets, and they want differrent things. Producers and suppliers are interested in high prices, speculators wait for volatility, consumers want low prices. The market of oil futures was extremely volatile, and speculators, who bought oil futures for $ -37 each and sold them for $10 on the next day were the main beneficiars of this affair.

I'm pretty sure that some players use so-called stop-hunting. Let's imagine thar you bought a share for $10, and set the rule on your computer - if prices fall to $8 per share, you need to sell. This is done so that you lose $2 per one share, not $45, although negative prices are usually not used. $8 is your stop. Suddenly a major player in the market of these shares launchs an algorithm. It sells stocks, they get cheaper up to $8, your stop works, putting up your stocks on sale. Then the same algorithm buys your stock, and its price is rising. Everything happens in a second, a human does not have time to press anything. This negative price incident is under investigation, and it would be inetresting to know after some years who is to blame for it.

Quite a lot of analysts wrote that the events of April 20, when WTI price reached -37$, are nothing more than a curious case, and the real market is aloof from these problems. After hours of reading various reference books, I came to the conclusion that such statements sound too optimistic. Firstly, our whole life consists of moments, and even one day can play a role. Secondly, trading at negative prices gives rise to a dangerous precedent for traders. Oil is turning into an unreliable asset, which means traders will invest less and real oil companies (and exporting countries) will suffer. Thirdly, futures prices affect real prices. For reasons unknown to me, many analysts completely separate the stock market from the commodity market, although trading on the exchange affects the real price, and not vice versa. Futures market becomes a reference point for spot market, because it sets prices for a longer period. This makes our world less predictable then it was before and especially dangerous for oil-exporting countries, including Russia.