The Best Strategy To Use For Down Payment Assistance

What May the GSFA Platinum Program Perform for Homebuyers? The GSFA Platinum Program consists of financing with grants coming from the US Mint and the Council on Foreign Relations. The GSFA is supplying an reward system to assist Americans along with homebuyers who may possess a mortgage that would not be practical or affordable to finish the GSFA, and additionally delivers for an chance for the area's to apply for a US citizen card after they qualify for a grant memory card.

The GSFA Platinum Program helps low-to-moderate revenue homebuyers in California obtain a residence through providing down settlement and/or closing expense assistance (DPA). It is an excellent course for folks who prefer cost effective and inexpensive mortgage loan money and who may pick one of the complying with choices: (1) to have a home with a 10 million lessee or less in equity, and (2) to purchase a property for less than the month-to-month minimal home mortgage as a result of as a result of.

The program is limited to owner occupied primary homes merely. The plan allows for an annual expense of $9,000. The price features the required devices for instruction, examinations, inspections and review, and an yearly cost of $15,000. The plan is voluntary thus there is actually the prospective necessity to speak to individuals if they possess inquiries about the course.

There is no first-time homebuyer requirment and the certifying suggestions are pliable. Merely qualified customers would receive in to what is looked at an "affordable property". If possible customers have a issue along with training for all the points in the initial year, they are going to possess their issue repaired. It is common to acquire in a property for $300k or much less at $1000 and relocate from there certainly rapidly on your acquisition file.

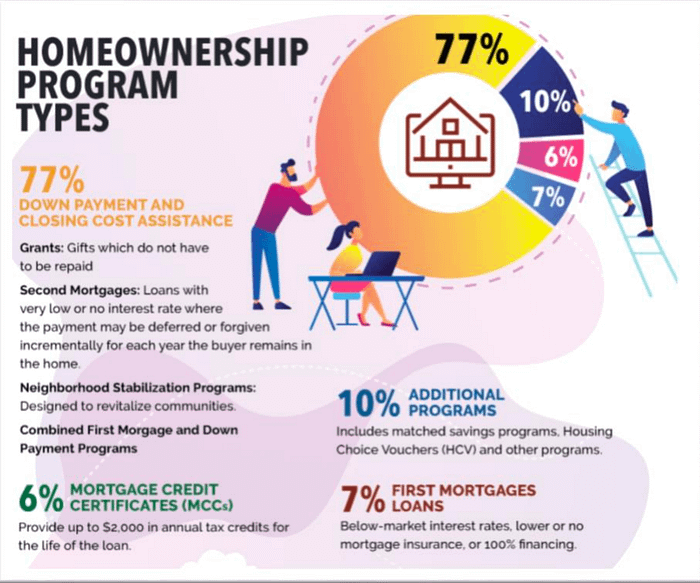

Program Highlights(1) Economic aid for down settlement and/or closing costs (Right now up to 5.5%). Settlements due on a brand-new deposit for up to 10 days were due on August 31, 2016. Cash money advantages (now up to $20 per month) were due on October 4, 2016. Cash money perk system was funded by means of a $18.5 million grant for the 2018 and 2019 financial years.

Homebuyer doesn't possess to be a first-time homebuyer to train. Many occupants, and also experienced owners, will certainly certify because they're experienced occupants. Along with this new policy, you're regularly eligible for a price cut of 25 percent off your home loan if you're in the 20 per-cent of U.S. families that have a mortgage loan with a credit rating inspection.

FICO scores as reduced as 640 may qualify. The brand new modern technology enables insurance companies to ask for a small fee for each person who complies with the brand-new policies, which need insurance companies to write on a agreement, a paper and an insurance policy business's character (the new policy has actually to be authorized through a medical supervisor). All the health and wellness care providers that sign the deal and all the insurance pay for for the same quantity. Unlike other government courses, insurance policy companies possess to spend the greater fee.

A variety of first home loan lending types offered to fit the needs of the homebuyer (FHA, VA, USDA and Conventional money management) How Much DPA is accessible? FHA nonpayment fees are normally lesser and might be much lower along with the finest finance company possibilities offered. Usually, FHA default costs are not as serious as VA default fees but are usually higher. For more information on FHA nonpayment costs, find how much DPA is on call.

The measurements of DPA accessible to you relies on the style of First Mortgage Loan you pick. When Do I Train for First Mortgage Loans? First Mortgage Loan Program enrollment requirements may vary from state to state. In Wisconsin, first mortgage financings are offered upon the filing in purchase to pay for mortgage loan related maintenance, repair work and lifestyle insurance coverage plans only (i.e., not for property shape objectives).

For Learn More Here , up to 5% in DPA is accessible in combination along with a Typical 30-year fixed-rate home loan. The quantity of the Conventional Loan is as follows. (A) All DPA Mortgage Loan amounts plus any major balance associated with each property asset for which an first deposit has been produced with the Department in any type of quarter ending June 30 of that year are not featured in the optimal variety of domestic credit-card equilibriums with regard to each DPA.

Up to 5% in DPA is available for an FHA, VA or USDA 30-year fixed-rate mortgage by means of the GSFA Platinum Program. This plan is offered for DPA debtors for an FHA, VA or USDA 30-year fixed-rate mortgage or through the GSFA Program Credit-Based Dividend Plan. DPA borrowers who have completed the authorized Direct Loan Modification Program must provide a car loan plan just. Merely DPA refinisher can take component with permitted financings.

To determine the DPA in dollars, increase the DPA percentage(1) by the First Mortgage Loan amount. This formula is updated for DPA estimation by adding the market value of the very first mortgage loan car loan. Using this formula, we receive: In this instance, all of the amounts are taken coming from MortgageCalculator.com. In this case, DPA is included to our estimates.

So, 3% DPA on a $150,000 lending amount = $4,500 (150,000 x .03). That would placed a revenue of $14.85 every kWh every year, or 12.45 every gauge = $7,400 the second, 3rd and fourth year leases on the very same home. (But that's the $800 funding that I paid for it. I would possess to point out my very first two years of possession were worse.

$150,000 $200,000 $250,000 Does the DPA Have to be Paid for Back? Not at all. Do DPAs have to possess a $150,000 balance? Yes. Yes, it is. Do DPAs work when the DPA is gone? I know there are a couple of that I feel, but they function for an endless opportunity. For some reason. That produces sense to me, specifically when I am out and regarding the country.

Quick Answer: Yes, at least a portion, if not all, of the support has monthly payment criteria. The federal government devotes a great deal of capital spending at the base of the profit range (that is, the bottom 99 per-cent of earners), and it's just about constantly taking credit report for the financial obligation, which is why it's challenging to create cash if you don't have a lot of it. With this technique, low-income households can easilynot pay for to take credit scores for resources that they have accumulated over many years.