TON validators APR vs APY

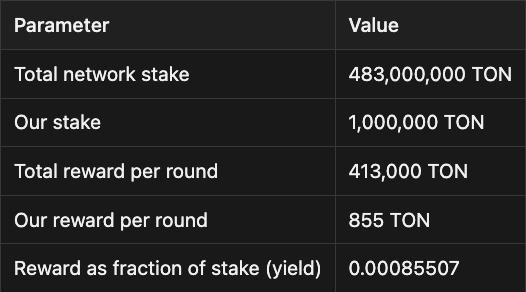

TON TechKey numbers

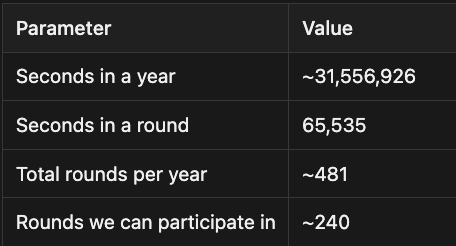

Round timing

A validation round lasts 65,535 seconds (~18.2 hours). However, each round also includes ~9 hours for elections beforehand and ~9 hours of hold time afterward. This means funds are locked for roughly 36 hours per cycle, and a validator can only participate in about half of all rounds in a year.

Note: TON has odd and even rounds with a slight imbalance between them. This document ignores that distinction for simplicity.

APR (Annual Percentage Rate)

APR is the simple, non-compounded annual return. Since we only participate in half the rounds, we multiply the per-round reward by half the total rounds:

APR = reward_per_round × (rounds_per_year / 2) APR = 0.00085507 × 240 APR ≈ 20.57%

This is straightforward and uncontroversial.

APY (Annual Percentage Yield)

APY accounts for compounding — each round's reward is added to the stake, so future rounds earn slightly more. The question is how to account for the fact that we only participate in half the rounds.

There are two ways to do this, and they give different results.

Incorrect formula

APY = ((1 + reward_per_round) ^ rounds_per_year - 1) / 2 APY = ((1.00085507) ^ 481 - 1) / 2 APY ≈ 25.44%

This compounds over all 481 rounds as if our stake grows every round, then divides by 2 at the end. The problem: we aren't actually compounding during the rounds we sit out. Compounding over 481 rounds and halving afterward overstates the yield because it grants compound growth that never happened.

Correct formula

APY = ((1 + reward_per_round) ^ (rounds_per_year / 2)) - 1 APY = ((1.00085507) ^ 240) - 1 APY ≈ 22.83%

This compounds over only the 240 rounds we actually participate in. The exponent reflects reality: compounding only occurs when the stake is active and earning rewards.

Why the difference matters

Both formulas "halve" the APY to reflect partial participation, but they do it at different points:

- Incorrect formula: compound first over all rounds, halve later → inflated result

- Correct formula: compound only over participated rounds → accurate result

The gap (~25.44% vs ~22.83%) comes entirely from phantom compounding in rounds where our funds are idle. The correct formula should be used for any reporting or decision-making.

Important notes on APR vs APY in practice

APY projections assume a specific compounding scenario and are highly dependent on market behavior:

- If everyone compounds their rewards, the total network stake grows proportionally for all participants. In this case, everyone's APY effectively converges to the same value as APR — compounding gives no relative advantage when all participants do it equally.

- If new assets enter staking, the total network stake increases, which means rewards are split among more TON. This directly lowers APR (and by extension APY) for all participants.

- Our projected APY of ~22.83% is only accurate in the scenario where everyone except us withdraws all their staking rewards. In reality, other validators compound too, so the actual realized APY will be somewhere between APR and the projected APY.

Why this matters now

Before the network speed-up, APR was around 4.11%, with the correct APY at ~4.19% and the old formula giving ~4.28%. A 0.09% discrepancy was not critical — this metric is only used for display, not for reward calculations. When network rewards increased roughly 6x, that same mathematical error was amplified proportionally, producing a ~3% gap between the two formulas. The growing divergence between APY figures reported by different services raised concerns, prompting us to re-evaluate the long-used math.