Swiss Franc Spread Betting Losses

🔞 ALL INFORMATION CLICK HERE 👈🏻👈🏻👈🏻

Swiss Franc Spread Betting Losses

Photographer: Stefan Wermuth/Bloomberg

19 мая 2020 г., 7:00 GMT+3

Updated on

19 мая 2020 г., 12:45 GMT+3

Options point to parity with euro, last seen in shock of 2015

Central bank spent billions trying to curb currency’s advance

( Updates with EU aid, company profits starting in the third paragraph )

Before it's here, it's on the Bloomberg Terminal.

Terms of Service Do Not Sell My Info (California) Trademarks Privacy Policy ©2021 Bloomberg L.P. All Rights Reserved

Your monthly limit of free content is about to expire.

Stay on top of historic market volatility. Try 3 months for $105 $6. Cancel anytime.

Bloomberg Anywhere clients get

free access

Want the lowdown on European markets? In your inbox before the open, every day. Sign up here .

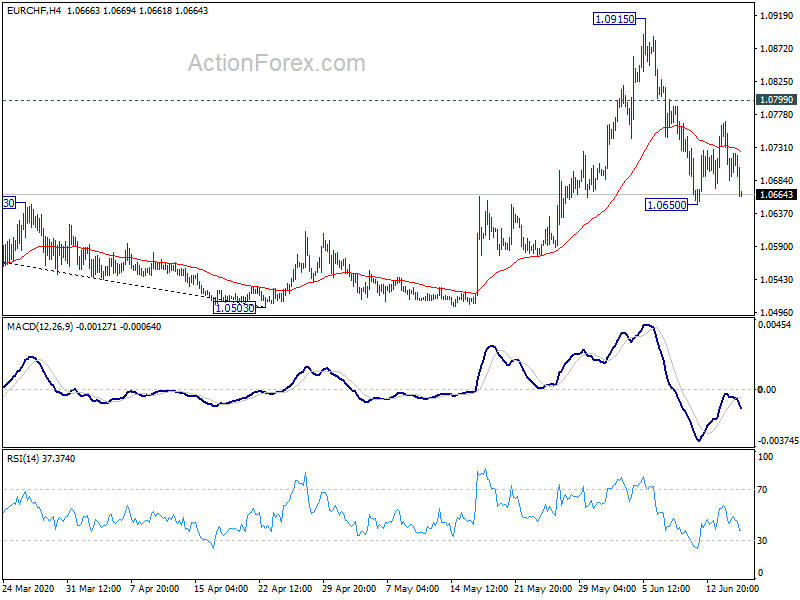

Despite billions spent by the Swiss National Bank to curb the franc’s advance, traders pushing the currency toward parity with the euro might have their way.

With the global economy in recession and the euro area risking a new debt crisis, the currency -- a popular haven -- has already come close to breaking through 1.05 per euro this year.

Even a German-French agreement for a European Union aid package failed to derail options bets that signal the pair may soon be on equal footing for the first time since 2015.

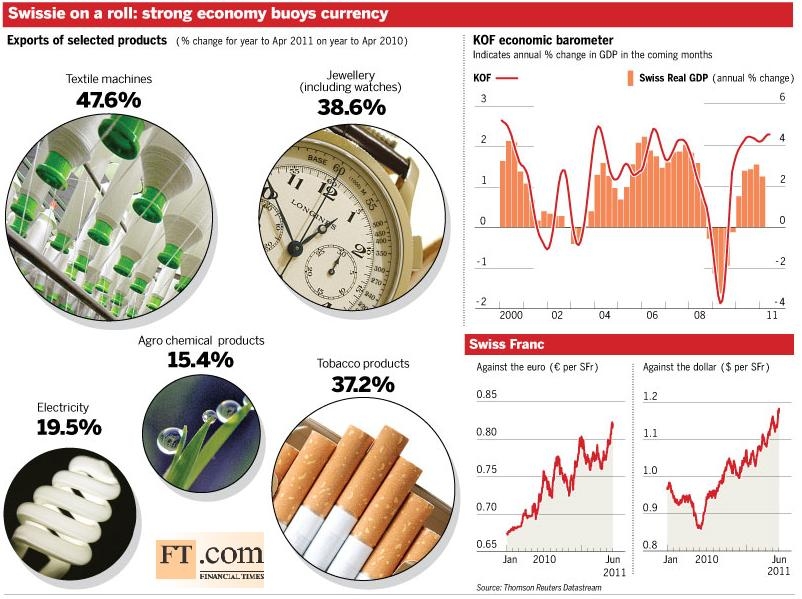

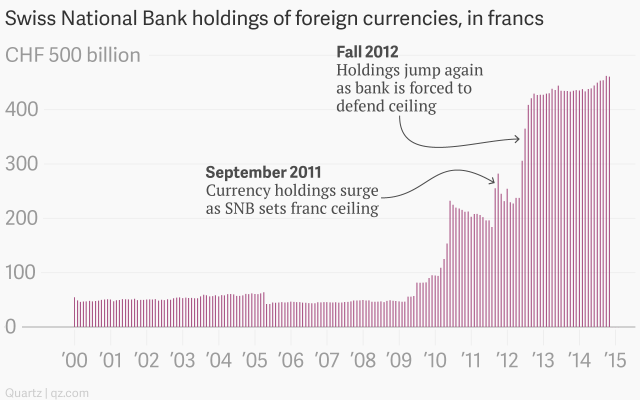

The central bank has struggled to tame the currency for years, with the institution injecting over 440 billion francs ($454 billion) into the foreign-exchange market since 2009. And yet the currency rose about 30% in a decade, fueled by recurring anxiety over global growth and a euro-area breakup .

Fears of how badly the coronavirus will hurt economies worldwide are just the latest in a long list of reasons why demand for the franc is high. The franc is a haven because neutral Switzerland, with its banks, rule of law and political stability, has for decades been considered the one of the safest places for the world’s rich to park their money.

There’s been market speculation that officials have their eyes on a new exchange-rate target that they’ll defend to the hilt. Some investors are focused on 1.05 per euro, after previous thresholds such as 1.12 and 1.08 were taken out. Strategists warn these triggers are largely fictional, meaning the race toward parity could come faster than anticipated.

“Markets like nothing more than talking about round numbers, so much so that they can become self reinforcing,” said Jeremy Stretch, head of G-10 currency research at Canadian Imperial Bank of Commerce in London. “Does the SNB really care explicitly about the number? Probably not.”

The SNB spent a record 188 billion francs on interventions in 2012

If the franc breaks through 1.05 per euro, it could “easily” head toward 1.02 per euro, according to Stretch. So far this year the franc has outperformed all Group-of-10 peers against the dollar save the Japanese yen, a fellow haven.

The SNB says it doesn’t target levels and instead takes the currency situation broadly into account.

Simply handing the franc over to the vicissitudes of the market would send it soaring, making Swiss goods abroad more expensive, and potentially causing manufacturers to lose orders and banks to see profitability evaporate.

Hearing aid-maker Sonova Holding AG on Tuesday said the stronger currency had a “significant negative impact” on growth in the last financial year.

Swatch Group AG Chief Executive Officer Nick Hayek has been one of the most prominent advocates of a weaker currency. So too have left-of-center politicians, who fear companies whose margins have dried up due to the rallying currency will fire staff to compensate.

Another consideration is what a stronger franc means for inflation. While cheaper imports are a boon for shoppers, they’re a headache for policy makers whose mandate is to keep the rate of inflation positive but under 2%. Consumer prices have dropped for the past three months on a year-on-year basis.

“As long as you don’t have a 5% or 10% move in the franc in a matter of weeks or months, a small 1% move here or there doesn’t impact inflation,” said Viraj Patel, a currency and macro strategist at Arkera Inc.

In a country whose financial sector prizes discretion, SNB President Thomas Jordan and his colleagues provide few details about what they’ve been up to in the foreign-exchange market. Weekly data hint at the scope of activity, but the only hard evidence is the annual report’s tally of money spent on interventions.

But rather than stem the advance in the franc altogether, it seems the SNB’s approach has shifted. While it used to say the currency would weaken over time, that turn of phrase was abandoned several years ago.

“Their modus operandi is now one of damage limitation -- slowing the appreciation of the franc rather than putting a fork in the road,” said Kamal Sharma, director of G-10 foreign-exchange strategy at Bank of America.

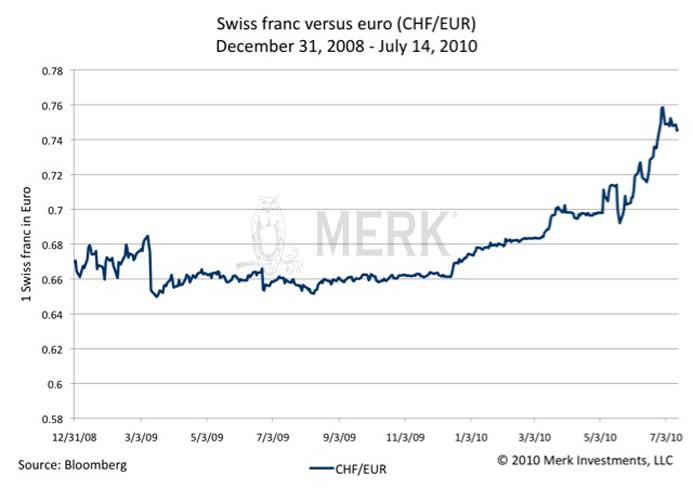

That’s a comfort for investors who, in 2015, saw the franc jump to parity with the euro in a matter of minutes after the SNB scrapped its cap on the currency. Brokers as far away as New Zealand went out of business as their clients racked up hundreds of millions worth of losses.

Investors have been on high alert for another jolt ever since.

As the region grapples with the fallout from the pandemic, banks are assessing the triggers that could send the franc roaring against the common currency. A key one is any additional strains on the finances of highly indebted nations such as Italy, something that may be alleviated by the promise of EU-backed financing.

“Today’s bullish euro price action is consistent with our view that a viable coordinated euro-zone fiscal response involving some kind of intra- eurozone fiscal transfer could be a game changer for the euro and euro-swiss fortunes. We still need the EU 27 to unanimously agree” to the proposals, “but this is a first step in the right direction.”

At the start of the year, investors were bearish about the euro’s prospects against the franc, but that’s accelerated significantly since the coronavirus spread across the globe. Demand, meanwhile, is growing for insurance against further swings in the franc against the dollar.

The isn’t much the SNB can do about the currency’s “direction until the ECB starts tightening and that is light years away,” said Kenneth Broux, a strategist at Societe Generale SA in London. “All it might take is a second wave of Covid-19 after the summer and we could be drifting closer to parity with the euro by year end.”

— With assistance by Tom Keene, Francine Lacqua, Zoe Schneeweiss, and Vassilis Karamanis

PHLX Swiss Franc Index (XDS) - Investing.com

Swiss Franc (CHF USD) Traders Betting Against the House May Win - Bloomberg

Guide to Dollar/ Swiss Franc Spread Betting

FOREX- Swiss franc drops to 2-month low, dollar bounces to 2-week high

IC Markets Covering 90% of Client Negative Losses from Swiss Franc ...

Also see:

Contact

Website Terms & Conditions

Privacy Policy

About Us

Press Releases

Spreads

Typically 70-80% of retail investors lose money when trading CFDs and spread bets. You should consider whether you can afford to take the high risk of losing your money.

† Spreads in market hours. * Tax treatment depends on the individual circumstances of each client and may change in the future.

The information and comments provided herein should not be considered as an offer or solicitation to invest. Under no circumstances should anything herein to be construed as investment advice. The information provided is believed to be accurate at the date the information is produced.

The information on this site is not directed at residents of the United States or any particular country outside the UK and is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

Apple, iPad and iPhone are trademarks of Apple Inc. which are registered in the USA and other countries. App Store is a service mark of Apple Inc., Android is a trademark of Google Inc., and Google Play is a trademark of Google Inc.

© Copyright Financial Spreads 2007-2021. All rights reserved.

The information and comments provided herein under no circumstances are to be considered an offer or solicitation to invest and nothing herein should be construed as investment advice. The information provided is believed to be accurate at the date the information is produced.

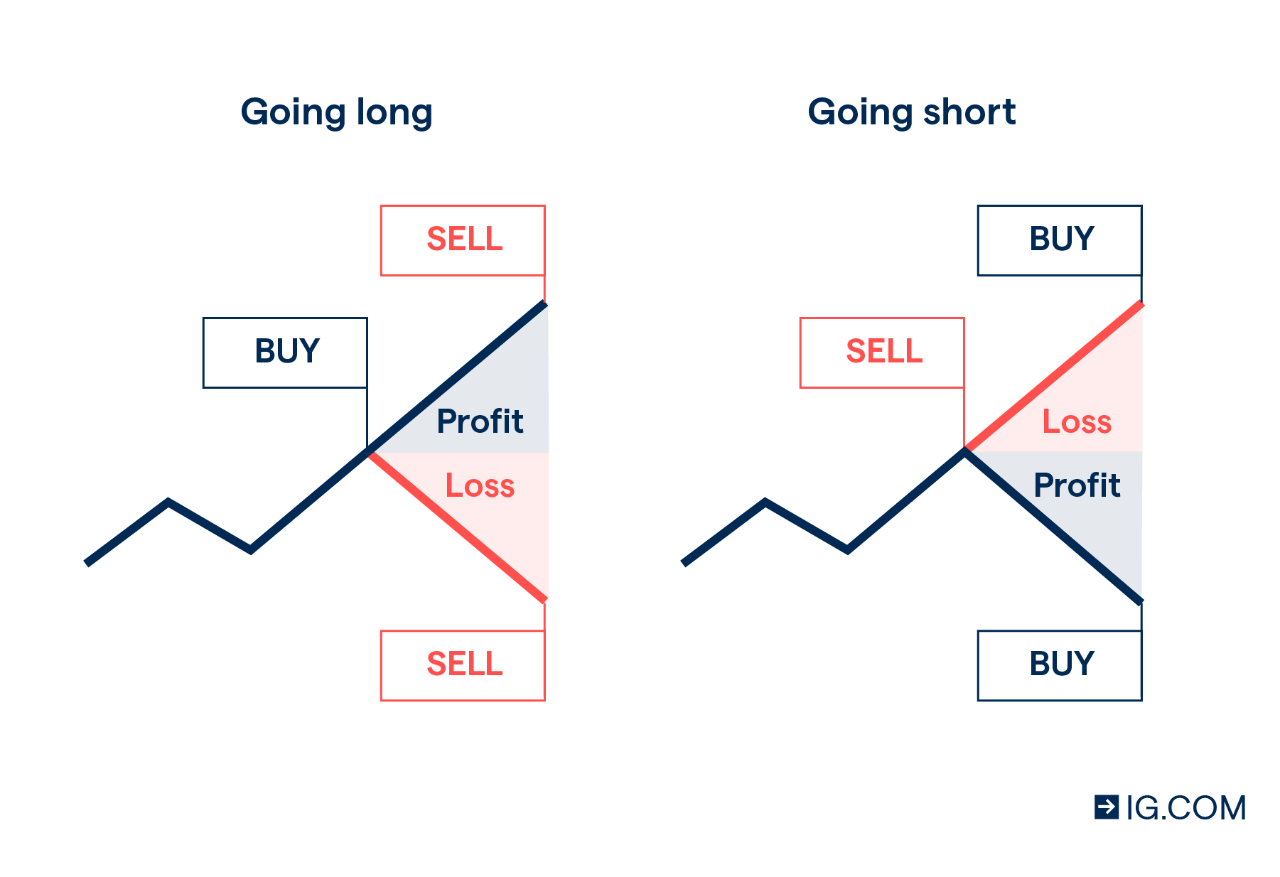

Now you can trade on the USD/CHF Rolling Spot market to push:

Higher than SFr 0.93012, or

Lower than SFr 0.92998

This is a 'Rolling' spread betting market and so there is no final closing date. If you don't close your position and the session ends then your trade will automatically roll over to the next session.

Note that if the trade is rolled over then you will either be credited or debited for overnight financing based on whether you are betting on the market to move higher or lower. For additional information also see Rolling Spread Betting .

Spread trades on the USD/CHF market are priced in £x per point.

Where a point is SFr 0.00010 of the FX market's price movement.

E.g. if USD/CHF changes by SFr 0.00500 then you would lose or gain 50 multiples of your stake.

You choose how much you want to risk per point, e.g. £1 per point, £4 per point, £10 per point etc.

For example, if you decided on a stake of £3 per point and USD/CHF moves by SFr 0.00270 (27 points), you would gain or lose £3 per point x 27 points = £81.

USD/CHF moving:

Higher than SFr 0.93012? or

Lower than SFr 0.92998?

You Select How Much to Risk, Let's Say You Choose

You will make £2 for each point (SFr 0.00010) USD/CHF increases above SFr 0.93012

You will lose £2 for every point (SFr 0.00010) USD/CHF moves below SFr 0.93012

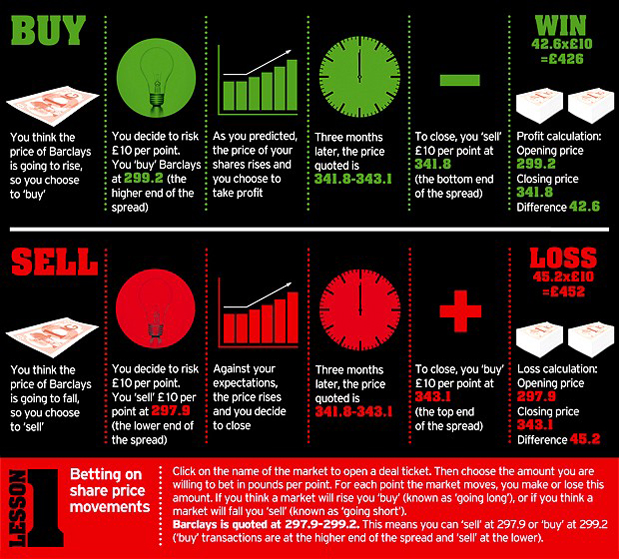

When Going Long of a Market Your P&L =

(Closing Price - Initial Price) x stake

USD/CHF increases and the market is moved to SFr 0.93640 - SFr 0.93654, so you would see:

At this point, you can decide to let your bet run or close it in order to lock in your profit. In this case you choose to close your trade by selling at SFr 0.93640.

(Closing Price - Initial Price) x stake

(SFr 0.93640 - SFr 0.93012) x £2 per point (£2 per SFr 0.00010)

USD/CHF goes lower and the spread betting market is revised to SFr 0.92454 - SFr 0.92468, i.e. on Financial Spreads you would see:

You may opt to leave your bet open or close it, i.e. close your trade and restrict your losses. In this instance you choose to settle your position and sell at SFr 0.92454.

(Closing Price - Initial Price) x stake

(SFr 0.92454 - SFr 0.93012) x £2 per point (£2 per SFr 0.00010)

USD/CHF to go:

Higher than SFr 0.93012? or

Lower than SFr 0.92998?

You Decide Your Stake Size, Let's Say You Select

You will lose £3 for every point (SFr 0.00010) USD/CHF increases higher than SFr 0.92998

You will make £3 for every point (SFr 0.00010) USD/CHF falls lower than SFr 0.92998

If You Are Speculating on a Market to Go Down Your P&L =

(Initial Price - Closing Price) x stake

USD/CHF moves lower and the spread trading market moves to SFr 0.92639 - SFr 0.92653, therefore you would see this on Financial Spreads:

At this point, you can choose to let your position run or close it in order to lock in a profit. In this example you opt to close your position by buying the market at SFr 0.92653.

(Initial Price - Closing Price) x stake

(SFr 0.92998 - SFr 0.92653) x £3 per point (£3 per SFr 0.00010)

USD/CHF moves higher and the financial spread betting market is revised and moved to SFr 0.93291 - SFr 0.93305. I.e.

You may choose to let your spread bet run or close it, i.e. close your position and restrict your loss. In this example you decide to settle your trade and buy at SFr 0.93305.

(Initial Price - Closing Price) x stake

(SFr 0.92998 - SFr 0.93305) x £3 per point (£3 per SFr 0.00010)

Percent of Open Interest for Each Category of Trader

Oral Orgasm Porn

Deepthroat Overwatch

Latina Mature Double Penetration

Porno Sperm Tits

Sensual Lesbian Kiss

1200" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">1000" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">1000" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">0" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">0/Crc15Bsv7Vs/6Xu8hKcIKspA0l516Mu8kK.jpg" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">

1200" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">1000" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">1000" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">0" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">0/Crc15Bsv7Vs/6Xu8hKcIKspA0l516Mu8kK.jpg" width="550" alt="Swiss Franc Spread Betting Losses" title="Swiss Franc Spread Betting Losses">