Some Known Factual Statements About Understanding Payday Loans - Capital One

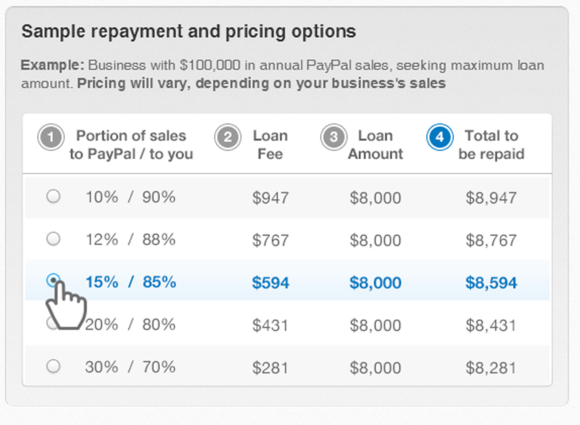

Is PayPal Working Capital Right for Your Business?

Is PayPal Working Capital Right for Your Business?Some Ideas on PayPal Working Capital Review For 2021 - SME Loans You Should Know

Along the exact same lines, simply determining the level to which payday-lending limitations affect the quantity of payday lending that takes place clarify what is currently a crucial unknown. Consumers in states that prohibit payday loaning might borrow from stores in other states, might obtain online, or may discover lending institutions willing to skirt the law.

PayPal Working Capital - Working capital loan - PayPal US

PayPal Working Capital - Working capital loan - PayPal US PayPal Working Capital Reviews – Lendvo

PayPal Working Capital Reviews – LendvoIn this paper, we take advantage of 2 recent advancements to study this question. The first is the availability of a new data set: the Federal Deposit Insurance Corporation's (FDIC's) National Survey of Unbanked and Underbanked Families, a supplement to the Existing Population Study (CPS). The study is big and nationally representative and includes detailed information about customers' loaning habits.

Second, a variety of states have actually prohibited the usage of payday advance in recent years. Through a simple difference-in-differences design, we exploit this policy variation to study the impact of changes in customers' access to payday loans in between states with time. We discover that payday-lending restrictions do not reduce the variety of people who take out alternative monetary services (AFS) loans.

The Facts About PayPal among supporters for blanket SBA PPP loan forgiveness RevealedWe also record that payday advance loan restrictions are associated with a boost in involuntary closures of consumers' checking accounts, a pattern that recommends that customers might replace from payday loans to other forms of high-interest credit such as bank overdrafts and bounced checks. In contrast, payday-lending bans have no impact on making use of traditional types of credit, such as credit cards and customer financing loans.

The paper is structured as follows. Area 2 offers background on numerous kinds of AFS credit. Area 3 evaluations specify policies of those credit products. Section 4 evaluates the literature on the relationship amongst payday advance loan access, monetary wellness, and using AFS credit products. Section 5 explains our information.

Section 7 concludes. 2. building business credit without personal guarantee . Alternative Financial Provider Credit Products, Alternative monetary services is a term used to describe credit items and other monetary services operating outside the standard banking systems. Lots of AFS credit items are high-interest loans that are gotten for brief time durations. These AFS credit products consist of payday advance, pawnshop loans, rent-to-own loans, and overdraft services.1 The following sections quickly describe these products (for more in-depth descriptions, see Caskey 1994; Drysdale and Keest 2000).