Private Funds

🔞 ALL INFORMATION CLICK HERE 👈🏻👈🏻👈🏻

Private Funds

Private equity funds are closed-end funds that are not listed on public exchanges. Their fees include both management and performance fees. Private equity fund partners are called general partners, and investors or limited partners. The limited partnership agreement outlines the amount of risk each party takes along with the duration of the fund. Limited partners are liable up to the full amount of money they invest, while general partners are fully liable to the market.

Sponsored

Compete Risk Free with $100,000 in Virtual Cash

Put your trading skills to the test with our

FREE Stock Simulator.

Compete with thousands of Investopedia traders and trade your way to the top! Submit trades in a virtual environment before you start risking your own money.

Practice trading strategies

so that when you're ready to enter the real market, you've had the practice you need.

Try our Stock Simulator today >>

Equity co-investment is made by minority investors alongside a majority institutional investor.

Two and Twenty is a typical fee structure that includes a management fee and a performance fee and is typically charged by hedge fund managers.

A hedge fund is an actively managed portfolio of investments that uses leveraged, long, short and derivative positions.

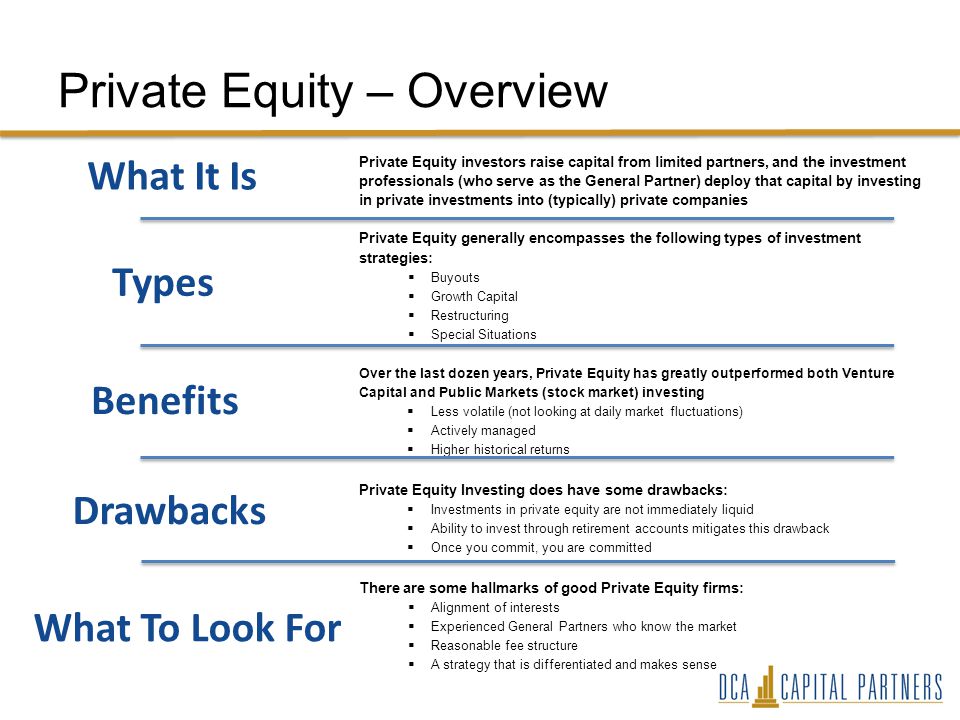

Private equity is a non-publicly traded source of capital from investors who seek to invest or acquire equity ownership in a company.

Anticipated holding period refers to the length of time a limited partnership expects to hold a specific asset.

Venture capital funds invest in early-stage companies and help get them off the ground through funding and guidance, aiming to exit at a profit.

#

A

B

C

D

E

F

G

H

I

J

K

L

M

N

O

P

Q

R

S

T

U

V

W

X

Y

Z

Investopedia is part of the Dotdash publishing family.

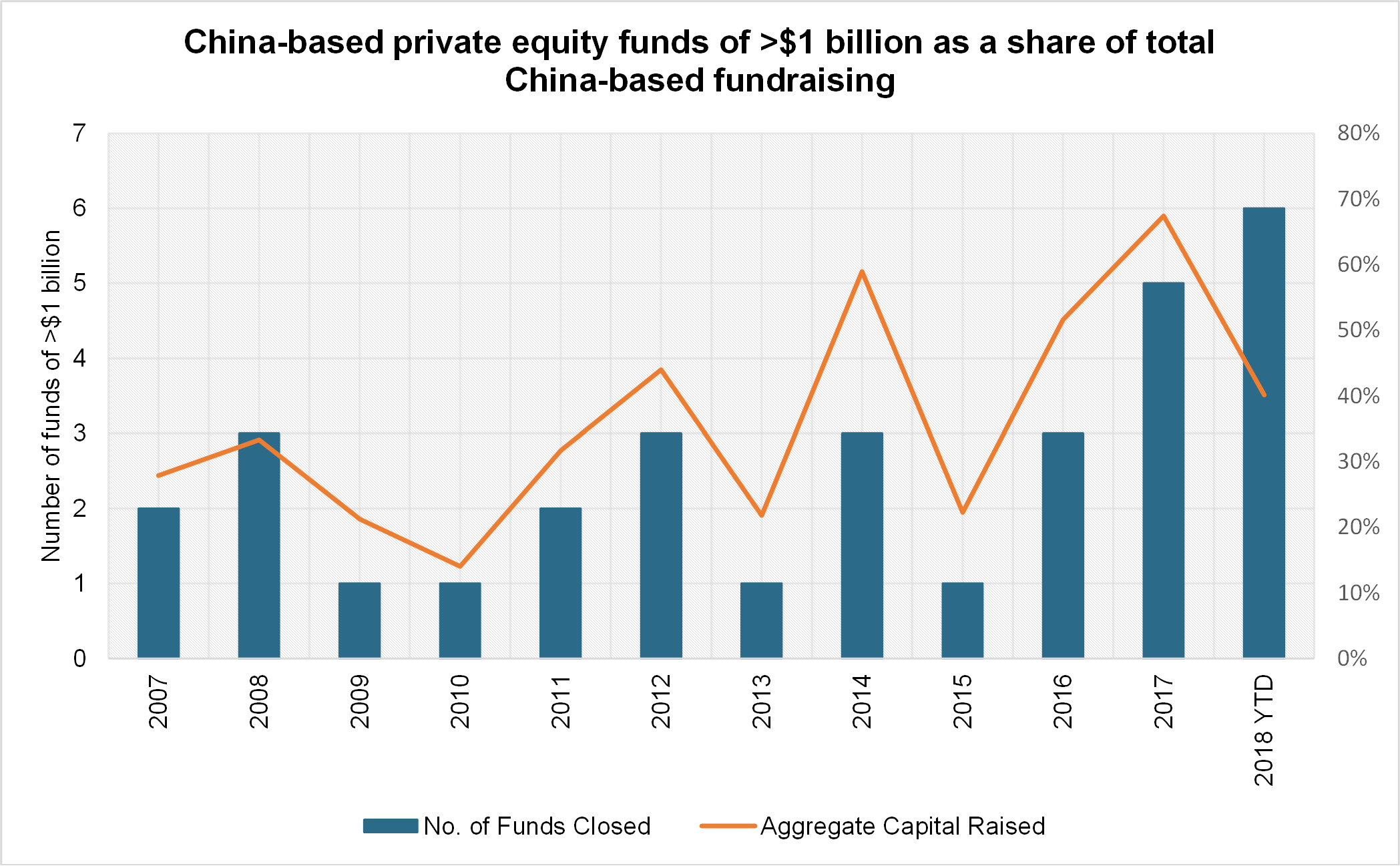

Although the history of modern private equity investments goes back to the beginning of the last century, they didn't really gain prominence until the 1980s. That's around the time when technology in the United States got a much-needed boost from venture capital .

Many fledgling and struggling companies were able to raise funds from private sources rather than going to the public market. 1 Some of the big names we know today— Apple , for example—were able to put their names on the map because of the funds they received from private equity. 2

Even though these funds promise investors big returns, they may not be readily available for the average investor . Firms generally require a minimum investment of $200,000 or more, which means private equity is geared toward institutional investors or those who have a lot of money at their disposal.

If that happens to be you and you're able to make that initial minimum requirement, you've cleared the first hurdle. But before you make that investment in a private equity fund , you should have a good grasp of these funds' typical structures.

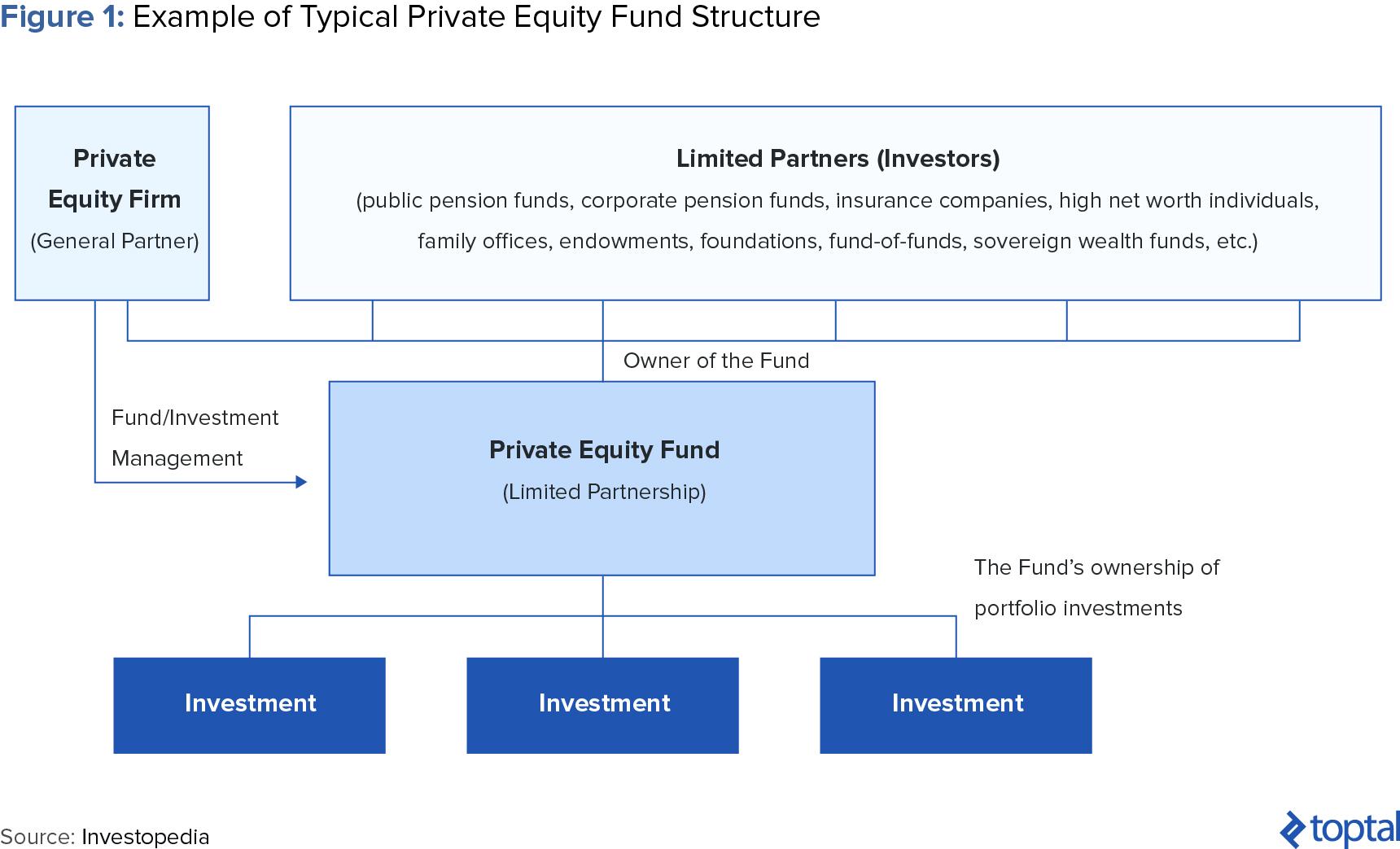

Private equity funds are closed-end funds that are considered an alternative investment class. Because they are private, their capital is not listed on a public exchange. These funds allow high-net-worth individuals and a variety of institutions to directly invest in and acquire equity ownership in companies.

Funds may consider purchasing stakes in private firms or public companies with the intention of de-listing the latter from public stock exchanges to take them private. After a certain period of time, the private equity fund generally divests its holdings through a number of options, including initial public offerings (IPOs) or sales to other private equity firms.

Unlike public funds, the capital of private equity funds is not available on a public stock exchange.

Although minimum investments vary for each fund, the structure of private equity funds historically follows a similar framework that includes classes of fund partners, management fees, investment horizons , and other key factors laid out in a limited partnership agreement (LPA).

For the most part, private equity funds have been regulated much less than other assets in the market. That's because high-net worth investors are considered to be better equipped to sustain losses than average investors. But following the financial crisis , the government has looked at private equity with far more scrutiny than ever before. 3

If you're familiar with the fee structure of a hedge fund, you'll notice it's very similar to that of the private equity fund. It charges both a management and a performance fee.

The management fee is about 2% of the capital committed to invest in the fund. So a fund with assets under management (AUM) of $1 billion charges a management fee of $20 million. This fee covers the fund's operational and administrative fees such as salaries, deal fees—basically anything needed to run the fund. As with any fund, the management fee is charged even if it doesn't generate a positive return.

The performance fee , on the other hand, is a percentage of the profits generated by the fund that are passed on to the general partner (GP). These fees, which can be as high as 20%, are normally contingent on the fund providing a positive return. The rationale behind performance fees is that they help bring the interests of both investors and the fund manager in line. If the fund manager is able to do that successfully, they are able to justify his performance fee.

Private equity funds can engage in leveraged buyouts (LBOs), mezzanine debt , private placement loans, distressed debt, or serve in the portfolio of a fund of funds. While many different opportunities exist for investors, these funds are most commonly designed as limited partnerships.

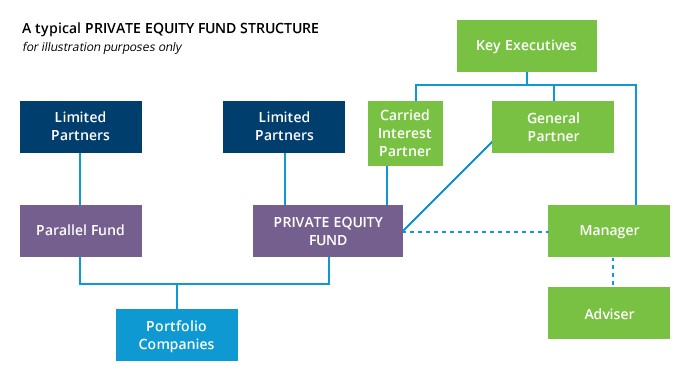

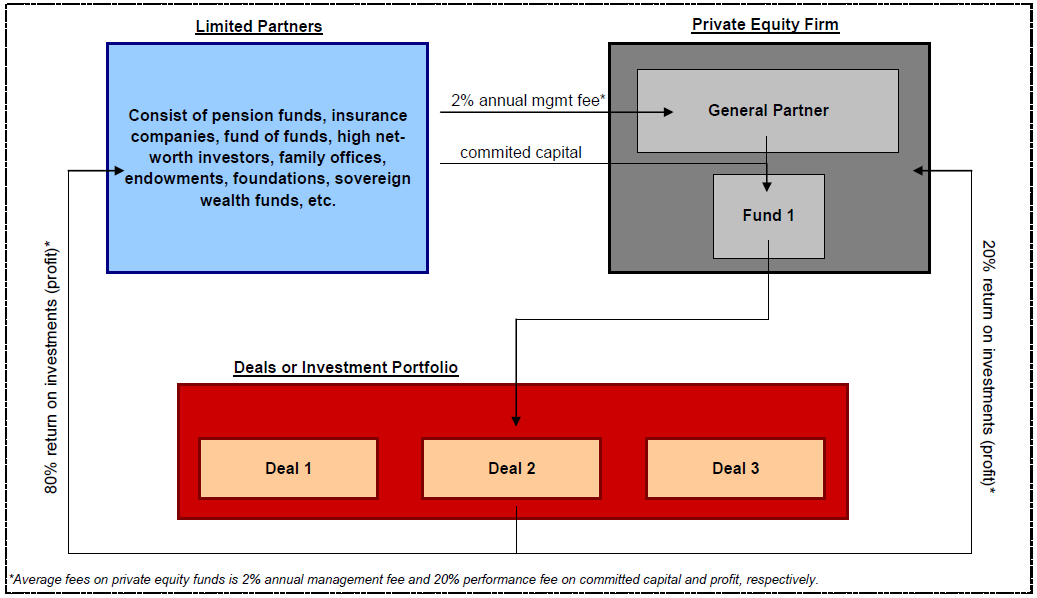

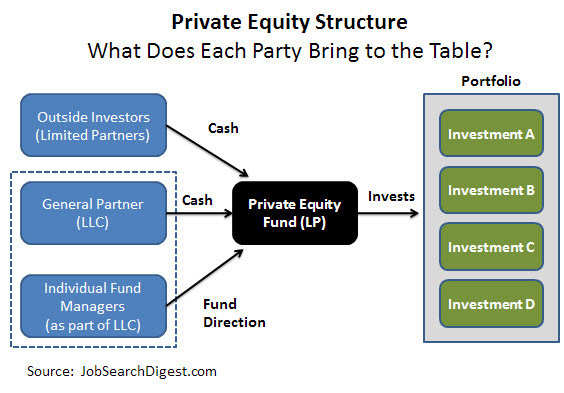

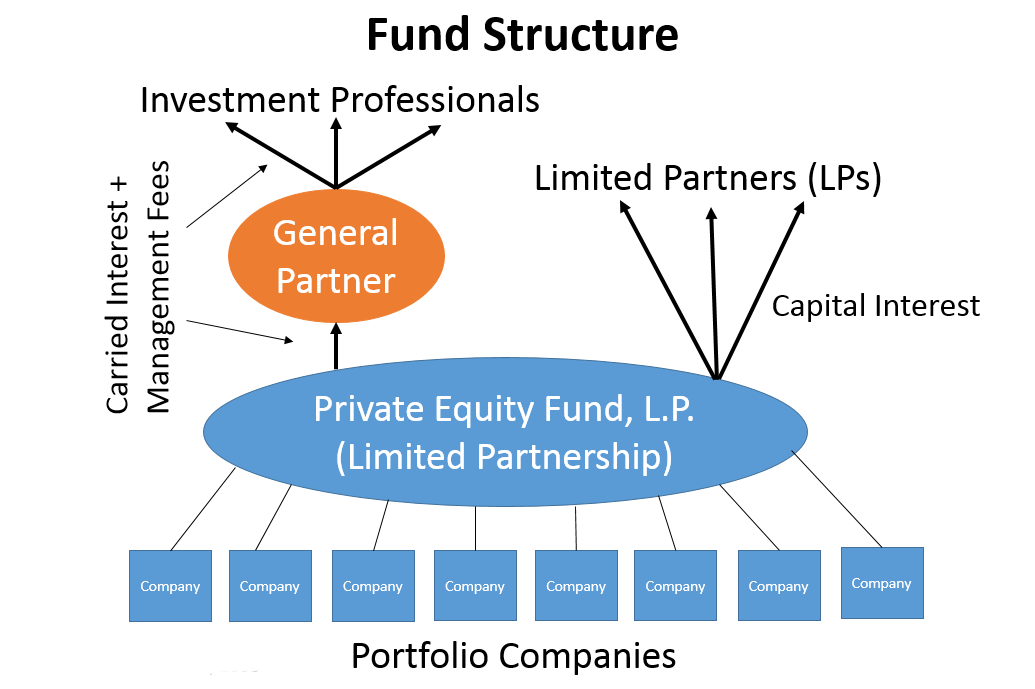

Those who want to better understand the structure of a private equity fund should recognize two classifications of fund participation. First, the private equity fund’s partners are known as general partners. Under the structure of each fund, GPs are given the right to manage the private equity fund and to pick which investments they will include in its portfolios. GPs are also responsible for attaining capital commitments from investors known as limited partners (LPs). This class of investors typically includes institutions—pension funds, university endowments, insurance companies—and high-net-worth individuals.

Limited partners have no influence over investment decisions. At the time that capital is raised, the exact investments included in the fund are unknown. However, LPs can decide to provide no additional investment to the fund if they become dissatisfied with the fund or the portfolio manager .

When a fund raises money, institutional and individual investors agree to specific investment terms presented in a limited partnership agreement. What separates each classification of partners in this agreement is the risk to each. LPs are liable up to the full amount of money they invest in the fund. However, GPs are fully liable to the market, meaning if the fund loses everything and its account turns negative, GPs are responsible for any debts or obligations the fund owes.

The LPA also outlines an important life cycle metric known as the “Duration of the Fund.” PE funds traditionally have a finite length of 10 years, consisting of five different stages:

Private equity funds typically exit each deal within a finite time-period due to the incentive structure and a GP's possible desire to raise a new fund. However, that time-frame can be affected by negative market conditions, such as periods when various exit options , such as IPOs, may not attract the desired capital to sell a company.

Notable private equity exits include Blackstone Group's (BX) 2013 IPO of Hilton Worldwide Holdings (HLT) that provided the deal's architects a paper profit of $8.5 billion. 4

Perhaps the most important components of any fund’s LPA are obvious: The return on investment and the costs of doing business with the fund. In addition to the decision rights, the GPs receive a management fee and a “carry.”

The LPA traditionally outlines management fees for general partners of the fund. It's common for private equity funds to require an annual fee of 2% of capital invested to pay for firm salaries, deal sourcing and legal services, data and research costs, marketing, and additional fixed and variable costs . For example, if a private equity firm raised a $500 million fund, it would collect $10 million each year to pay expenses. Over the duration of the 10-year fund cycle, the PE firm collects $100 million in fees , meaning $400 million is actually invested during that decade.

Private equity companies also receive a carry, which is a performance fee that is traditionally 20% of excess gross profits for the fund. Investors are usually willing to pay these fees due to the fund's ability to help manage and mitigate corporate governance and management issues that might negatively affect a public company.

The LPA also includes restrictions imposed on GPs regarding the types of investment they may be able to consider. These restrictions can include industry type, company size, diversification requirements, and the location of potential acquisition targets. In addition, GPs are only allowed to allocate a specific amount of money from the fund into each deal it finances . Under these terms, the fund must borrow the rest of its capital from banks that may lend at different multiples of a cash flow, which can test the profitability of potential deals.

The ability to limit potential funding to a specific deal is important to limited partners because several investments bundled together improves the incentive structure for the GPs. Investing in multiple companies provides risk to the GPs and could reduce the potential carry, should a past or future deal underperform or turn negative.

Meanwhile, LPs are not provided with veto rights over individual investments. This is important because LPs, which outnumber GPs in the fund, would commonly object to certain investments due to governance concerns, particularly in the early stages of identifying and funding companies. Multiple vetoes of companies may educe the positive incentives created by the commingling of fund investments.

Private-equity firms offer unique investment opportunities to high-net-worth and institutional investors . But anyone who wants to invest in a PE fund must first understand their structure so they are aware of the amount of time they will be required to invest, all associated management and performance fees, and the liabilities associated.

Typically, PE funds have a 10-year duration, require 2% annual management fees and 20% performance fees, and require LPs to assume liability for their individual investment, while GPs maintain complete liability.

private funds - это... Что такое private funds ?

Private Equity Fund Structure

Private Equity Funds - Know the Different Types of PE Funds

PEI 300 | Top private equity firms | Private Equity International

private funds - Translation into Russian - examples... | Reverso Context

Pools of capital invested in private companies

We and selected partners, use cookies or similar technologies as specified in the cookie policy . With respect to advertising, we and selected third parties , may use precise geolocation data and actively scan device characteristics for identification in order to store and/or access information on a device and process personal data (e.g. browsing data, IP addresses, usage data or unique identifiers) for the following purposes: personalised ads and content, ad and content measurement, and audience insights; develop and improve products . You can freely give, deny, or withdraw your consent at any time by accessing the advertising preferences panel . You can consent to the use of such technologies by closing this notice.

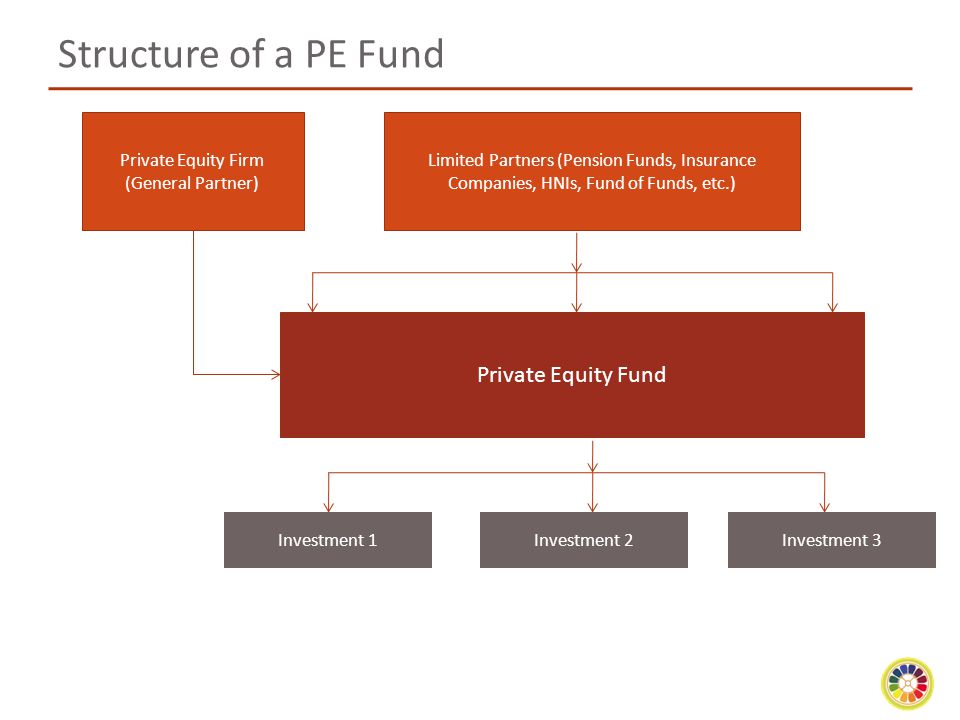

Private equity funds are pools of capital to be invested in companies that represent an opportunity for a high rate of return. They come with a fixed investment horizon Return on Investment (ROI) Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments. , typically ranging from four to seven years, at which point the PE firm hopes to profitably exit the investment. Exit strategies include IPOs Initial Public Offering (IPO) An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Prior to an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors). Learn what an IPO is and sale of the business to another private equity firm or strategic buyer.

Institutional funds and accredited investors usually make up the primary sources of private equity funds, as they can provide substantial capital for extended periods of time. A team of investment professionals from a particular PE firm raises and manages the funds.

Equity can be further subdivided into four components: shareholder loans, preferred shares, CCPPO shares, and ordinary shares.

Typically, the equity proportion accounts for 30% to 40% of funding in a buyout. Private equity firms tend to invest in the equity stake with an exit plan of 4 to 7 years. Sources of equity funding include management, private equity funds, subordinated debt holders, and investment banks. In most cases, the equity fraction is comprised of a combination of all these sources.

Private equity funds generally fall into two categories: Venture Capital and Buyout or Leveraged Buyout.

Venture capital Venture Capital Venture capital is a form of financing that provides funds to early stage, emerging companies with high growth potential, in exchange for equity or an ownership stake. Venture capitalists take the risk of investing in startup companies, with the hope that they will earn significant returns when the companies become a success. funds are pools of capital that typically invest in small, early stage and emerging businesses that are expected to have high growth potential but have limited access to other forms of capital. From the point of view of small start-ups with ambitious value propositions and innovations, VC funds are an essential source to raise capital as they lack access to large amounts of debt. From the point of view of an investor, although venture capital funds carry risks from investing in unconfirmed emerging businesses, they can generate extraordinary returns.

Contrary to VC funds, leveraged buyout funds invest in more mature businesses, usually taking a controlling interest. LBO Leveraged Buyout (LBO) A leveraged buyout (LBO) is a transaction where a business is acquired using debt as the main source of consideration. An LBO transaction typically occur when a private equity (PE) firm borrows as much as they can from a variety of lenders (up to 70-80% of the purchase price) to achieve an internal rate return IRR >20% funds use extensive amounts of leverage to enhance the rate of return. Buyout finds tend to be significantly larger in size than VC funds.

There are multiple factors in play that affect the exit strategy of a private equity fund. Here are some necessary questions to ask:

When deciding to exit, PE firms take either one of two paths: total exit or partial exit. In terms of a wholesale exit from the business, there can be a trade sale to another buyer, LBO by another private equity firm, or a share repurchase.

In terms of a partial exit, there could be a private placement, where another investor purchases a piece of the business. Another possibility is corporate restructuring, where external investors get involved and increase their position in the business by partially acquiring the private equity firm’s stake. Finally, corporate venturing could happen, in which the management increases its ownership in the business.

Lastly, a flotation or an IPO is a hybrid strategy of both total and partial exit, which involves the company being listed on a public stock exchange. Typically, only a fraction of a company is sold in an IPO, ranging from 25% to 50% of the business. When the company is listed and traded publicly, private equity firms exit the company by slowly unwinding their remaining ownership stake in the business.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ FMVA® Certification Join 350,600+ students who work for companies like Amazon, J.P. Morgan, and Ferrari certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

Advance your career in investment banking, private equity, FP&A, treasury, corporate development and other areas of corporate finance.

to take your career to the next level! Learn step-by-step from professional Wall Street instructors today.

Trans Nasty

Nerd X Jock

Voyeur Pee Forums

Beautiful Collection Of Nude Nudists Photo

Flash Dick Car Xhamster

:max_bytes(150000):strip_icc()/dotdash_Final_Private_Equity_Apr_2020-01-3ce99c81ce344ddc94fe05b17a2b7716.jpg)