Poker Variance Calculator | Primedope

=============

Регистрируйся и получи бонус до 50000 рублей!

✅ Ссылка: 1WIN.COM

🔥 Промокод для СУПЕРБОНУСА: TELEGRAPHBONUS

💰 Раздача ваучеров до 1000 рублей: t.me/onewin_vauchers.

=============

Poker Variance Calculator

Poker Variance Calculator for cash games. Displays variance, possible downswings, upswings and probabilities depending on your win rate.

Settings

Онлайн калькулятор покер

Winnings in BB on right axis, current downswing in BB on left axis. Depending on the number of hands displayed, the extent and number of downswings may be underrepresented due to the resolution of the graph.

This section will explain how the calculator works and what the numbers and charts mean.

Enter the data

Settings

Hop over to the Variance Calculator page and enter your win rate, standard deviation and the number of hands you want to simulate. You can ignore the field observed win rate, we’ll get to its purpose later. Once you have entered the data, hit Calculate and let the Calculator do its magic.

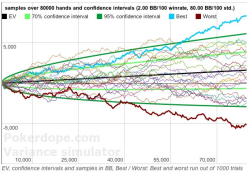

20 samples

Variance Calculator Samples

The first thing the Variance Calculator does is to run 20 samples over the number of hands, win rate and standard deviation specified. It’ll also calculate the expected winnings over the number of hands. This number will appear as a rather boring straight and black line in the graph. Thirdly the calculator displays the 70% and 95% confidence intervals as light and dark green curves. What you need to know about them is that at any given time your winnings will be within these intervals with a probability of 70% and 95% respectively. They basically show, how much variance you should expect to see.

Variance in numbers

Below the first chart the Variance Calculator compiles a neat list of additional information:

- EV: win rate entered above

- Standard deviation: standard deviation entered above

- Hands: number of hands entered above

- Expected winnings: estimated winnings over the simulated amount of hands

- Standard deviation after X hands: This number shows how much your actual results will differ from the expected results on average. The first number shows the absolute value and the second translates this number into BB/100, showing the impact on your win rate.

- 70% confidence interval: Your actual results over the simulated amount of hands will be within this interval 70% of the time. The first interval shows absolute numbers and the second translates those into BB/100, showing the 70% confidence interval for your win rate.

- 95% confidence interval: Same as the above with 95% certainty. Meaning: 19 out of 20 times your actual winnings will be within this interval.

- Probability of loss after X hands: probability that you will experience negative winnings (meaning: losses) over the number of hands.

- Probability of running at or above observed win rate …: If you entered an observed win rate, this number will show you the probability that you will experience a run at or above this win rate over the number of hands.

- Probability of running below observed win rate …: Same as above – probability that you will experience a run below the observed win rate over the number of hands.

- Minimum bankroll for less than 5% risk of ruin: the bankroll needed to have a risk of ruin of less than 5%

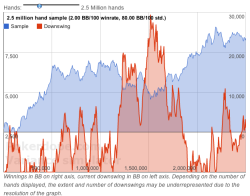

Detailed sample with downswing

Variance Calculator Downswing Samples

This chart simulates a single run over 100 thousand up to 10 million hands with the win rate and standard deviation entered above. You can choose how many hands to simulate by moving the slider.

Apart from showing a single sample, this graph also shows some insightful information about downswings. The red area shows for any given point, how much the sample is currently away from its previous peak, meaning it tracks downswings. This chart uses two vertical axes. While the sample winnings have their scale on the right axis, the downswing tracker has its scale on the left axis. In this example, the simulated player ended up with winnings over 25,000 big blinds after 2.5 million hands but had to deal with a nasty downswing of almost 10,000 big blinds between hand 1.2 million and hand 2 million.

Downswings in numbers

The last section of the Variance Calculator sheds some more light on potential downswings. Therefore 100 million hands are simulated and all downswings over this simulation are tracked. The first table shows the extent of downswing. It shows how often the simulated player was stuck in a downswing of at least X big blinds. For example (1000+ BB – 31.77%) means the player was in the middle of a downswing of at least 1,000 big blinds 31.77 percent of the time.

The second table shows how long downswings last on average. For example (50000+ Hands – 15.81%) means the simulated player was in a downswing over at least 50,000 hands 15.81 percent of the time. For the purpose of these calculations, a downswing is defined as any period where the current total winnings are below the maximum previous total winnings. Meaning, that by this definition a downswing is not over until the player has fully recovered its losses.

In general, these simulations underestimate the extent of downswings, but the numbers should still give you a decent idea of the vastness of downswings you should expect.

Should you have any questions, encounter any errors or have ideas for improvements, please let me know.

fix your site all the numbers are wrong they are impossible

What do you mean exactly?

hey, the ‘Downswings in numbers’ section is not working,thankyou verymuch!

Yes, I think I broke it accidentally a few days ago. :O Will be fixed within a few days.

please repair ___)))

I am a part of digital marketing strategy.We are providing the quality sites for guest posts. a If you are looking for guest posts sites ? then you are in the right place.

This guest post strategy increases your website traffic and visitors.

Just let me know which sites you are interested in and I will provide you my best.

Would it be possible to get the ability to set a target risk of ruin?

it would be really awesome if there was an option to input a bankroll amount and calculate the risk of ruin based on the input bankroll

You can calculate BR for RoR directly…

BR for 5% RoR = 1.5 * (std.dev)^2 / WR

For different RoRs, simply multiply by ln(RoR)/ln(.05)

So, 10 bb/100 WR at 100 bb/100 std. dev would result in:

1.5 * (100)^2 / 10 = 1500 bbs bankroll for 5% RoR

for 10% RoR, multiply by ln(.1)/ln(.05) = .7686

1500 * .7686 = 1153 bbs bankroll for 10% RoR

Hi would you be willing to add 3 sigma(99.7 %) below 70% and 95% confidence interval (»?«) ?

What kind of stochastic process do you use to make these simulations?

Hi Torsten, the calculator runs rather simple Monte Carlo simulations assuming that cash game results follow the normal distribution when repeated often enough and over a long enough time frame.

Great job on the tool! Maybe you could add an input box for rake or give choice to choose site / limits, tough of course it’s possible to just add the rake back to our win rate. Cheers

For variance purposes you should always consider your win rate with rake (and possible rake back) included.Otherwise you’d heavily overestimate your EV and underestimate the variance.

Is it possible to get Risk for ruin shown to 0%?

Is it possible to get it shown over a hand period?

A 0% risk of ruin at infinity is unachievable unless one starts with an infinite BR.

For risk of ruin shown over a hand period you can use the formula I gave in the comment below.

Sorry, where’s the formula?

The risk of ruin you show is only at infinity, not for finite time.

R = risk of ruin

s = standard deviation per hand = (standard deviation per 100) / 10

m = bb/hand

br = initial bankroll

Then the risk of ruin after n hands is given by:

R = 1 + exp(-2*m*br/s^2)*Phi((br + m*n)/sqrt(n*s^2)) – Phi((-br + m*n)/sqrt(n*s^2))

where Phi(x) is the standard normal cdf.

You can see that as n goes to infinity, R becomes the formula you use exp(-2*m*br/s^2).

Hi, adelarosa, thanks for your great answer.

Could you please provide a reference for the stated formula for finite n? I am eager to learn the fundamentals of this kind of computations.

I have also attached a derivation I did a while ago.

can you do a version in spanish?? i

Unfortunately, right now there are no international version planned.

Thank you for this, it’s awesome I can see there’s a lot of time and effort that’s gone into it. Really cool.

Is there a calc that does this that shows the same but without rake?

Perhaps I’m missing the point but that would be a different curve no? Less Variance more winning?

Well, yes, you can just add the rake to you win rate to see the difference. If you have a win rate of 3BB/100 and pay 5BB/100 rake, your win rate before rake is 8BB/100.

The variance is independent of your win rate though. Of course your EV will increase, but the size of the confidence intervals for example will stay the same.

Hi – does anyone know the standard deviation of evBB/100 hands for 6max no-limit? Seems like it should be less than the SD of winrates that aren’t adjusted for all-in equity.

Standard Deviation heavily depends on your play style. More aggressive players tend to have much higher SD/100 than super tight players.

I just went through my database with a couple of million cash game hands to get some detailed numbers about the standard deviation of all players in the database. (Regular cash game, not fast fold.) I filtered for number of players and removed all players with less than 1000 hands.

Those are the standard deviations the players in my database had:

Games with 2 players

- Median Standard Deviation: 93

- 95% Interval: 62 – 156

Games with 6 players

- Median Standard Deviation: 86

- 95% Interval: 56 – 140

Games with 9 players

- Median Standard Deviation: 86

- 95% Interval: 57 – 144

95% Interval means that 95% of all players had a standard deviation between those two values.

As you can see, standard deviation doesn’t change much between 9 player games and 6 player games.

Edit: This didn’t really answer your question though.

Go into detail regarding the standard deviation when looking at evBB/100 is a bit tricky. Unfortunately, PokerTracker doesn’t have a StdDev(evBB/100) readily available.

But I think we can get a decent approximation when we just remove all hands with an all-in and call before the river when calculating the standard deviation. At least this will show the maximum impact all in hands have on the standard deviation.

In my database I have 3.06 Million hands (NL100) with 5 or 6 players. Only 29k of those (0.9%) had an all in before the river and a showdown.

Again I filtered for all player with at least 1k hands and removed all hands with all in before the river & showdown. Those are the numbers I got:

Hands with all in & showdown: 29,350

Hands without all in & showdown: 3,058,874

- Median Standard Deviation for hands without an all in & showdown: 67

- 95% Interval: 41 – 112

Meaning: We can compare this with the numbers above for Games with 6 players. StdDev(evBB/100) is at most 28BB/100 lower than StdDev(BB/100), on average not more than 19BB/100 lower.

Great, thanks for the prompt reply!

Thank you for that amazing tool, this is great ! 🙂

The simulator is not working. It’s blocked at 1 million hands.

Fixed. Should work now again.

it doesnt work! cant calculate anything!

Weird. I cleared the cache just in case. It should work. Try hard reloading the page (Ctrl-Shift-R) and see if that helps.

“In general these simulations underestimate the likelyhood and extent of downswings” Why is that?

Generally because players tend to play worse during down swings. Lower win rates drastically increase the Likelihood of extended down swings.

the number of tables change the results of the calculator? for how many tables is calculated the variance on this site?

What about rake and fee? Is it calculated?

Yes. The rake is already considered in the win rate. Your win rate should always be after the rake.

Hello, how identify “Winrate in BB / 100”?

Is it my EV?

“Winrate / 100” means how much you win over the course of 100 hands statistically. Winnings are measured in big blinds. Lets say you’ve played 10,000 hands of $1 / $2 NLH and won $500. That means you have won 250 big blinds over 10,000 hands. This is equal to 2.5 big blinds per 100 hands.

How do you calculate standard deviation after X hands?

standard deviation is constant, and for 6max cash is betwine 100-120

the standard deviation for a single outcome is always constant. What youre looking for is the standard deviation for the mean.

It follows the following formula:

Variance of the mean result after N hands = (1/(N squared)) * Variance of the sum

N would be the number of hands and the “variance of the sum” would be the sum of the variances of all the outcomes.

For example the variance for a single fair coin flip is 0.25. If you want to know the variance of the sum of 10 coin flips you do 0.25 * 10 = 2.5

2.5 is the variance of the sum of 10 coin flips.

The same goes for poker hands. The variance for 100 poker hands in NLH 6max is, say, 10000 (100 squared).

To calculate the variance of the sum for 10 thousand hands you have to think how many groups of 100 hands does 10000 have? well, 10000/100 = 100

There are 100 groups of 100 hands in 10000 hands, which also means there is 100 times the variance of the sum of 100 hands, so:

100 * 10000 = 1000000

One million is the variance of the sum of 10000 hands. You divide this number by N squared(10000 squared) and you get the variance of the mean:

1000000 / 100000000 = 0.01

0.01 is the variance of the mean for 10000 hands; which is the same as saying 0.01 is how much your observed results will differ from the mean when looking at a sample of 10000 hands.

as you increase the number of hands the variance of the mean approaches zero:

for 10000 hands = 0.01

for 100000 hands = 0.001

for 1000000 hands = 0.0001

etc.

Btw, industry standard is to use BB to describe “big bets” and bb to describe (big blinds). Everything is super misleading.

dont know in what industri is BB for big bets

sure maybe 45 years ago lol

hi

do i need to use ev adjusted winrate or winnings winrate? i am asking cause i am running way above ev at the moment.

thanks

Hi, using your adjusted winrate makes the results more accurate.

hi, can you explain me?

No. Did you forget that the Gamblking Theory book states:

Special Note: It has been pointed out to me by Bruce Zastera, one of the most knowledgeable posters on our forums at http://www.twoplustwo.com, that it is also possible to go broke before reaching the number of hours at which we evaluate the probability of a loss, as well as after that time, and this problem is more acute at the 95 percent level than I originally realized. This means that these tables are significantly underestimating by a factor of about 2 the amount of bankroll needed to only have a 5 percent chance of going broke. Fortunately, this problem mitigates as the probability of going broke is reduced. Thus the Bankroll Required to Assure a Win tables do contain solid estimates and produce a risk of ruin of approximately 1.1 percent, but the 95 percent tables should probably not be used.

Of course I didn’t forget that note. I wrote some of it. It in no way changes the fact that the calculations in that section are no way to compute the bankroll requirement for a desired risk of ruin. That’s because the number of sigmas in your derivation does not translate to a probability of ruin, for the same reason that the 95% confidence interval in this blog has nothing to do with a 5% risk of ruin. Moreover, this fundamental problem does not “mitigate as the probability of going broke is reduced”. Your computation for the “bankroll required to assure a win” ignores 88% of the possible ways we can go broke. That number gets worse as the risk of ruin is reduced. I’m sure you understand that a mathematical model should capture the dominant effects rather than ignoring the dominant effect.

We need to be clear what was meant by “the problem mitigates as the probability of going broke is reduced”. The bankroll needed for a 5% risk of ruin is about 2.2 times the bankroll that your method would compute. If we want a 1% risk of ruin, the bankroll required is about 2 times what your method would compute. If we want a 0.13% risk of ruin, the bankroll required would be about 1.5 times what your method would compute. That’s about as small a risk of ruin as most people would care about, yet the bankroll is still off significantly. There’s not a lot of mitigation.

The actual risk of ruin produced by your bankroll in that last case, which you describe as “the bankroll required to assure a win”, would be about 1.1%, not 0.13%. The mitigating factor is that both of those numbers are relatively small. Lots of folks may not care if their risk of ruin is 1.1% or 0.13%, though I’m not sure everyone would describe a 1.1% risk of ruin as having assured a win. The 0.13% came from 3 standard deviations. You chose that as a way to include essentially all of a population as is common in statistics. Except you are considering the wrong population. We don’t want the population of positive results at a particular point in time assuming we can play through any draw down. We want the population of all random walks that never go broke. Using the former population for bankroll requirements and risk of ruin is mathematical nonsense.

BTW, the formula Pokerdope posted was well known long before Mathematics of Poker by Chen and Ankenman. It has been discussed by many at 2+2 since I introduced it there in the early 2000s or possibly even the late 1990s. It also appears in Douglas Zare’s poker book. Before that it was well known to the blackjack community, having appeared in papers by George C. and Patrick Sileo in 1989 and 1990 respectively . It was surely known in mathematics before that as the general expression is important in financial math, and it can also be obtained from the Weiner process. Deriving it from scratch isn’t that hard, but if you want a rigorous examination of the conditions under which it applies and how to modify it when those conditions don’t apply, see the essay “Gambler’s Ruin Revisited” in the book Optimal Play. There is also an analytical short term ruin formula for risk of ruin in a finite number of hands. I’ve only recently found a derivation of that one, and it is quite involved but still fairly accessible. Of course it’s quite straightforward to simulate these results to verify the accuracy of the formulas under a variety of conditions.

Variance Calculator Downswing Samples

Похожие статьи

Tournament Variance Calculator | Primedope

Отзывы игроков о Фонбет букмекерская контора - Рейтинг Букмекеров

Пятёрка лучших онлайн-покеристов России - Все о жизни покериста - Блоги.

Как работает онлайн казино Вулкан?

Реально ли выиграть в казино вулкан?

Онлайн-казино Поинт | Форум - Крупнейший форум игроков в онлайн казино

Казино ПоинтЛото - лучшее место для игры в автоматы в России | - развлекательный портал

Муж играет в онлайн казино - 309 ответов - Семья и семейные отношения - Форум Дети

Как выводить деньги с казино вулкан - Жизнь Игра - Блоги.

Самое честное проверенное онлайн казино по выплатам с выводом денег Октябрь 2022