NVIDIA Earnings May 20 — The Falsification Framework

The Durability Curve

Subscribe to The Durability Curve on Substack — free weekly analysis on AI infrastructure, verification, and durable systems.

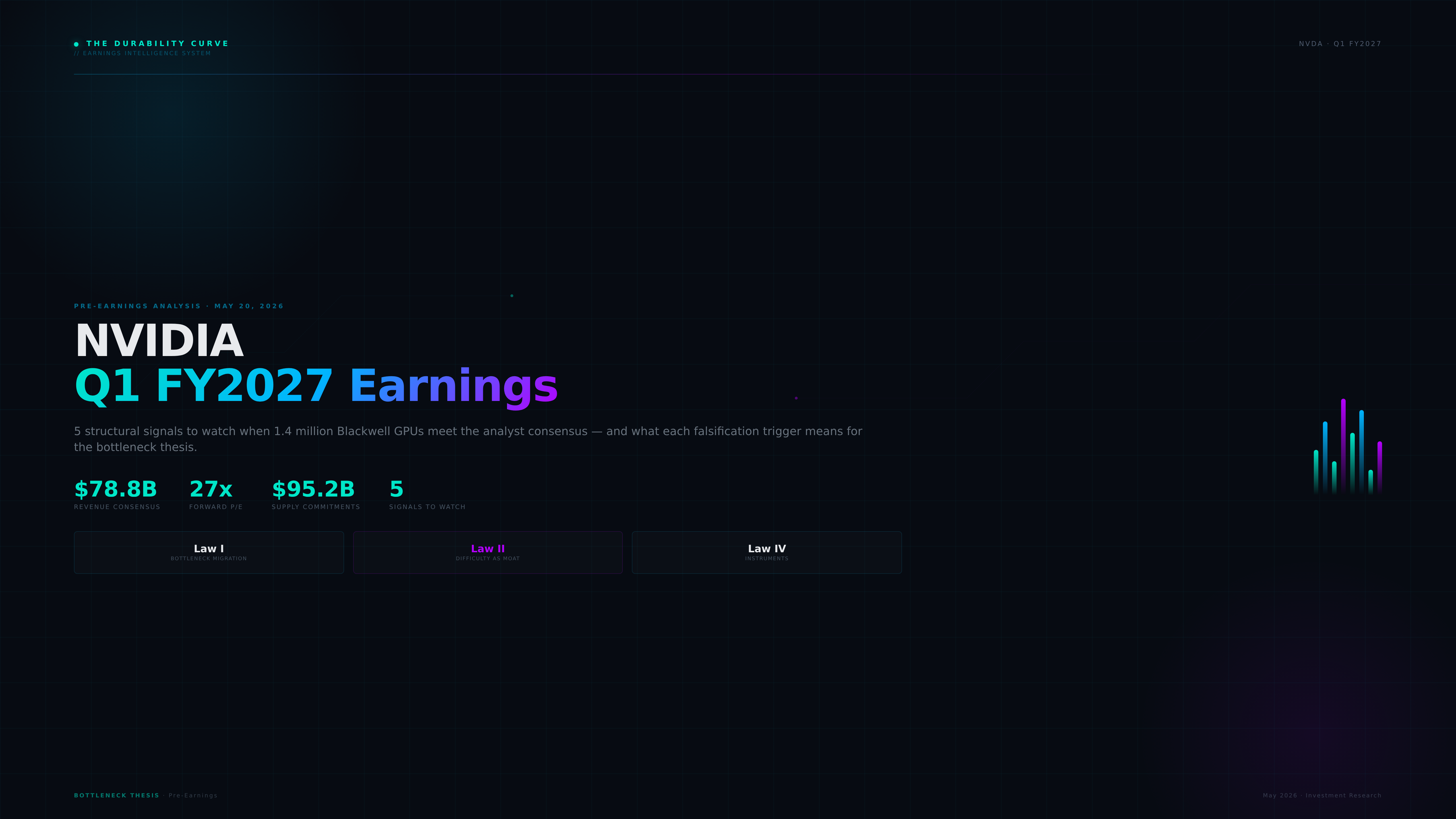

NVIDIA reports Q1 FY2027 earnings on May 20 at approximately 4:00 PM ET. The headline numbers matter less than the structural signals embedded in them.

The Durability Curve framework analyzes NVIDIA through three laws: Bottleneck Migration (Law I), Difficulty Is Load-Bearing (Law II), and Instruments Over Theory (Law IV). Each law produces a falsification trigger for Tuesday's call.

Part of full NVIDIA coverage index.

Law I Falsifier: The Supply Chain Signal

NVIDIA's purchase commitments doubled from $50.3B to $95.2B between Q3 and Q4 FY2026. This is the single most important data point on the balance sheet. Supply commitments = locked-in supply contracts for constraints NVIDIA believes are structural.

What to watch: If commitments rose further in Q1, NVIDIA is securing supply deeper into the shortage cycle. If flat or declining, either supply is easing or they have hit allocation limits.

The trigger: A flat commitment trajectory would suggest supply is catching up with demand, weakening the Bottleneck Migration thesis for NVIDIA's compute layer.

Law II Falsifier: The Optical Moat

NVIDIA committed $4.7B+ to the optical supply chain in 10 weeks — $500M to Corning, $2B+ each to Lumentum and Coherent, and ~$155M to Ayar Labs. Lumentum reported $808M revenue (+90% YoY). Coherent reported $1.81B (+21% YoY).

What to watch: Any mention of Corning, Lumentum, or Coherent by name on the earnings call. The optical interconnect layer is the next bottleneck. If management names these suppliers, the demand constraints are real and being addressed.

The trigger: Silence on optical supply chain, or describing it as 'secured,' would weaken the photonics bottleneck thesis. These are hard problems — if they are easy, the difficulty moat is shallower than assumed.

Law IV Falsifier: The ASIC Narrative

The most credible competitive threat is custom hyperscaler ASICs: Google TPU 8t/8i, Amazon Trainium 2, Meta MTIA. TrendForce projects custom ASIC shipments growing faster than GPU shipments in 2026.

What to watch: Management's framing of ASIC competition. Acknowledge + counter is the signal of clear-eyed strategy. Dismissal is concerning.

The trigger: A hyperscaler announcing >50% internal ASIC utilization across their AI workload would break the architecture-moat thesis. Not expected this quarter.

What to Read into Each Outcome

The standard framework — beat, miss, guide — tells you how the market feels. The Falsification Framework tells you whether NVIDIA's structural position improved or weakened.

- Bull case: Commitments rising, optical supply named, margins stable, inference quantified, ASICs acknowledged. All three laws intact.

- Base case: Revenue in-line, commitments flat, no supply chain commentary. Laws untested. Position unchanged.

- Bear case: Commitments declining, margins compressing, ASICs dismissed. At least one law falsified.

Published by The Durability Curve — AI infrastructure research. Finding compute bottlenecks before they are priced.

Free weekly analysis on Substack

Part of the NVIDIA Q1 FY2027 earnings coverage. See the full NVIDIA earnings coverage hub.