Inside the Hyperlane drop: How it works?

JJHow the Hyperlane airdrop actually works — and why you’re not the main character here

Hyperlane is a carefully planned scheme where everything was rigged for insiders. Hyperlane created the illusion of a fair distribution, but in reality, it funneled tens of millions of tokens into pre-prepared pockets using an open but misleading mechanism.

And if you dig deeper — this wasn’t an airdrop, but a dirty operation to cash in on the project’s future market cap.

Read carefully — everything is backed by numbers, facts, screenshots, and transactions.

How it’s “officially” set up

We can open Hyperlane medium article and read:

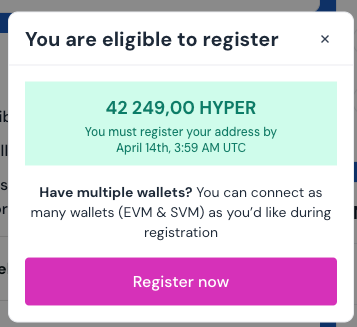

6.25% of total supply will be distributed at TGE, with 85% of rewards passed through to application end-users.

Sounds nice, right? Like it’s all going to users. But let’s break it down.

62,500,000 HYPER tokens will be distributed in the drop. That includes everyone — users and dev teams. Users are set to get 85% of that amount, while teams get the remaining 15%.

The distribution isn’t based on the number of transactions, total volume, or some complex formula. It’s much simpler: the airdrop is linear and based on how much gas you paid into Hyperlane contracts.

The more you paid, the more you get. It’s that straightforward

Looking at the reality

Now, we jump into the Hyperlane Dune dashboard:

https://dune.com/realpeha/hyperlane

We see around 7 million total transactions. That’s the visible activity — real numbers could be even higher. But let’s be conservative here. We’ll base all our estimates on the lower end, just to understand the minimum reasonable value of the HYPER token.

Here’s the deal:

- You paid gas fees — Hyperlane tracked it.

- You paid more — you get more tokens.

- The entire airdrop system is built on this mechanic.

And this is where it starts to get interesting…

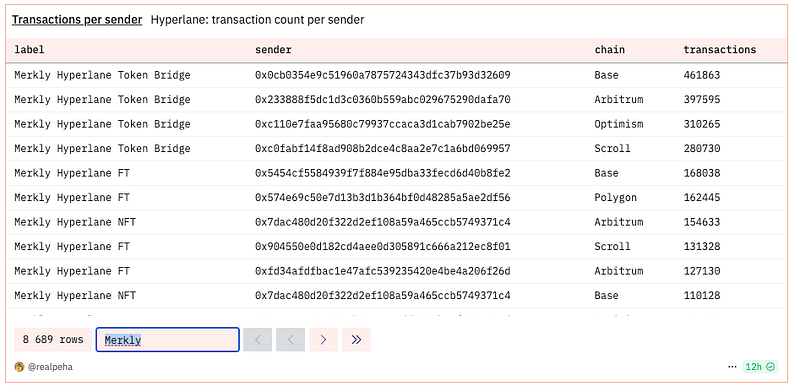

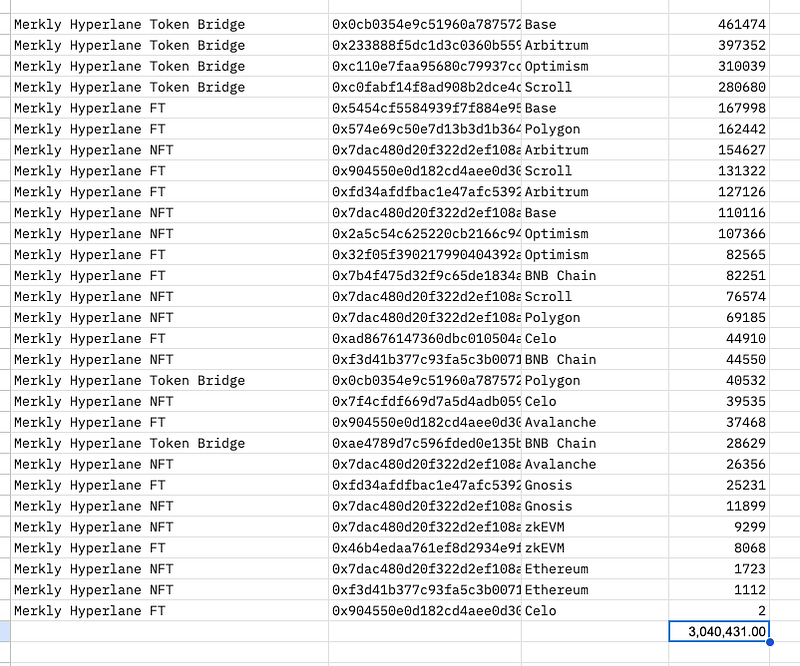

Of course, we begin with the biggest fish in the Hyperlane pond: Merkly.

Here are two wallets used for deploying their contracts. First up:

0xCe17f4bD2E0a12F3f7c81d4Ca3057e46e7600E3c — this one was used to deploy their FT and NFT contracts.

0xe584B655a6D3D818998670f73c9c0702B66498e2 — this is the address from which the ETH Bridge was deployed.

So, it turns out that the Merkly will receive approximately 3,250,000 HYPER tokens on their addresses.

Now, we go to the same service on Dune, search using the keyword in the contract name, and export the data to double-check the calculations.

In general, the numbers are in the same ballpark. Obviously, Dune can’t cover all networks and all transactions, so we’ll just assume that we got the general trend.

Token Distribution and User Earnings

- 85% for users and 15% for developers.

Now, let’s calculate how much the Merkly users earned, given that the deployer wallet received 3,250,000 HYPER tokens. (I’m intentionally using lower estimates to get a rational calculation).

Calculating: 3,250,000 / 15 * 85 = 18,416,666 tokens earned by the users, while the total allocation for everyone who used the Merkle contracts was approximately 21,600,000 tokens. This is again a lower estimate.

What does this mean? About one-third of all tokens will be sent to the Merkly ETH Bridge users, following this principle and LITERALLY A HALF OF THE WHOLE DROP goes to Merkly's users.

Merkly has around 3,000,000 transactions via Hyperlane, and they receive around 3,000,000 tokens to their addresses (simple math, 1-to-1).

Users will receive approximately 5.6 tokens for every transaction made via Hyperlane.

BUT MAIN QUESTION:

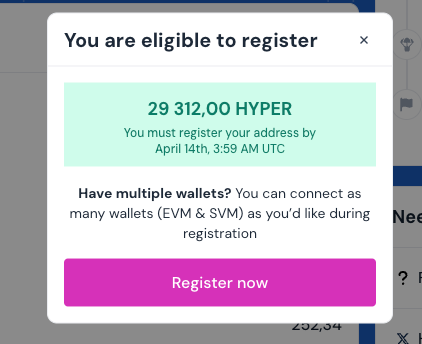

At what price did the audience purchase these tokens?

Let’s check token price

The deployer wallet for ETH Bridge holds over ⅔ of the total Merkly token allocation, so it sets the price.

(And if you think about it rationally, this cluster of contracts earned almost a half of the entire Hyperlane allocation. Just think about it — does this remind you of anything? 😏 )

The Price of Gas and Contract Calls

Over the past year, the cost of one contract call was around $1 when ETH was in the $3000-$4000 range. Some networks were slightly higher or lower, but this estimate should work well for our calculations.

What does this mean?

It means that users buy their 5.6 tokens for about $1.

To cover gas and fees, Hyperlane’s tokens farmed by one transaction need to be worth at least $1.1.

$0.2 — This is the lower limit for the token price if we consider these factors.

Most interesting part — where do the fees go that Merkly holds?

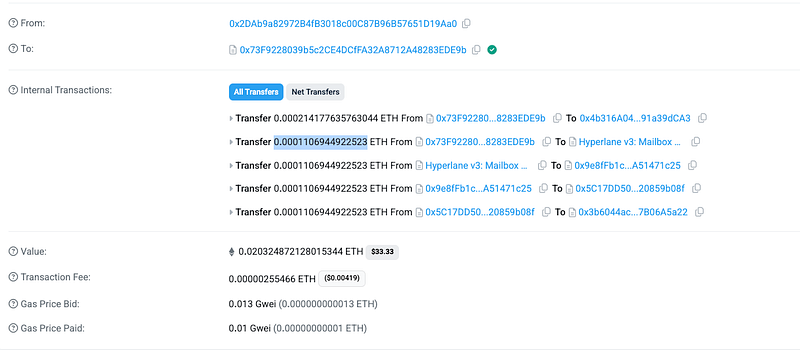

Here’s an example of a transaction made in December, during the peak interest in Hyperlane, from Arbitrum to Optimism:

Transaction on Hyperlane Explorer: https://explorer.hyperlane.xyz/message/0x431946c1831b07d74e83fb7928d230f6d99345f49ec81c61d4026f2f336d8583

Check out the detailed transactions:

Arbiscan Transaction: https://arbiscan.io/tx/0xe57412d0c83eb158e126fc96b86ba789a63f6748ad7146900c26352fa522b8df

Optimistic Etherscan Transaction: https://optimistic.etherscan.io/tx/0x52f5f6bb3f9625d0a4cfea3ab2bdaa8d621635e88f62e9f83ff8e0afc89bfabb

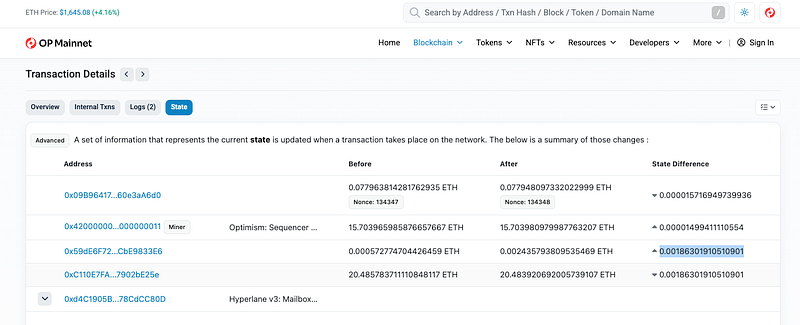

Hyperlane retains a fee of 0.000240032284358332 ETH, which, based on the current exchange rate shown by the explorer, is approximately $0.40.

The user initially sends 0.002178051389467342 ETH (which is $3.58) and receives 0.00186301910510901 ETH (or $3.04) on Optimism.

Minus the gas fees and the work of the sequencers, it turns out that Merkly essentially carried out a Hyperlane transaction for free.

Let’s take a look at some of the recent transactions, for example, here’s one from the explorer:

Transaction on Hyperlane Explorer: https://explorer.hyperlane.xyz/message/0x538ceab2c53851d835c0e370e9271c870c9755b5517a973a0b2e6e3c8a52f866

Can you believe it? The protocol is working for free on the token bridge; Merkly doesn’t make any profit from it, Hyperlane is the one earning.

But there’s another important detail to consider.

For example, here’s a transaction carried out through Zeroway Gas Refuel, probably one of the most ambitious Merkly’s competitor working with the Hyperlane:

Transaction on Arbiscan: https://arbiscan.io/tx/0x4f4443293f933000732cb25cc78d179b7159f35c78f4b60f54950a2db0365491

Pay attention to the fee paid to Hyperlane:

It’s less than 20 cents, which is half of what Merkly pays

Now, ask yourself: Why isn’t Merkly optimizing its contracts the same way Zeroway did to lower the fees paid to Hyperlane? By doing so, they could either further lower the token price and fully dominate the market, or simply pocket the savings.

For each transaction, Merkly earns essentially one token to its wallet, but based on our calculations, this token is worth about 20 cents!

This means that Merkly could save 20 cents per transaction while receiving half the tokens, resulting in a 10-cent pure profit per transaction.

The question: Why don’t they do this?

Because the Hyperlane airdrop is distributed linearly, based on the fees paid to Hyperlane, not on the amount of information in the message, the number of messages, or even the amounts being transferred.

Without this understanding, Merkly’s behavior and pricing strategy would not align with the model of a rational agent.

**Therefore, Merkly KNEW the principle behind the airdrop distribution.**Whether they got insider information directly from Hyperlane or simply have an excellent read on the market, in the end, Merkly is sacrificing approximately $500,000 for a shot at the Hyperlane airdrop, essentially giving that money to Hyperlane.

This implies that Merkly plans to recoup at least these funds, so the token’s price should be at least double — around $0.40.

But then the question arises: Why take the risk when this could be implemented almost guaranteed?

So it’s more rational to assume that the price should be even higher, at least $0.80 or $1+, to justify the risk.

Now, let’s step away from the dry calculations and look at Hyperlane’s marketing strategy and their main statements regarding the airdrop.

For the most part, they kept quiet about the airdrop, but when they lifted the taboo on the topic, they said that the airdrop would be focused on developers, which created expectations among the audience that a portion of the airdrop would be distributed by the developers themselves, as was the case, for example, with Merkly and LayerZero, where they gave out 90% of the tokens to the audience, which immediately dropped the token price.

But I remind you, Hyperlane by default gives 85% of the tokens to users, who, naturally, will sell their tokens.

Moreover, Hyperlane deliberately creates demand from the audience for the teams to distribute almost all the tokens they earned to users who will immediately dump their allocations into the market without thinking, and honestly, they will be completely right in doing so.

And now, let’s check: What about Zeroway? Who was more profitable to farm: Zeroway or Merkly?

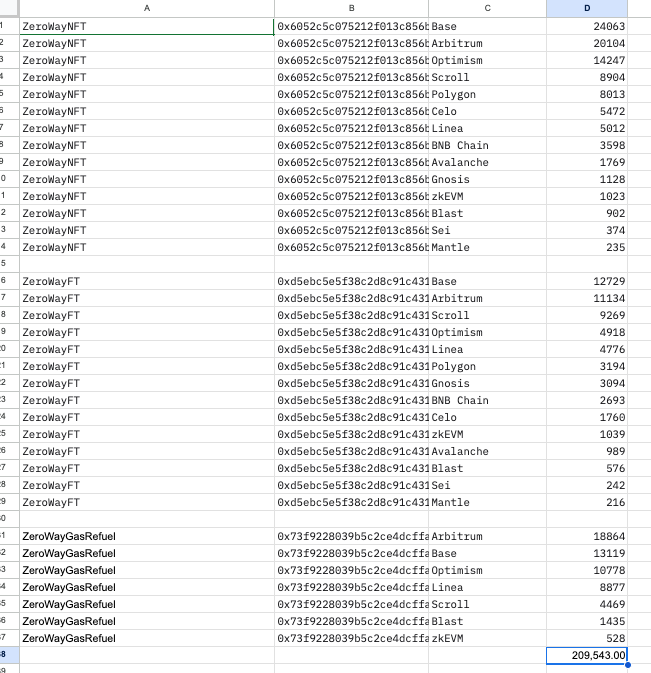

Here are Zeroway contracts:

NFT

- Address: 0x6052c5c075212f013c856bff015872914ed3492a

- Deployer: 0x91d173Fb244b72007249aECc17F6ad6E035605A4

- Airdrop:

FT

- Address: 0xd5ebc5e5f38c2d8c91c43122a105327c1f0260b4

- Deployer: 0x91d173Fb244b72007249aECc17F6ad6E035605A4

- Airdrop:

Refuel

- Address: 0x73f9228039b5c2ce4dcffa32a8712a48283ede9b

- Deployer: 0xFd8BEd310491748fF40aaF3b6A084A60560DA7C0

- Airdrop:

USDC

- Address: 0xdf4ff5122170fe28a750d3a1d2b65bb202dd0dd2

- Deployer: 0xe4180626DfFdb59d2dd7081A70B9eb265b919D58

- Airdrop: not eligible

It turns out that the Zeroway NFT contract is the price-making contract. Let’s figure out if it was more profitable to farm it than Merkly.

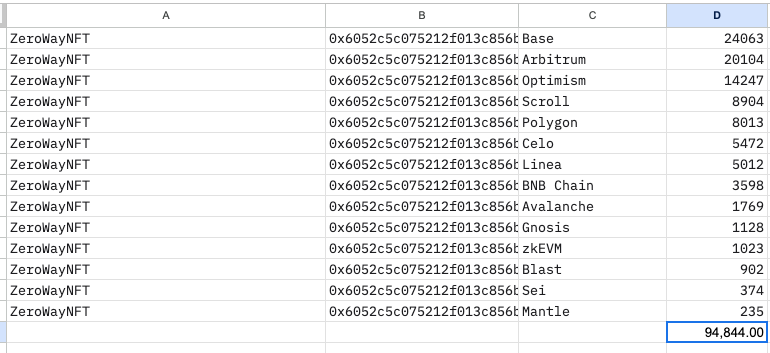

We go to Dune and look at the transactions by the contract name. In total they have…

So, Zeroway earned around 60,000 tokens for approximately 90,000 transactions.

That means the team gets 1 token for every 1.5 transactions, while Merkly gets 1 token per transaction.

But here’s the key question: which one is actually cheaper to farm?

Let’s compare the transaction costs for the two price-setting contracts of both projects.

We already know the cost of farming Merkly’s ETH Bridge is about $0.40 per transaction (at current prices).

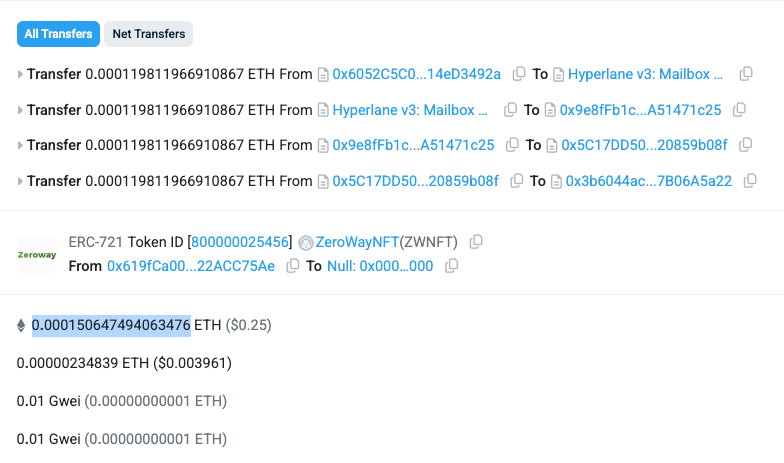

Now here’s an example Zeroway NFT transaction between Arbitrum and Optimism — one of the most commonly used routes:

https://arbiscan.io/tx/0xebd8f06a846050dad3f06211f135131f8e1cb008bc40844ea98e3726d734eb5a

Let’s break it down and compare.

So the Zeroway NFT transaction cost came out to just $0.25.

Let’s calculate that:

- Merkly earns 1 token per transaction, at a cost of $0.40/token.

- Zeroway earns 1 token per 1.5 transactions, at a cost of $0.25/transaction, which is $0.375/token.

Now let’s scale that:

- With $2, Merkly gives you 5 tokens (5 txs × $0.40).

- With the same $2, Zeroway lets you do 8 transactions (8 × $0.25), earning you 5.33 tokens (8 / 1.5).

So on large transaction volumes, Zeroway gives you a clear edge — more tokens per dollar spent.

And here’s the kicker:

If Zeroway drops their price (their extra internal fee), they could undercut Merkly by up to 25%, and their higher transaction count makes the activity look more organic and less sybil-like.

So, was Zeroway the true optimal farm?

Well… definitely not.

Let’s go back to Dune and check all transactions and actual token payouts.

Here’s what we find:

Roughly 200,000 transactions and about 140,000 HYPER tokens received — that gives Zeroway an average of 0.7 tokens per transaction, while Merkly averages 1 token per transaction.

So yes, Zeroway was less efficient overall in terms of raw token farming.

And we already know why:

Hyperlane’s airdrop logic heavily favors fees paid to them, not the number of messages or the amount of value transferred. Zeroway kept a portion of each transaction fee, which lowered the effective amount paid to Hyperlane and therefore reduced the token rewards.

To be fair, Zeroway did return part of those fees via royalties — so not everything went into their own pocket.

And honestly, if the Zeroway team is truly community-driven and focused, they now have a clear roadmap.

In this transparent environment — where we all understand how Hyperlane distributes rewards — they could easily tune their fees to match or even beat Merkly’s token-per-dollar ratio, like they already did on their NFT contract.

If Zeroway doesn’t make that change, then let’s be real:

They’re likely just another fee-scraping black box — not so different from Merkly after all.

Now, let’s ask ourselves about the Sybil resistance approach.

Remember HyperMe? The project literally offers to SEND MESSAGES THROUGH HYPERLANE, which is just a absolutely straight wrapper without real functionality. It’s one of the most Sybil projects you could imagine. And guess what?

- Address: 0xe425183Ce903a2387C00C35A6Fb47FC6B9DE8fd9

- Deployer: 0xA889c25E0fD644a27Da3f9cdf87cA7EecAB8bd28

- Airdrop:

Plus, now we know the most profitable farming strategy for Hyperlane:

You needed to take the two least popular networks and literally send anything, setting huge fees paid to Hyperlane.

These networks are Mantle and Sei EVM.

Can you guess who has the most transactions with inflated gas for Hyperlane?

If you haven’t figured it out yet, welcome to Dune LOL :)))))))))))))))

And let me tell you, the gap is pretty substantial.

If this isn’t a coincidence, I honestly don’t know what other arguments I can bring forward.

How many coincidences can we still call coincidences?????

So what does this all mean in the end?

It probably means:

- Hyperlane isn’t interested in optimization — they’re just extracting as much as they can from users under the guise of a fair protocol.

- All that talk about preventing sybil farming? Smoke and mirrors. You could farm them sybil-style to absurd levels and it would still work.

- Hyperlane may even be farming itself to inflate numbers and look better in reports.

- Merkly is very likely an insider project, backed by large funds, fully aware of how the airdrop model works.

- Most likely a cooldown period and a brutal price dump, letting those same funds scoop up HYPER for pennies.

Now ask yourself:

How is this any different from what LayerZero did?

The answer: It’s not. At all.

Curtain. 🎭