India intends to ban private cryptocurrency and push central bank digital currency

lluluIndia is preparing a bill to regulate cryptocurrency-the "Regulation Act of Cryptocurrency and Official Digital Currency in 2021". The bill will be submitted at the winter meeting of the Indian Parliament starting on November 29. It aims to ban all private individuals in India. Cryptocurrency to promote the official digital currency issued by the Central Bank of India (RBI).

Although the concept of private cryptocurrency is proposed in the bill, Indian regulation has not yet clearly defined it, which confuses the country's cryptocurrency service providers, and panic selling has also appeared in the Indian market.

On November 24, on the country’s well-known cryptocurrency exchange WazirX, Bitcoin (BTC) fell from around 4.3 million Indian rupees (approximately 57,600 U.S. dollars) to 3.35 million Indian rupees (approximately 44,900 U.S. dollars) within a day. The biggest drop was 22%; more obvious was the sell-off of the US dollar stablecoin USDT, which fell from 75.9 Indian rupees (about 1 US dollar) to 60 Indian rupees (about 0.8 US dollars).

In the past 3 years, India’s attitude towards cryptocurrency has changed. In 2018, the country banned cryptocurrency trading, but the Supreme Court removed this restriction in March 2020. Local media believe that the new bill to be discussed in the Indian Parliament attempts to pave the way for the official digital currency issued by the country's central bank by suppressing private cryptocurrencies.

India plans to ban private cryptocurrency, BTC drops 22% daily

On November 23, India will propose the "2021 Cryptocurrency and Official Digital Currency Regulation Bill" at the upcoming winter parliament meeting on the 29th. According to the parliamentary announcement, "The intended intention of the bill is to provide a convenient framework for the creation of an official digital currency issued by the Central Bank of India." The bill also attempts to ban all private cryptocurrencies in India. However, "it allows certain exceptions to promote The basic technology of cryptocurrency and its uses."

The banned object of the bill is "private cryptocurrency", and the bill does not give a clear definition of this concept, and leaves a lot of room for interpretation in the wording, such as those that promote the technology and use of cryptocurrency. exception".

This has brought confusion to cryptocurrency service providers. Nischal Shetty, the founder of WazirX, a well-known cryptocurrency trading platform in India, said that it is difficult for him to understand what the government means by "private cryptocurrency", "Bitcoin, Ether and others are public cryptocurrencies built on public blockchains and have their own specific use cases. They need to run smart contracts and write to the distributed ledger built on top of them. People cannot use INR (Indian Rupee) or USDT To pay for the Bitcoin or Ethereum blockchain .”

"Don't panic," Shetty wrote on Twitter after the news of the new bill appeared, "all of us want to regulate. We have been pushing it for more than 1,000 days... We need to treat legislators Confident, there will be discussion and deliberation.” Shetty tried to comfort his users, but panic inevitably came.

BTC plummeted in India's local exchanges

Mainstream cryptocurrencies have generally fallen in the Indian market, with a drop of more than 20%, and there has been a sharp drop. WazirX was down for a while, and the official Twitter notified the transaction delay problem of the application.

From the morning to the evening of November 24, Bitcoin (BTC) fell from around 4.3 million Indian rupees (approximately US$57,600) to 3.35 million Indian rupees (approximately US$44,900) on WazirX, the largest drop in the day by 22%; and Ethereum ( ETH ) fell from the lowest of 320,000 Indian rupees (4290 US dollars) to 250,000 Indian rupees (3352 US dollars), the biggest drop of 21%; the US dollar stable currency USDT also experienced a sell-off, down 20 from 75.9 Indian rupees (1 US dollars) %, as low as 60 Indian rupees (0.8 US dollars).

The Indian market was not repaired until 8 pm on November 24, local time. As of 4 am on November 25, BTC recovered to around 4.248 million Indian rupees, which is about 56,000 U.S. dollars; ETH rebounded to 315,000 Indian rupees. Approximately US$4,223; USDT has returned to around US$1.

At the same time, on the global crypto asset trading platform Binance, BTC reached 57,200 US dollars and ETH was around 4257 US dollars. It can be seen that there is still a pricing gap between mainstream crypto assets in the Indian market and the international market.

The Indian ban aims to pave the way for the central bank's digital currency?

Judging from the wording of the new bill, Indian regulation has left some room for cryptocurrency, and greater intentions may clear market obstacles for the upcoming central bank's digital currency.

The local media "India Today" quoted high-level government sources as saying that India may not be completely closed to concepts and technologies involving digital currencies, nor will it take a strong stance like China. At the same time, while expressing concerns about cryptocurrency, some officials emphasized the sovereign status of currency. "Currency has the support of sovereigns, and it can be supervised at all levels; if cryptocurrency gains currency status, the problem still exists, who will provide the guarantee? ?"

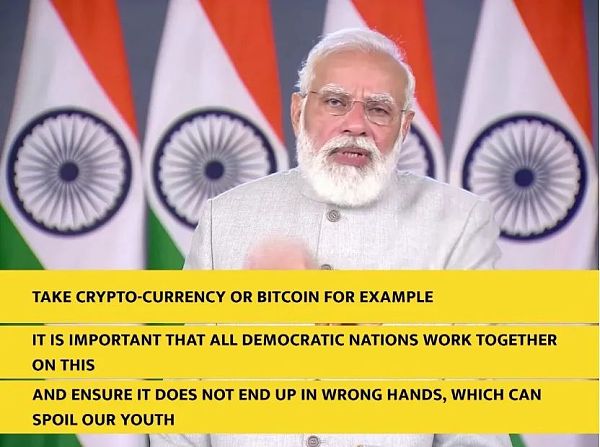

Indian Prime Minister Modi mentioned Bitcoin in the "Sydney Dialogue" forum

The media reported that there are signs that the government is trying to adjust the situation by providing cryptocurrency-related safeguards. On November 18, Prime Minister Narendra Modi (Narendra Modi) said in a speech at the "Sydney Dialogue" forum, "Take cryptocurrency or Bitcoin as an example. It is important that all democratic countries should share this. Work hard and make sure it doesn’t fall into the wrong hands and ruin our young people.”

Five days before that, Prime Minister Modi had a meeting with senior officials on cryptocurrency. A source told "India Today" that despite the volatility and risks, the popularity of cryptocurrency shows that it can become a source of government revenue. The benefits include direct taxes and goods and services taxes on services provided by cryptocurrency operators; It can also create jobs.

Since 2017, the Central Bank of India (RBI) has been expressing its serious concerns about cryptocurrencies. In July 2017, Ulijit Patel, then Governor of the Central Bank of India, stated that he was paying close attention to transactions involving cryptocurrencies. Since then, the Bank of India established an interdisciplinary committee to discuss the legality of cryptocurrencies.

On April 6, 2018, RBI issued a notice prohibiting banks and entities under its supervision from providing virtual currency-related services. But on March 4, 2021, the Supreme Court of India revoked the notice.

The definition of "private cryptocurrency" in the new bill in 2021 is very likely to be based on the recommendations made by the SC Garg Committee established by the Economic Affairs Department of the Ministry of Finance of India in January this year. The committee even proposed a ban on cryptocurrency in its report entitled "Committee's Report on Proposing Specific Actions Related to Virtual Currency," and believed that "all these cryptocurrencies are created by non-sovereign parties." In this sense, "They are completely private companies. These private cryptocurrencies have no potential intrinsic value, so they lack all the properties of currencies."

Another important recommendation of the committee is that the government should maintain an open attitude towards official digital currencies. It proposes that the Ministry of Economic Affairs establish a group with representatives from financial regulatory agencies such as RBI to review and develop digital currency models suitable for India. . If official digital currencies are to obtain the status of legal tender, the committee has proposed that the central bank should create appropriate regulatory agencies for such digital currencies in accordance with the powers of the "Reserve Bank of India Act 22."

Judging from the results, the committee’s recommendations seem to have been adopted, and India’s new bill on cryptocurrency and central bank digital currency will be discussed in Parliament on the 29th.

For local cryptocurrency service providers, a positive background is that on November 15th, the Standing Committee of Finance, led by Jayant Sinha, the former Minister of Finance of India, met with cryptocurrency exchanges and block exchanges. The representatives of the Chain and Crypto Assets Committee (BACC) and other representatives explained the rules and regulations and clear basic rules of operation. Although the members of the Financial Standing Committee expressed serious concerns about cryptocurrency and the need for supervision, at this meeting , No one proposed a ban.