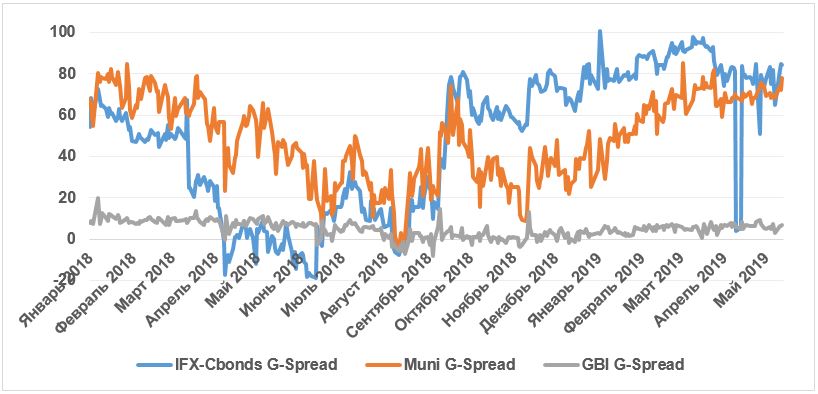

G Spread

⚡ ALL INFORMATION CLICK HERE 👈🏻👈🏻👈🏻

G Spread

g - spread and other bond spreads | Wall Street Oasis | Forum

G Spread - God is Watching (Audio EP) - YouTube

Defining Credit Risk and Understanding Credit Spreads — GoStudy

fixed income - Why is G spread bigger than Z spread theoretically?

Yield Spread Definition | G - spread , I- spread , Z- spread and OAS

Products

Blog

Login

Sign up for free!

Categories

guidance

level 3

level 1

walkthrough

curriculum

review

fixed-income

strategies

Sitemap

Home

Products

Blog

Sign Up

Credit risk is the risk of loss if a counterparty or debtor fails to make a promised payment. It has two components: the likelihood of default and the estimated recovery rate in the event of a default.

By combining these we can estimate our expected loss. In other words, expected loss = (default risk x loss severity)

For a full recap of credit risk see our blog post here .

Credit risk is not limited exclusively to default risk however. Two other factors can impact bond prices based on the perceived risk: downgrading a bond’s credit rating or changes in its spread.

Thus credit risk has three primary components:

These three components are related of course. Credit quality will decline as the risk of defaulting goes higher, and this higher risk will cause spreads to widen above an equivalent treasury security in order to compensate an investor for taking on more risk.

Not all bonds are assumed to have credit risk. We only talk about credit risk when talking about bonds that have a realistic chance of defaulting. This can include bonds from both governments and corporations, but generally excludes bonds issued by very developed countries such as U.S. treasuries.

Superior credit analysis remains the most important determinant of relative performance for a credit portfolio. This means you should be aware of the basic framework for credit analysis generally. These are the 4 Cs: character, capacity, capital, and conditions :

These 4Cs are traditionally used by various credit agencies to categorize bonds into investment-grade bonds and high-yield or junk bonds. Non-investment grade corporate bonds have higher perceived credit risk and a higher default risk than investment-grade bonds. This means that analysts need to pay more attention to loss severity , or the amount of loss if default occurs.

You may recognize these agency classifications from L1, we offer them here as useful refresher:

From a portfolio construction standpoint these public classifications often define portfolio constraints. Many institutional investors for example are required to only invest in bonds with a minimum credit rating.

As we turn now to the different strategies to manage credit risk remember we are talking about hedging three separate risks:

In this blog post, and really for the CFA Level 3 exam, we think credit spread risk is the most tested.

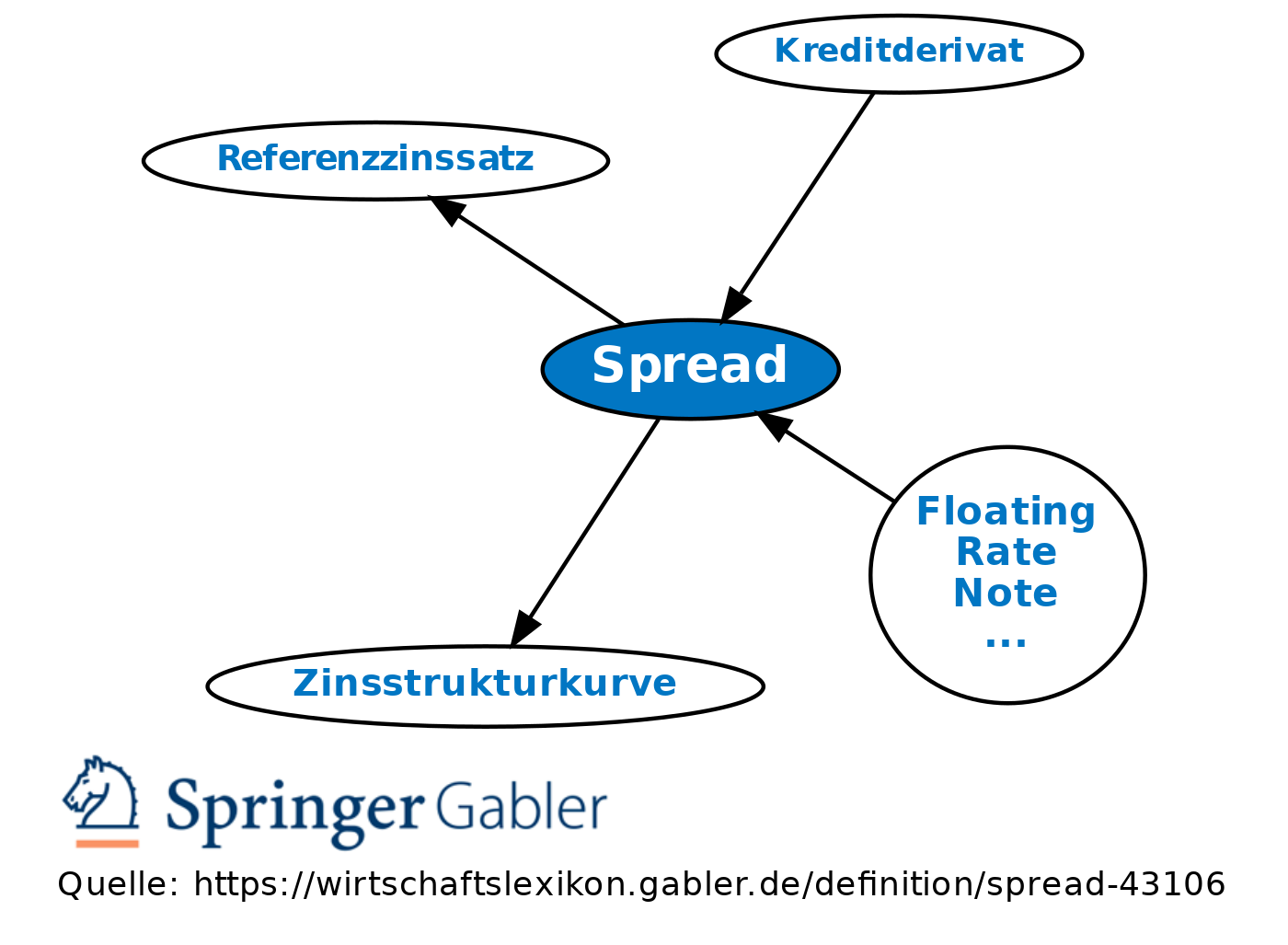

Investors in corporate bonds usually focus on the yield spread of a corporate issuance relative to its risk free benchmark (where yield spread = liquidity premium + credit spread).

Credit spread risk is the risk that spreads will widen (narrow), decreasing (increasing) the market value of a bond.

We measure this risk by using spread duration , which gives us the approximate percentage increase (decrease) in a bond’s price given a 1% decrease (increase) in credit spread.

Factors that cause credit spreads to widen include:

As we just mentioned high-yield managers care more about credit spreads than they do underlying interest rates. Both are, of course, still important.

Now when we look at a bond’s overall price change we can decompose this effect into two components: the change in price due to changes in the risk free interest rate and the change in price caused by changes in the credit spread.

Doing this successfully of course means we need a way to measure credit spread. The CFAI reading references three main credit spread measures:

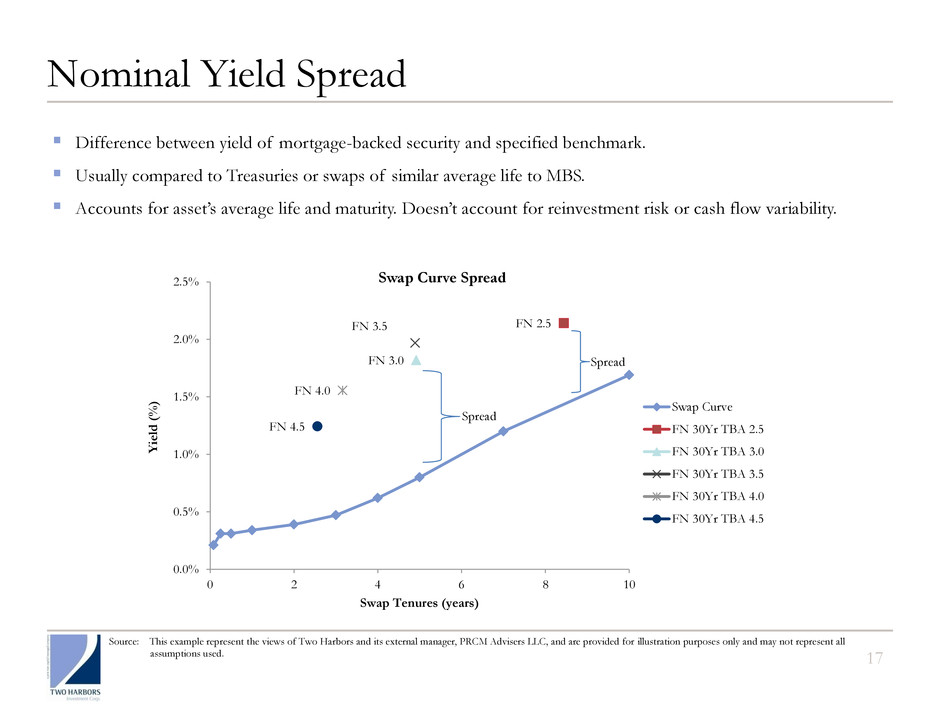

The G-spread is a simple measure of the difference of the YTM on a bond with credit risk and the equivalent duration risk-free bond, which usually refers to an on-the-run government bond. If no perfectly duration matched bond is available we take the weighted average of the two nearest bonds such that the duration matches that of the credit security.

The G-spread is a straightforward measure that can help an investor determine how to hedge interest rate risk while preserving exposure to credit risk. In other words, if you are long a high-yield bond with a duration of 6, you could sell short a government bond with the equivalent duration to hedge your interest rate risk while preserving your exposure to the underlying credit risk of the long position.

The I-spread, or interpolated spread, is calculated in the same way as the G-spread but uses the price of swap-fixed rates instead of government bonds in order to calculate the benchmark yield. The primary advantage of this approach is that swap fixed rates are priced at a far wider range of maturities, eliminating the need to assume that the yield of a specific duration government bond is the weighted average of the two closest durations that are actually issued. The wider availability of these swap prices also leads to a “smoother” curve that is less impacted by idiosyncratic factors.

That said, the I-spread also has certain disadvantages the most important of which is that the underlying bonds referenced in these swaps may not be truly risk free (e.g. a government bond from a reputable country may carry some credit risk even if they are perceived to be high quality).

Option-Adjusted Spread (OAS)s and the Z-spread

The option-adjusted spread (OAS) is a bit more complex as it accounts for the impact of options on expected return. It does this by adjusting the zero volatility spread to remove the call option value. That is . Think of it as the part of the spread above the yield on a risk-free bond that is not attributable to the effect of embedded options. As you can see from the formula, the OAS is always less than the z-spread on a callable bond. If a bond portfolio has bonds with embedded options the OAS is the most appropriate measure for credit risk. You should also know that the higher the volatility, the lower the OAS.

Higher quality investment-grade portfolios obviously have lower credit risk than a portfolio of junk-bonds. But high quality portfolios actually have higher interest rate risk. Why is this? In a sense it’s about the relative importance of the two factors.

For junk bonds, which have a large credit spread, the impact of this spread changing can dominate the impact of any interest rate changes. High quality bonds lack a large spread and thus most of their price changes are based on changes in the underlying interest rate.

In practice what this means is we see that credit spreads have a negative correlation with risk-free interest rates. It also means that junk-bond returns can behave more like those of equity assets than a more traditional fixed-income investment.

What is the mechanism for this to happen? When the economy is performing well we expect to see higher risk-free rates. We also expect to see narrower credit spreads: a rising tide lifts all boats. The reverse is also true. A poor economy leads to lower risk-free rates and wider credit spreads as the risk between a poor credit risk company and an investment-grade company grows more pronounced.

So a manager of high-yield bonds is more likely to focus on credit risk and credit spreads than interest rates.

If you remember nothing else, remember when spreads are forecast to widen that decreases returns, and when spreads are projected to narrow that will enhance returns. Also, when spreads narrow, longer duration bonds will gain more value than shorter duration bonds. Similarly, when spreads widen, longer duration bonds will lose more value than shorter duration bonds.

There are several additional ways to use or incorporate spread analysis that you should be aware for the exam but are out of scope in this blog post. This includes mean reversion analysis, quality spread analysis, and percentage yield spread analysis.

Get Gostudy Tips and tricks in your inbox!

GoStudy is an integrated learning platform for the CFA Exams.

We love hearing from our users. Follow us on Facebook to start a conversation!

The CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute. CFA Institute does not endorse, promote, review, or warrant the accuracy of the products or services offered by GoStudy. “CFA Institute does not endorse, promote or warrant the accuracy or quality of GoStudy. CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Wtfpass Public Sex Porn

Porn Blonde Outdoor

Ddf Solo Girls

Sleeping Teen Sex

Spread Ass Pics