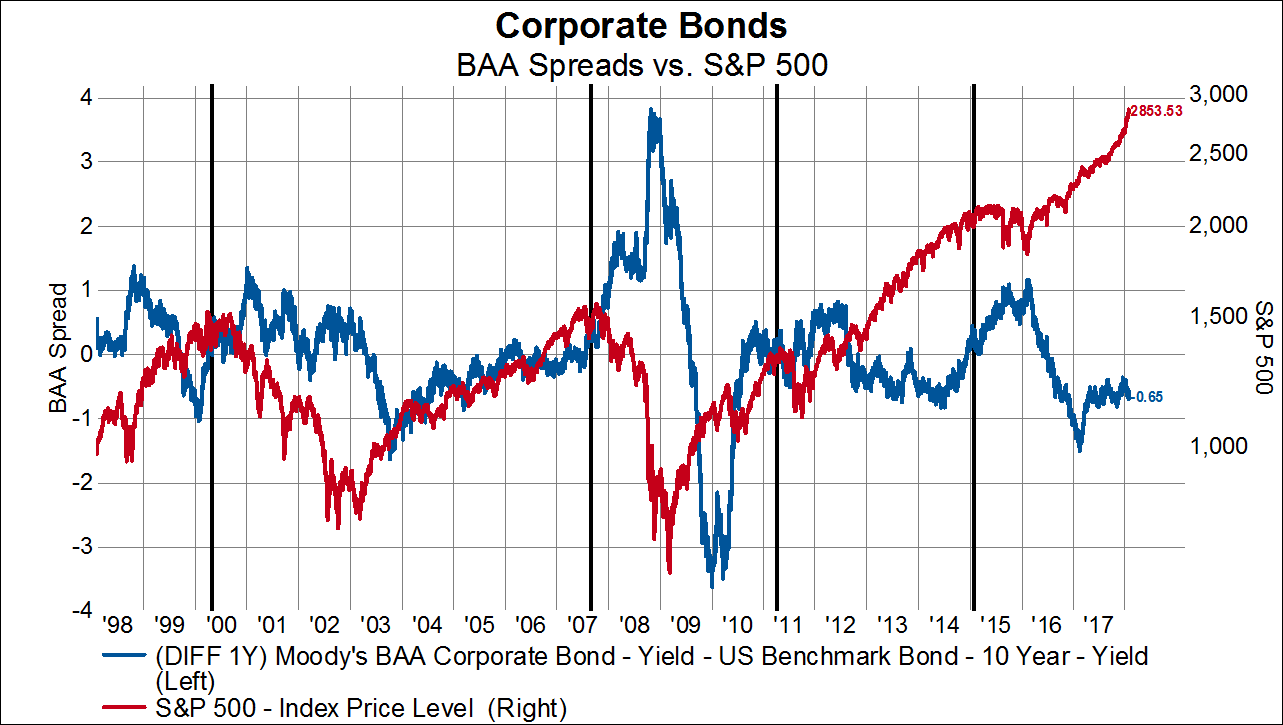

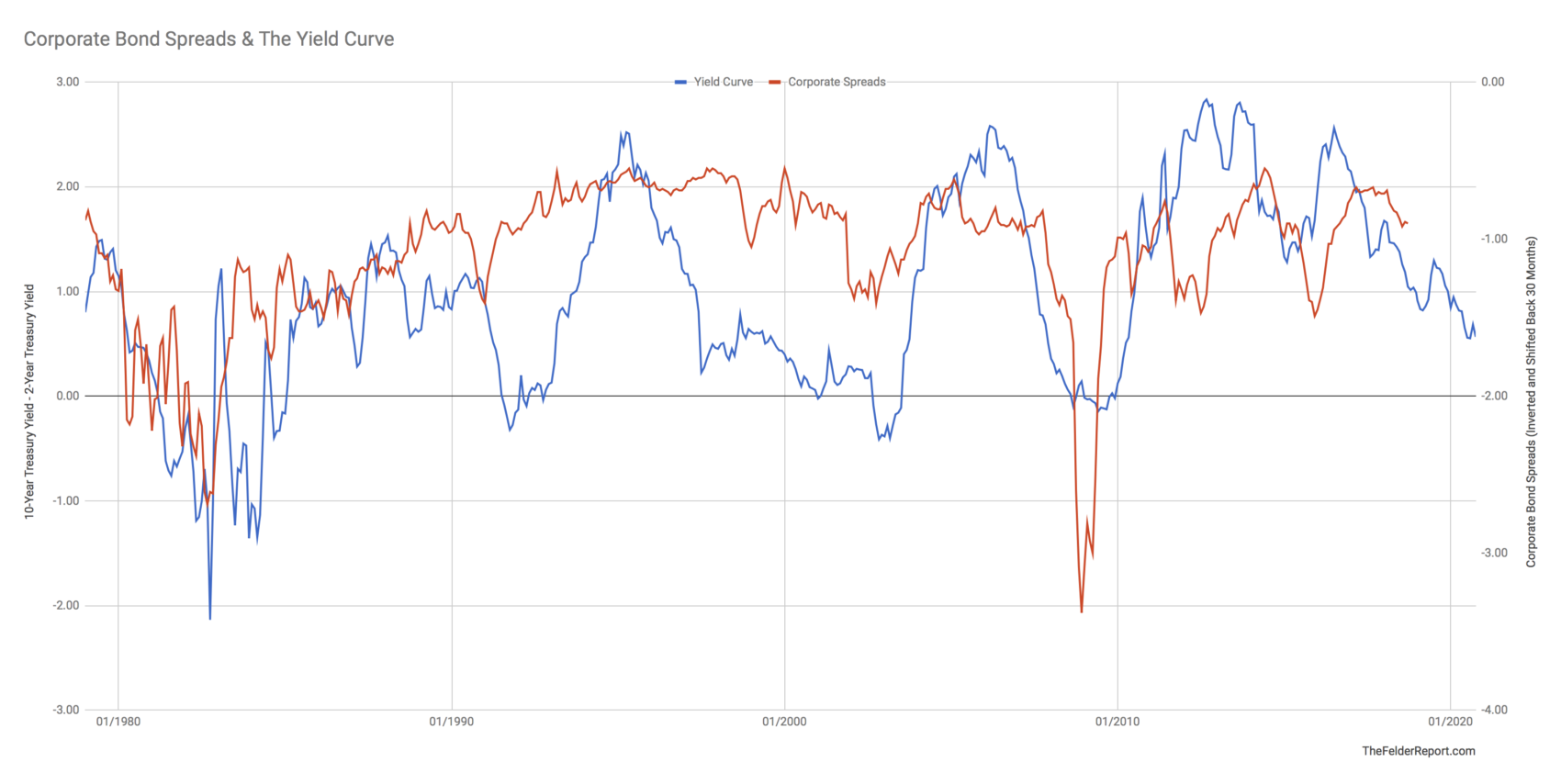

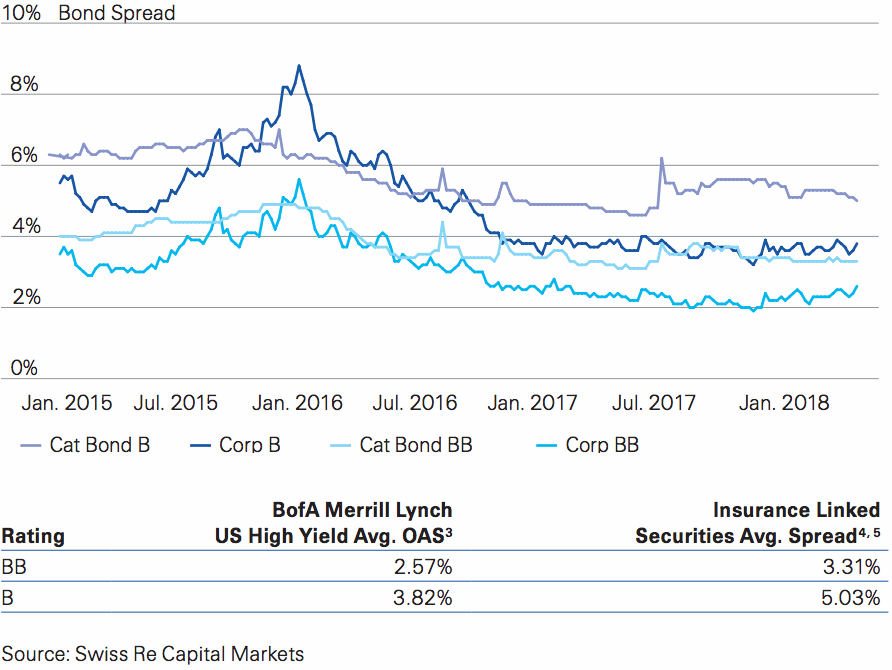

Corporate Bond Spread

🛑 ALL INFORMATION CLICK HERE 👈🏻👈🏻👈🏻

Corporate Bond Spread

Bond Spreads Bond Trading

Uncle Pipeline

Reading time: 6 minutes

Uncle Pipeline has been a Financial Pipeline contributor since 1996. He’s an expert in investments and has a wealth of financial information. From investing in bonds to managing your personal finances, Uncle Pipeline is the kindly uncle who is always there for you with great financial advice. Always opinionated but never boring, his insightful anecdotes and simple explanations will help you to make better decisions about your money. He’s like a stiff pull of hard liquor – a little hard to swallow, but remarkably warming and helpful in the end. Website: http://www.finpipe.com

Short selling, a short squeeze, and GameStop

Expert Commentary: A Taxing Problem for Bonds

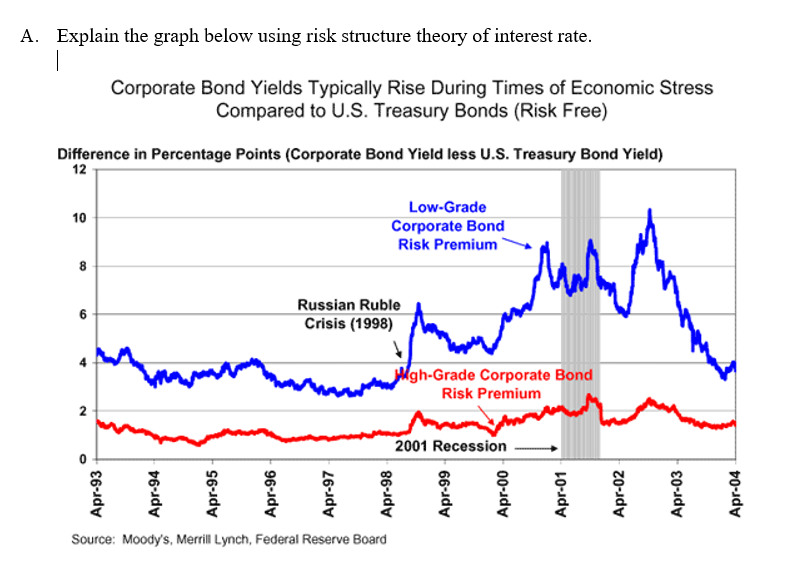

The term “bond spreads” or “spreads” refers to the interest rate differential between two bonds. Mathematically, a bond spread is the simple subtraction of one bond yield from another. Bond spreads are the common way that market participants compare the value of one bond to another, much like “price-earnings ratios” are used for equities.

Bond spreads reflect the relative risks of the bonds being compared. The higher the spread , the higher the risk usually is. People referring to bond spreads are generally talking about comparing the yields on federal government bonds, generally considered a country’s most creditworthy bonds, to the bonds of other issuers such as provinces, municipalities or corporations. Bond spreads can also be calculated between bonds of different maturity, interest rate coupon or even different countries and currencies.

Let’s compare a Sears Canada 11% bond due in 1999 (Sears 11/99) with a Government of Canada 9.25% bond due in 1999 (Canada 11/99). To properly understand the concepts of bond spreads, we must first examine the mechanics of how spreads are calculated. The current yield on the Sears 11/99 is 5.3% compared to the Canada 9.25/99 yield of 4.5%.

Below we subtract the Canada yield from the Sears yield to obtain the spread :

5.3% (Sears yield) – 4.5% (Canada yield) = .8% “Spread”

A bond trader would formally refer to this spread in terms of one hundreds of a percent or “80 basis points” (bps) or “beeps” in the jargon of the bond market.

Obviously, the interest rates on both the Sears and the Canada bond will change over time. The chart below shows the yield of the Sears bond since its issue in 1989 and the Canada bond yield for the same time period. Note that the Sears bond has a higher yield throughout the period, reflecting the fact a corporate bond trades at higher yields than a government bond. Inspecting the chart, we also see that the yields move in a very similar pattern, since both bonds have the same term and both are affected by the general changes in interest rates.

Using computers, we can calculate the yield spread between two bonds over a time period. Below, we take the Sears yield and subtract the Canada yield for each day since June of 1989. Spreads can change considerably as they are based on many factors, as we discuss below. The spread of the Sears Canada 11/99 has moved rather violently in the eight years since it was originally issued in June 1989.

As the spread graph above shows, the Sears 11/99 was originally issued at a spread of 125 bps in 1989 and almost immediately narrowed in to the 80s since the economic cycle was at its peak and things looked good for a retailer. It then widened as the economy weakened into 1990 and gapped to a wide point of 425 bps in the corporate bond debacle of 1992 when the collapse of real estate and Confederation Life led to widespread liquidation of corporate bonds. In 1993, however, when it was apparent that Sears was still solvent and the recession was ending, the bonds tightened back in to their original issue 125 bps spread and have now continued to narrow in to 80 bps.

Spreads seem simple but reflect a lot of underlying valuation factors. Here are some of the spreads that can be calculated, as well as their commonly understood meaning:

Credit Spreads are the differences in interest rates that reflect the credit risk between two bonds. The larger or “wider” the spread, the higher the credit risk of the high interest rate bond compared to the low interest rate bond. Corporate bonds generally have higher yields than similar maturity federal government bonds, as in our Sears Canada example above, reflecting their higher default or credit risk. The lower the credit quality and rating, the higher the yield spread compared to governments. That is why “less than investment grade” or “junk bonds” are commonly called the “high yield” sector of the bond market.

Term or Duration Spreads are the spreads that reflect the different interest rates between bonds of different maturity . For example, the current interest rate on the very short-term, two year Canada bond in our example is 4.5% reflecting its minimal capital risk because of interest rate movements. The current interest rate on a thirty-year Canada 8% of 2023 is 6.1%, reflecting its greater “interest rate risk”. The yield spread or “curve spread ” between these two bonds is 1.6%, which reflects the interest rate between the two bonds and the conditions of monetary policy.

Coupon Spreads are spreads that reflect the differences between bonds with different interest rate coupons. For example, the Government of Canada has issued two bonds that are due in 2008, one with a 10% coupon (Canada 10/08) and one with a 7% coupon (Canada 7/08). These two bonds have very similar maturities but very different coupons with a 3% difference in payment each year until the final repayment of the principal of $100 at maturity. Right now, these bonds trade 10 bps apart in yield, reflecting the difference in coupon and liquidity. At one time, there was a very large difference in coupons of over .5% between Canada issues, reflecting the illiquidity of the Canadian bond market and tax preferences of investors. Clearly, a taxable investor would prefer to have less up front taxable income and would prefer to own a “lower coupon” bond. In recent years, the “stripping” activity of investment dealers, which produces “zero coupon” bonds , has caused coupon spreads to narrow considerably as high coupon bonds were sought because of their profitable “stripping” characteristics (higher profits for dealers).

Liquidity Spreads reflect the difference in “liquidity” or ease of trading between bonds. For example, an investor can buy Province of Ontario “zero coupon” bonds for the same maturity date in three different forms: 1) a “coupon” which is a stripped coupon payment from an Ontario bond; 2) a “residual” which is the stripped principal payment from an Ontario bond; and 3) an actual zero-coupon Ontario Global bond issue which was originally issued as a zero coupon “global” bond issue. In terms of liquidity, the “global zero” trades at the lowest spread to Canada bonds, given its high liquidity. The residual trades at a wider spread , reflecting its lower liquidity. The coupon trades at the highest yield and spread , reflecting its smaller size (each “coupon” is ½ of a bond’s stated interest rate, for example, $4 on an 8% interest rate) where the residual is $100.

There are many other types of spreads , such as “ swap spreads ” which reflect the demand for fixed to floating interest rate swaps or “ Yankee spreads ” which are spreads between U.S. dollar bonds of domestic and foreign issuers. Investment strategists use the spreads between the dividend yield and earnings yields on stocks and bond yields in their judgments on the relative attractiveness of these markets.

Traders use yield spreads as their benchmark for valuing bonds. Most traders have computer trading systems, such as Bloomberg and PC Bond which allow them to quickly calculate historical and actual spreads between many different bonds. To discuss the fundamentals of “spread trading”, one must recall the relationship of bond prices to interest rate movements. Remember that an increase in interest rates for an existing bond leads to a decline in price and that a decrease in interest rates leads to a decline in a bond’s price.

It’s also important to remember the inverse bond price and interest rate relationship, which we can transfer to our bond spread trading . Consider a yield spread increase. Take our Sears 11/99 moving or “widening” from an 80 bps spread to a 100 bps spread . This increases its relative interest rate. We start with the Canada 9.25/99 at 4.5% with the Sears at 5.3%, which is 80 bps higher. Let’s say that interest rates don’t change and the Canada stays at 4.5% but because corporate bond supply is heavy the Sears “widen” or increase in spread to 100 bps. This makes a new interest rate of 5.5% on the Sears bond (4.5% + 1% = 5.5%). This means that the price of the Sears bond will fall about $.40 since its interest rate rose. This also means that despite the Canada bond staying at the same price and yield, the Sears bond has fallen $.40 or “under-performed”.

The opposite would be true for a spread tightening. If the yield spread on the Sears bond fell or “tightened” to 60 bps, it means its interest rate had fallen by 20 bps relative to the Canada bond. This would make its price increase relative to the Canada by $.40.

The investor who has bought and held since 1989 has received 10% extra compared to Canada’s (125 bps spread for eight years) and a capital appreciation due to the spread narrowing of about 1% for a total excess return of 11.25%. The investor who bought at the issue spread of 125 bps in 1989 and sold at 425 bps in 1992 received additional spread of 3.75% (3 years of 125 bps ) versus Canada’s, but had a price loss of about 21% due to the spread widening for a total under-performance of Canada’s of –17.25%! The savvy investor who bought in 1992 and has held to 1997 has an excess spread of 21.25% (5 years at 425 bps) and an appreciation from spread narrowing of 6.9% for a total outperformance of 28.2% versus Canada’s over five years. It’s interesting how different a performance can result from the timing when a corporate was bought and sold. This all occurred when Sears Canada was rated investment grade, never falling below a BBB rating.

Who ever said that bonds were boring?

Founded in 1996 by a group of portfolio managers, The Financial Pipeline is dedicated to providing financial knowledge and education to anyone and everyone with even a passing interest in Finance. All of our articles are screened and edited for accuracy and impartiality. Our motto, “financial information for the rest of us,” speaks for itself.

Our aim is to provide financial information at all levels for financial consumers and investors. We have gone to great lengths to make sure our content is easily accessible and approachable. We have tailored-with-padding our articles to all levels of financial expertise. If you’ve seen and read enough on a subject, move on to the next one.

© Copyright 2021 Financial Pipeline. All rights reserved.

Corporate bond - Wikipedia

What Are Bond Spreads ? | The Financial Pipeline

European Corporate Bond Market: Spreads , Yields, Size - Credit Market...

Spread ratios show corporate bond buyers saying `if I have to

Understanding Corporate Bonds | PIMCO

Home / European Corporate Bond Market: Spreads, Yields, Size

Investment Grade >>

Index: iBoxx EUR Corporates

High Yield >>

Index: iBoxx EUR HY Overall

Senior & Subordinated Financials >>

Index: iBoxx EUR Financials

Non-Financial Corporate Hybrid >>

Index: iBoxx EUR Non-Financials Subordinated

CoCo Bond Market Index >>

Index: iBoxx EUR Contingent Convertibles

Sterling Corporate Market >>

Index: iBoxx GBP Corporates

This site uses cookies More info No problem

The pages listed below show the history of corporate bond spreads and performance, as well as the size and growth of the Euro-denominated corporate bond market, since 2003. They are a means for interested parties to gain a sense and appreciation of how the bond market in Europe has performed and grown during this period. All data supplied by Markit Group Ltd.

2021 starts again...

It's almost as if the second half of January was a necessary aberration, if only to check the breakneck speed with which markets were rallying. That opening rally was courtesy of new year exuberance on the back of the Biden inauguration-cum-fiscal stimulus anticipation, as well as the hope that the vaccine roll-out would necessitate an economic recovery [...]

Wobble over, big finance back in the game...

It took a blow, but the establishment is fighting back. Well, not quite, but calm has transcended the markets and the hitherto great arbiter of efficient capital allocation is back in the game. So, after reeling for much of the final week of January and unfortunately denting monthly investor portfolio returns considerably, we're o [...]

Established order rattled by the little guy...

The emerging retail-led investing phenomenon, buying (at the moment) in heavily shorted equities, has stirred markets and risks - becoming a real poke in the eye for the established order. It should throw up many concerns for traditional markets and the accepted behaviour of institutional investors (include hedge funds in that [...]

Vaccine squabbles sully the mood...

The 'Biden bounce' might have turned into an almighty, vaccine-squabble-inspired sell-off. And the huge bullish tone early on may have flipped, leaving markets exhibiting a more nervous disposition. But they've bounced again, leaving investors chewing on whether they will hang on for a bit longer this time. After all, in January, risk mark [...]

Mature Mom Sleep Sex

Sex Asian School Girl Skachat

Skinny Teen Pee Gif

Download Porn Sexy Naughty America

Czech Couple Public Agent Porn

:max_bytes(150000):strip_icc()/CorporateBonds_CreditRisk22-8c12f1dbc1494f28b3629d456fb4fa63.png)