A Comprehensive Guide to Car Coverage: All You Need to Understand

Traveling through the landscape of auto insurance may be intimidating, yet it is a necessary part of prudent car ownership. Whether you are a first-time car buyer or just looking to evaluate your current policy, grasping the nuances of car insurance is imperative. This guide aims to clarify the various components of auto insurance, to help you arrive at informed decisions that suit your needs and budget.

Auto insurance is more than just a legal requirement; it is a shield for you, your vehicle, and others on the road. From liability coverage to all-inclusive plans, the options available can be quite diverse, making it essential to know what each type includes. In this comprehensive guide, we will examine the important terms, policy types, and tips for obtaining the best coverage for your specific situation, empowering you to drive with certainty.

Types of Auto Insurance

Auto insurance comes in several forms, all designed to meet distinct needs and requirements. The primary type is liability insurance, that is required by law in numerous states. This coverage helps pay for injuries and damages you cause to other people and their property in an accident. Liability insurance does not cover your personal injuries or damages; instead, it protects you from the financial fallout of being at fault in a collision.

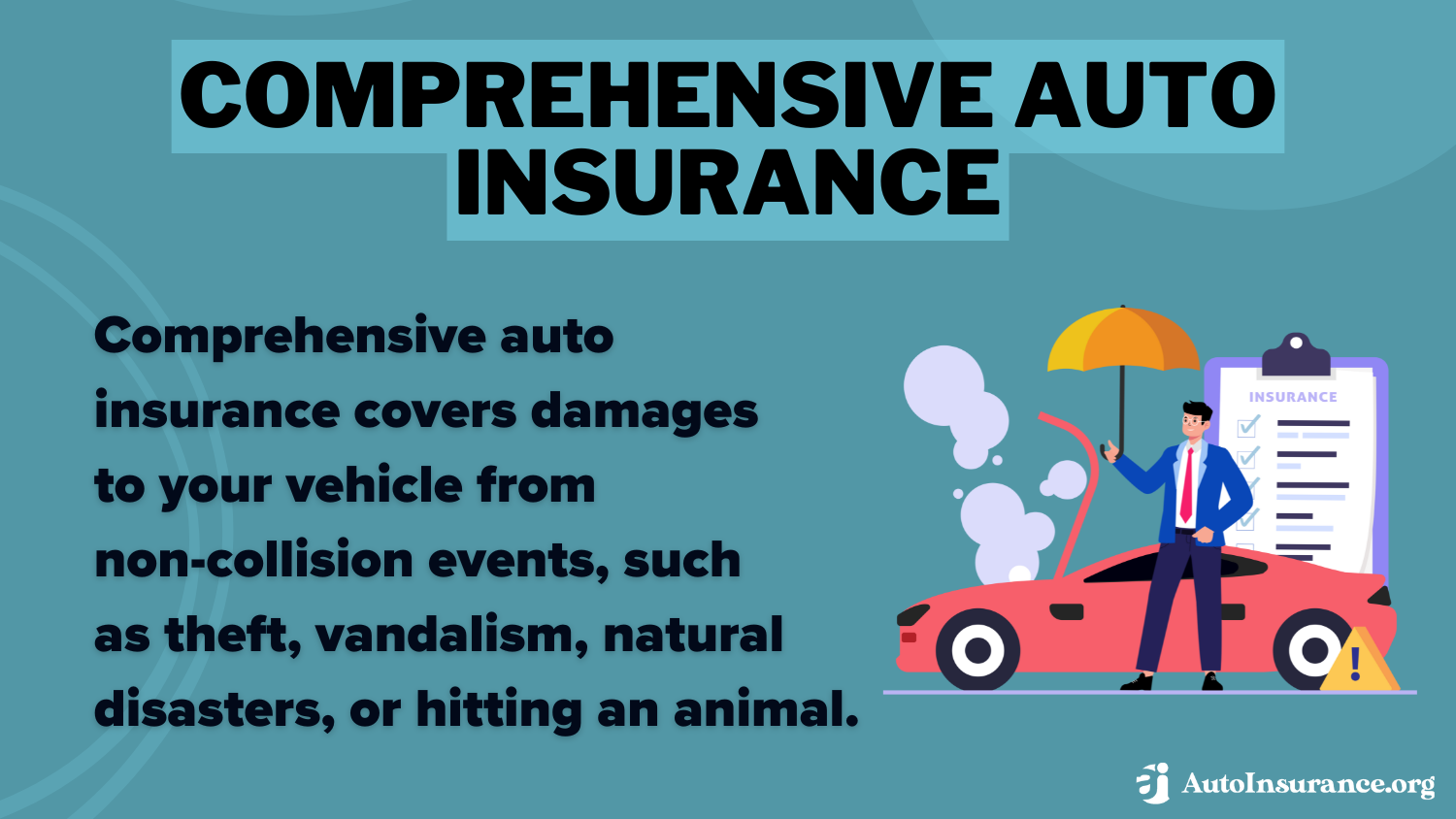

An additional type is collision insurance, which covers damage to your own vehicle resulting from a collision with another car or object, no matter who is at fault. This insurance is especially useful for new or more expensive vehicles where repair costs can be substantial. Additionally, a lot of drivers choose comprehensive insurance to protect against non-accident incidents such as theft, vandalism, or natural disasters. Comprehensive coverage ensures that you are protected from a broad spectrum of potential risks beyond just accidents.

Uninsured and underinsured motorist insurance is also crucial. This form of insurance protects you in case you are involved in an accident with a driver who does not carry any insurance or has insufficient coverage to pay for the damages. Having this form of coverage can provide reassurance knowing that you are protected against drivers who may not take the necessary precautions to have adequate insurance. Each type serves its purpose, and understanding them can help you choose the best auto insurance policy for your needs.

Understanding Insurance Choices

In the realm of car insurance, comprehending the different coverage choices available is essential for making wise decisions. Auto coverage is not a one-size-fits-all product; each type of coverage has a specific purpose. Common types of coverage include obligation, collision, comprehensive, injury protection, and uninsured motorist coverage. Knowing what each option provides helps you tailor your policy to meet your specific needs and budget.

Obligation coverage is often required by law and guards you in the event that you're liable for an accident that causes injury to others or destroys their property. Collision coverage, on the other hand, aids pay for repairs to your vehicle after an accident, no matter of who is at fault. Comprehensive coverage safeguards against non-crash incidents such as theft, vandalism, or natural disasters. Evaluating these choices will allow you to emphasize what is most important for your situation.

Moreover, injury protection provides coverage for medical expenses and lost wages resulting from an accident, regardless of fault. Uninsured motorist coverage defends you if you are involved in an accident with someone who is without ample insurance. Comprehending these coverage options not only helps enhance your financial protection but also offers reassurance as you navigate the roads.

Components Impacting Premiums

Several factors play a critical part in calculating the costs you are charged for auto insurance. One of the key important considerations is your driving history. Insurers examine your history for accidents, speeding tickets, and other road violations. A clear driving record typically yields decreased costs, while a history of violations can result in elevated rates. Additionally, insurers consider your years, sex, and even your marital situation, as demographics suggest that particular categories are likelier to make claims.

Another crucial factor is the kind of car you own. Sports cars often have higher premiums due to the increased risk of accidents and victimization. On the other hand, vehicles equipped with safety features and high crash test ratings may qualify for lower rates. The vehicle's years, brand, model, and overall worth are also crucial elements that insurers assess to assess risk and set rates.

Finally, your where you live can significantly influence your auto insurance costs. Living in urban areas typically results in higher costs due to a larger probability of accidents, loss, and damage. Conversely, rural areas may offer lower risks, resulting in more affordable coverage. Additionally, factors such as the local crime rate, environment, and the density of uninsured motorists in your area can also impact how insurers calculate your premiums.

How to Choose the Best Policy

Selecting the appropriate auto insurance policy requires analyzing your personal needs and comprehending the offered options. Begin by analyzing your driving habits, the category of vehicle you own, and your budget for premiums. Consider factors such as mileage, age of the car, and whether you primarily use it for commuting or leisure. Such elements can substantially influence the sort of protection that is fitting for you.

Then, familiarize yourself with the diverse types of insurance options available. Liability coverage is typically required by law and protects you against claims for damages or injuries you impose to others. Additionally, you may want to look into collision coverage, which compensates for damages to your vehicle after an accident, and comprehensive coverage, which covers against non-collision incidents such as theft or natural disasters. Comprehending these coverages will help you customize a policy that fits your needs.

Finally, take the time to review quotes from multiple insurance providers. Rates can fluctuate significantly, so obtaining several quotes will provide you a better picture of the market. Look for discounts that may apply, such as safe driver discounts, bundling policies, or discounts for certain safety features in your car. By thoughtfully weighing your options and opting for a policy that aligns with your driving habits and financial situation, you can secure the most suitable auto insurance for your needs.

Prevailing Auto Insurance Misconceptions

A lot of people harbor misconceptions about auto insurance that can lead to poor decisions when choosing coverage. One widespread myth is that the shade of a car affects insurance rates. Although it may seem logical that a vivid scarlet car would be priced more to insure, the fact is that insurance companies determine their rates primarily on factors like the driver's history, the car’s brand and model, and safety ratings, rather than its shade.

Additionally prevalent myth is that just inexperienced drivers pay high premiums. Although it is true that younger drivers often face higher rates due to their insufficient driving experience, factors such as a clean driving record, financial score, and location can significantly impact rates for drivers of all groups. A lot of adults may discover themselves paying high premiums if they have a track record of incidents or infractions.

In conclusion, there’s a notion that all auto insurance policies provide the identical level of coverage. In reality, policies can vary substantially in terms of coverage restrictions, out-of-pocket expenses, and the types of coverage provided. It’s essential for consumers to thoroughly review their policy details and grasp the distinctions between fundamental liability coverage and full or accident options. Making the right choices can ultimately save money and provide greater protection on the road.

Filing a Claim: Step-by-Step

When you are in an accident, the initial step is to ensure everyone is safe and request medical assistance as needed. Once addressing urgent safety concerns, collect all pertinent information at the scene. This includes details about the other driver, such as their identity, phone number and address, policy details, and license plate number. Document on the accident's details, including the timestamp, location, and any witnesses. Capture the scene with photographs to create a visual record for your claim.

Once you have collected all necessary information, get in touch with your auto insurance provider to initiate the claims process. Texas cheap car insurance have a specific claims hotline that enables you to notify an incident quickly. Be prepared to provide your insurance policy ID and specific information about the accident. Your insurer will walk you through the next steps, explain what documentation is required, and designate a claims adjuster to your case who will evaluate the damages and determine liability.

After filing your claim, maintain records of all communication with your insurer and any paperwork you submit. Follow up regularly to check the status of your claim and respond to any additional requests from the claims adjuster. Based on the nature of the claim, resolution may take some time, but staying systematic and proactive will help ensure a smoother process.