Economics

Harshit YadavUnit -7

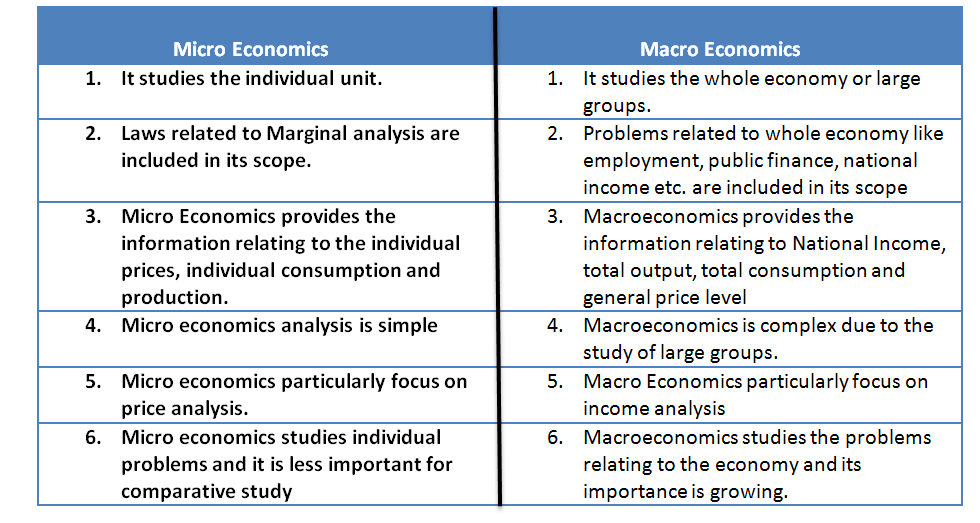

What is 'Macroeconomics'

Macroeconomics is a branch of the economics field that studies how the aggregate economy behaves. In macroeconomics, a variety of economy-wide phenomena is thoroughly examined such as, inflation, price levels, rate of growth, national income, gross domestic product and changes in unemployment.

It focuses on trends in the economy and how the economy moves as a whole.

Macroeconomists study aggregated indicators such as GDP, unemployment rates, national income, price indices, and the interrelations among the different sectors of the economy to better understand how the whole economy functions. Macroeconomists develop models that explain the relationship between such factors as national income, output, consumption, unemployment, inflation, savings, investment, international trade and international finance.

Basic macroeconomic concepts (Expand if required)

- Output and Income

- Unemployment

- Inflation and Deflation

What is GDP ?

GDP is the total monetary value of the final goods and services produced within the geographical boundaries of a country in a given period of time.

Gross domestic product is the best way to measure a country's economy. GDP is the total value of everything produced by all the people and companies in the country. It doesn't matter if they are citizens or foreign-owned companies. If they are located within the country's boundaries, the government counts their production as GDP

Link for More Info : WEB URL

What is GNP (Gross National Product) ?

Gross national product (GNP) is the market value of all the products and services produced in one year by labor and property supplied by the citizens of a country. Unlike gross domestic product (GDP), which defines production based on the geographical location of production, GNP indicates allocated production based on location of ownership. In fact it calculates income by the location of ownership and residence, and so its name is also the less ambiguous gross national income.

DIfference between GDP and GNP

GNP and GDP are very closely related concepts, and the main differences between them comes from the fact that there may be companies owned by foreign residents that produce goods in the country, and companies owned by domestic residents that produce products for the rest of the world and revert earned income to domestic residents.

What is 'Income Per Capita'

Income per capita is a measure of the amount of money earned per person in a certain area. It can apply to the average per-person income for a city, region or country, and is used as a means of evaluating the living conditions and quality of life in different areas. It can be calculated for a country by dividing the country's national income by its population.

What is 'Inflation'

Inflation is the rate at which the general level of prices for goods and services is rising and, consequently, the purchasing power of currency is falling. Central banks attempt to limit inflation, and avoid deflation, in order to keep the economy running smoothly.

What is 'Privatization'

Privatization can refer to the act of transferring ownership of specified property or business operations from a government organization to a privately owned entity, as well as the transition of ownership from a publicly traded, or owned, company to a privately owned company. For a company to be considered privately owned, it cannot secure funding through public trades on a stock exchange.

What is 'Globalization'

Globalization is the tendency of investment funds and businesses to move beyond domestic and national markets to other markets around the globe, thereby increasing the interconnection of the world. Globalization has had the effect of markedly increasing international trade and cultural exchange.

What is a 'Value-Added Tax - VAT'

A value-added tax (VAT) is a type of consumption tax that is placed on a product whenever value is added at a stage of production and at final sale. VAT is most often used in the European Union. The amount of VAT that the user pays is the cost of the product, less any of the costs of materials used in the product that have already been taxed.

For example, when a television is built by a company in Europe, the manufacturer is charged VAT on all of the supplies it purchases to produce the television. Once the television reaches the shelf, the consumer who purchases it must pay the applicable VAT.

GATT , TRIPS from hard copy notes

UNIT -6

What is a 'Market'

A market is a medium that allows buyers and sellers of a specific good or service to interact in order to facilitate an exchange. This type of market may either be a physical marketplace where people come together to exchange goods and services in person, as in a bazaar or shopping center, or a virtual market wherein buyers and sellers do not interact, as in an online market.markets do not necessarily need to be a physical meeting place. Internet-based stores and auction sites are all markets in which transactions can take place entirely online and where the two parties do not ever need to physically meet. Technically speaking, a market is any medium through which two or more parties can engage in an economic transaction, even those that do not necessarily need to involve money. A market transaction may involve goods, services, information, currency or any combination of these things passing from one party to another in exchange for one of these or another combination.

Markets establish the going rates for goods and other services, which sellers determine by creating supply and which buyers determine by creating demand. A market is a focal center for the distribution of goods and resources within a society

>>Types of market

- Perfect Competition

a.) There is free entry and exit for different firms operating in this market. The only hindrances to entry are firm’s related constraints like costs and lack of raw materials.

b.) The goods sold in this market are homogenous. Homogenous means that the products are almost identical and the consumer does not prefer one product to the other.The perfect competition market has also a very large number of buyers and sellers. This way there is no individual firm in the market that can influence the prices of goods and services.

c.) The individual firms are price takers and have to accept the prices set by the laws of demand and supply.

d. )In a perfectly competition market there is no information asymmetry and Perfect information is available to the buyers and sellers.

2. Imperfect Competition

a . Monopoly

In business terms, a monopoly refers to a sector or industry dominated by one corporation, firm or entity.

Monopolies can be considered a extreme result of free market capitalism: Absent any restriction or restraints, a single company or group an enterprise becomes big enough to own all or nearly all of the market (goods, supplies, commodities, infrastructure and assets) for a particular type of product or service. Antitrust laws and regulations are put in place to discourage monopolistic operations – protecting consumers, prohibiting practices that restrain trade and ensuring a marketplace remains open and competitive

b. Oligopoly

Oligopoly is a market structure in which a small number of firms has the large majority of market share. An oligopoly is similar to a monopoly, except that rather than one firm, two or more firms dominate the market. There is no precise upper limit to the number of firms in an oligopoly, but the number must be low enough that the actions of one firm significantly impact and influence the others.

1. Interdependence:

The foremost characteristic of oligopoly is interdependence of the various firms in the decision making.

This fact is recognized by all the firms in an oligopolistic industry. If a small number of sizeable firms constitute an industry and one of these firms starts advertising campaign on a big scale or designs a new model of the product which immediately captures the market, it will surely provoke countermoves on the part of rival firms in the industry.

Thus different firms are closely inter dependent on each other.

2. Advertising:

Under oligopoly a major policy change on the part of a firm is likely to have immediate effects on other firms in the industry. Therefore, the rival firms remain all the time vigilant about the moves of the firm which takes initiative and makes policy changes. Thus, advertising is a powerful instrument in the hands of an oligopolist. A firm under oligopoly can start an aggressive advertising campaign with the intention of capturing a large part of the market. Other firms in the industry will obviously resist its defensive advertising.

3. Group Behaviour:

In oligopoly, the most relevant aspect is the behaviour of the group. There can be two firms in the group, or three or five or even fifteen, but not a few hundred. Whatever the number, it is quite small so that each firm knows that its actions will have some effect on other firms in the group. In contrast, under perfect competition there are a large number of firms each attempting to maximise its profits.

4. Competition:

This leads to another feature of the oligopolistic market, the presence of competition. Since under oligopoly, there are a few sellers, a move by one seller immediately affects the rivals. So each seller is always on the alert and keeps a close watch over the moves of its rivals in order to have a counter-move.

5. Barriers to Entry of Firms:

As there is keen competition in an oligopolistic industry, there are no barriers to entry into or exit from it. However, in the long-run, there are some types of barriers to entry which tend to restrain new firms from entering the industry.

7. Existence of Price Rigidity:

In oligopoly situation, each firm has to stick to its price. If any firm tries to reduce its price, the rival firms will retaliate by a higher reduction in their prices. This will lead to a situation of price war which benefits none. On the other hand, if any firm increases its price with a view to increase its profits; the other rival firms will not follow the same. Hence, no firm would like to reduce the price or to increase the price. The price rigidity will take place.

8. No Unique Pattern of Pricing Behaviour:

The rivalry arising from interdependence among the oligopolists leads to two conflicting motives. Each wants to remain independent and to get the maxmium possible profit. Towards this end, they act and react on the price-output movements of one another which are a continuous element of uncertainty.

9. Indeterminateness of Demand Curve:

In market structures other than oligopolistic, demand curve faced by a firm is determinate. The interdependence of the oligopolists, however, makes it impossible to draw a demand curve for such sellers except for the situations where the form of interdependence is well defined. In real business operations, the demand curve remains indeterminate. Under oligopoly a firm can expect at least three different reactions of the other sellers when it lowers its prices.

Features of Monopilstic Competition

1. Large Number of Buyers and Sellers:

There are large number of firms but not as large as under perfect competition.

That means each firm can control its price-output policy to some extent. It is assumed that any price-output policy of a firm will not get reaction from other firms that means each firm follows the independent price policy.

If a firm reduces its price, the gains in sales will be slightly spread over many of its rivals so that the extent to which each of the rival firms suffers will be very small. Thus these rival firms will have no reason to react.

2. Free Entry and Exit of Firms:

Like perfect competition, under monopolistic competition also, the firms can enter or exit freely. The firms will enter when the existing firms are making super-normal profits. With the entry of new firms, the supply would increase which would reduce the price and hence the existing firms will be left only with normal profits. Similarly, if the existing firms are sustaining losses, some of the marginal firms will exit. It will reduce the supply due to which price would rise and the existing firms will be left only with normal profit.

3. Product Differentiation:

Another feature of the monopolistic competition is the product differentiation. Product differentiation refers to a situation when the buyers of the product differentiate the product with other. Basically, the products of different firms are not altogether different; they are slightly different from others. Although each firm producing differentiated product has the monopoly of its own product, yet he has to face the competition. This product differentiation may be real or imaginary. Real differences are like design, material used, skill etc. whereas imaginary differences are through advertising, trade mark and so on.

4. Selling Cost:

Another feature of the monopolistic competition is that every firm tries to promote its product by different types of expenditures. Advertisement is the most important constituent of the selling cost which affects demand as well as cost of the product. The main purpose of the monopolist is to earn maximum profits; therefore, he adjusts this type of expenditure accordingly.

5. Lack of Perfect Knowledge:

The buyers and sellers do not have perfect knowledge of the market. There are innumerable products each being a close substitute of the other. The buyers do not know about all these products, their qualities and prices.

Therefore, so many buyers purchase a product out of a few varieties which are offered for sale near the home. Sometimes a buyer knows about a particular commodity where it is available at low price. But he is unable to go there due to lack of time or he is too lethargic to go or he is unable to find proper conveyance. Likewise, the seller does not know the exact preference of buyers and is, therefore, unable to get advantage out of the situation.

7. More Elastic Demand:

Under monopolistic competition, demand curve is more elastic. In order to sell more, the firms must reduce its price.