Private Equity Venture Capital

🛑 👉🏻👉🏻👉🏻 INFORMATION AVAILABLE CLICK HERE👈🏻👈🏻👈🏻

Preqin uses cookies and other tracking technologies to assist with navigation and your ability to provide feedback, analyse your use of our products and services, assist with our promotional and marketing efforts, and provide content from third parties. By using our site, you consent to our use of cookies. Cookie Policy

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

Contact us with any questions or concerns at info@preqin.com or locate your nearest office.

What Do You Get With a Free Account?

High-level industry statistics, exclusive reports and publications.

Free users can:

Read the latest reports and market-level statistics covering fundraising, deals & exits, dry powder, AUM, and investors

Access alternative asset performance benchmarks

View our proprietary PrEQIn Indices

Download slide decks from our conference presentations

Private equity has been a form of investment for more than a century. Born out of the industrial revolution, private investments emerged as wealthy families contributed funds to building transportation. Over time, the asset class has expanded to encompass a vast array of investment types, now with trillions of dollars-worth of assets under management. In this lesson, we'll explore what constitutes a private investment, the story of its inception, strategies, and why investors choose to allocate funds to this sector.

Private equity is an asset class in which capital is invested in private companies in exchange for equity or ownership. Private companies are not publicly traded or listed on a stock exchange. Public companies can also be acquired by a private investor – in these circumstances, the public company becomes private and is de-listed. The industry currently has a total AUM of $4.11tn. In 2019, the average value of a buyout deal was $487mn.

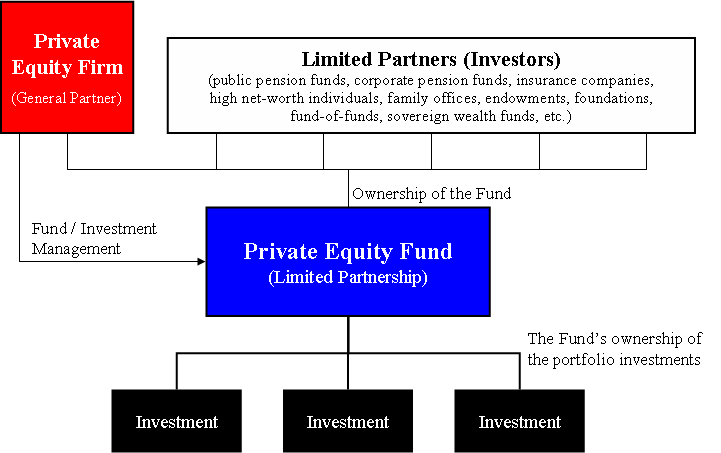

Private equity capital comes primarily from institutional and accredited investors that either invest directly in companies, or through funds managed by fund managers. In comparison to public equity investments, which trade daily, these are long-term and illiquid. Some of the most active investors are private equity fund of funds managers, pension funds, endowment plans, and family offices.

Definitions of private equity differ. In its broadest sense, the term can include niche strategies such as venture capital, real estate, infrastructure, and debt transactions - this is what Preqin would refer to as 'private capital.' For the purposes of this lesson, private equity specifically refers to investments made in companies, as opposed to hard assets such as real estate or infrastructure.

We touched on private equity in Lesson 2: What Is Private Capital?, exploring the early history of these investments. In this lesson, we dive deeper into the history of the asset class from its beginnings to the modern day.

Investments in private companies can be traced back to the dawn of the Industrial Revolution, when wealthy individuals and families contributed capital to railroads and other industrial companies.

Widely accepted as the first major buyout transaction, J. Pierpoint Morgan acquired Carnegie Steel Company for $480mn.

Founding of the first two venture capital firms: American Research and Development Corporation (ARDC) and J.H. Whitney & Company.

McLean Industries Inc. purchased Pan-Atlantic Steamship Company and Waterman Steamship Corporation, the first examples of leveraged buyout transactions.

The Small Business Investment Act passed, allowing the licensing of ‘Small Business Investment Companies’ (SBICs) to help the financing and management of small businesses in the US. The act gave venture capitalists access to federal funds which could be leveraged up to a ratio of 4:1 against privately raised investment funds.

The SBI Act resulted in the establishment of the first common form of private equity fund – a traditional pooled fund structure. Private equity firms could form limited partnerships to hold investments, with investment professionals acting as general partners.

The first ‘buyout boom’ era, a period characterized by large numbers of leveraged buyouts and hostile takeovers. Buyout activity accelerated due to the availability of high-yield debt financing, also known as ‘junk bonds.’ One of several high-profile disasters, the junk bond crash in 1989 led to restrictions on the industry to prevent riskier practices.

Private equity investors began to take a longer-term approach to companies acquired. During this period transactions typically utilized lower leverage levels in response to the excesses of the 1980s. The number of private equity investors also grew significantly, and in the early 1990s the Institutional Limited Partner Association (ILPA) was formed as a trade association for limited partners in private equity.

In the mid-to-late 1990s, venture capital activity grew, the internet rose to prominence and the dotcom bubble expanded. Companies like Amazon, AOL, eBay, Netscape, and Yahoo were all recipients of venture capital financing. This meant that private equity & venture capital firms were severely affected by the NASDAQ crash (2000) and the bursting of the internet bubble. Valuations for start-up technology companies collapsed and those leveraged buyout firms that had invested in telecommunications were also impacted.

As a result, global economic activity was slow at the turn of the century. The Federal Reserve looked to stimulate the American economy through a series of interest rate reductions.

The second ‘buyout boom’ came when low interest rates drove asset owners to private equity in search of yields. Lowered borrowing costs enabled private equity firms to finance larger acquisitions. The number of private equity deals soared and mega deals in excess of $20bn were made by Kinder Morgan, iHeartmedia, Hilton Worldwide Holdings, and First Data Corporation.

The collapse of Lehman Brothers heralded the Global Financial Crisis (GFC). Activity was depressed during this time as private equity firms had difficulty finding attractive investments and obtaining debt financing.

'The Third Boom’ arrived as financial markets started to recover. 2011 was the first year since the crash where the capital distributed back to asset owners surpassed capital being called up for investment. This was the result of a steep rise in exit activity as asset managers looked to exit the investments that they had held onto during the crisis. This trend accelerated and provided asset owners with huge amounts of liquidity, which in turn led to an unprecedented growth in fundraising from 2013 to present.

The enormous growth post-Global Financial Crisis has largely been driven by investor demand as a result of the high returns achieved by the asset class, with investments outperforming the public markets. This trend has continued in response to increasing global wealth concentration, with a rising class of very wealthy investors striving to access the high potential returns on offer.

Today the term private equity is very different to what it was 20 years ago. The traditional pooled fund structure is still widely used and accounts for most of the capital at work in the industry, but managers have evolved their offerings to cater to the changing needs of investors. Many investors are utilizing alternative methods of accessing the asset class such as direct investments, co-investments, and separately managed accounts. Meanwhile, some managers are moving away from the traditional commingled fund to more customized offerings and branching into new asset classes and strategies, such as private debt.

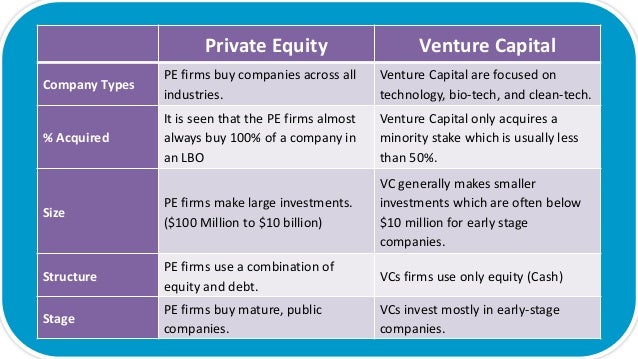

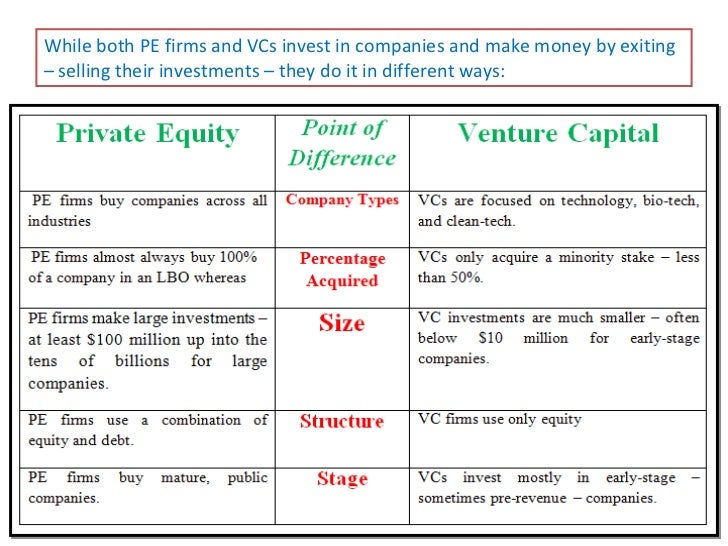

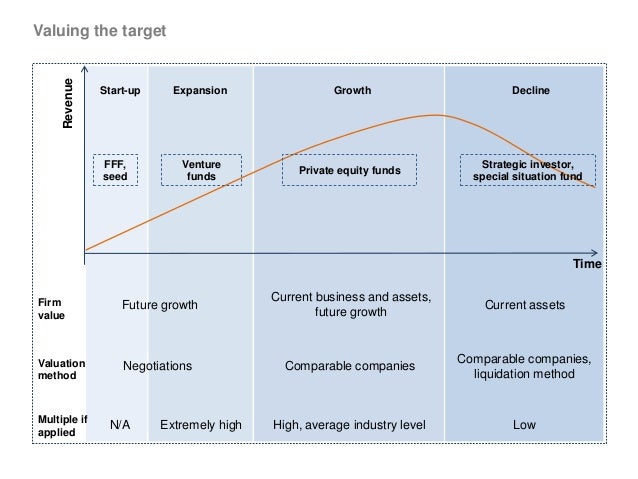

There are six key strategies and fund types for private equity investments – buyout, venture capital, growth capital, turnaround, fund of funds, and secondaries. Explore the drop-down for an overview of each strategy.

In a buyout investment, the investor often has complete or majority ownership and control of the company. Frequently, investors ‘shake up’ or replace the management teams and are relatively involved in operational decision-making. Buyout represents the largest strategy segment within private equity as measured by assets under management, and as such has an impact on the aggregated performance of private equity as an asset class.

The investor controls investments in the equities of mature private companies using a combination of equity and debt. Debt is utilized as it has a lower cost of capital than equity since interest payments reduce corporate tax liability, unlike dividend payments.

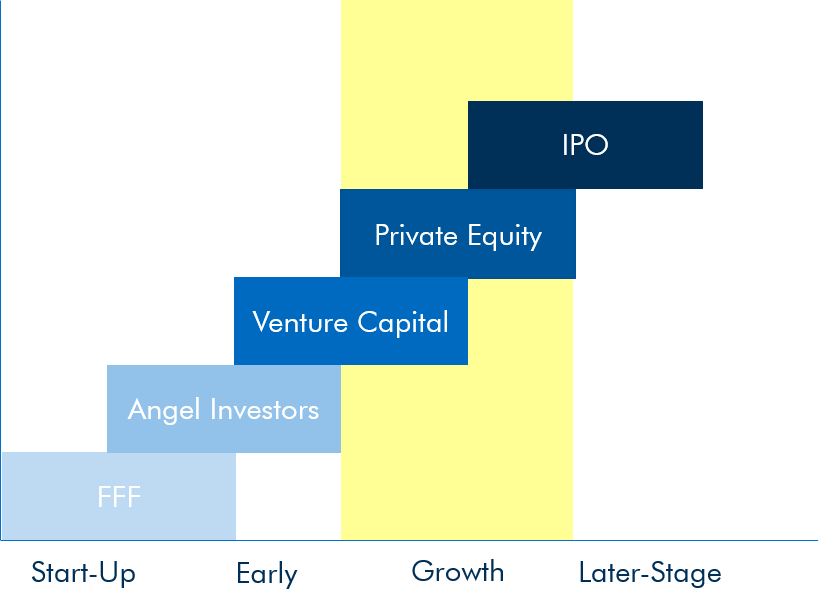

Investments made in start-up companies and early stage businesses that are believed to have significant growth potential. There are different stages of venture capital financing across angel, seed, late stage and expansion, which are reflective of a company’s maturity level. As a company grows, additional financing is provided in the form of ‘rounds’ to facilitate further development.

Growth capital can be seen as part of the venture capital strategy or its own strategy. For this type of strategy, investors take a minority or non-controlling stake in companies they believe will grow. In most circumstances, the investor has a passive approach and retains the same management team to oversee operations. The companies invested in are often relatively mature compared to venture capital, but less mature than the companies targeted in buyouts. The focus is more on market expansion as opposed to cost cutting or financial engineering. Typically, lower levels of leverage are used in growth capital than for buyout transactions.

This strategy targets companies with poor performance, or those experiencing trading difficulties. The basic concept is to buy cheap and sell high, with the difference between the depressed price at purchase and improvements at the time of sale creating a return on investment.

Funds of funds are vehicles raised by managers with a mandate to invest in the funds of other managers. The key value add for the investor is that they need only conduct a diligence process around the manager they have invested with. The fund manager will then proceed to source potential investments, carry out due diligence, and monitor the other managers holding the investors' capital.

However, there are higher fees and a smaller portion of profits go to the allocator, with less control over the underlying managers selected. This is a good option for allocators with small or inexperienced investment teams who would not be able to carry out the allocation process in-house.

This is a specialized fund type that looks to purchase other investors’ stakes in private equity funds. These funds will capture a portion of the anticipated growth in value of an investor's fund stake. Depending on when the fund stake is sold, the buyer may not obtain the full value of growth, as a percentage will have already gone to the original investor.

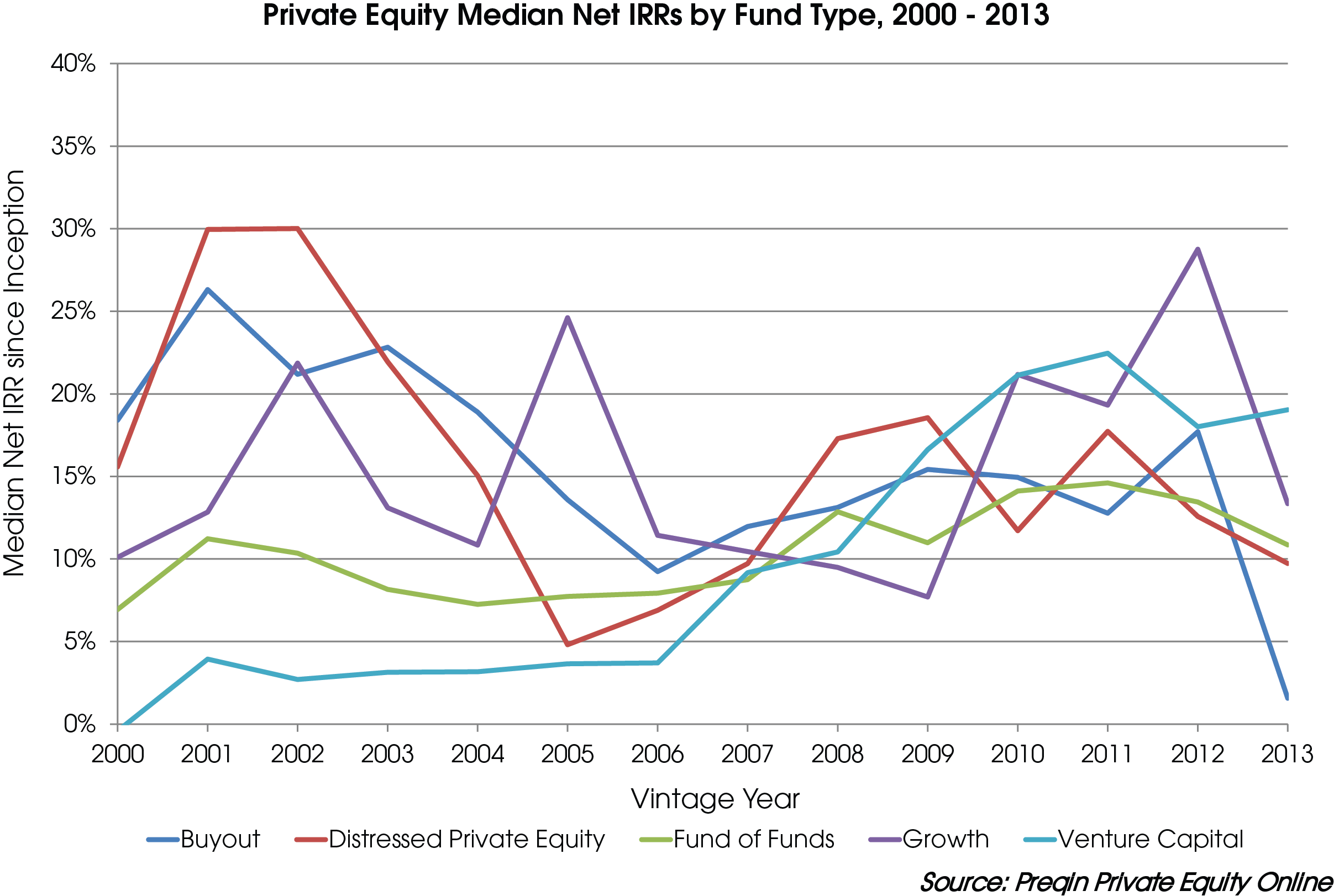

Buyout is the largest strategy segment within private equity as measured by assets under management. Therefore, it has a significant impact on the aggregated performance of the entire asset class. Buyout funds have generated strong and steady returns in recent years, driving much of the cash distribution seen in the private equity industry and contributing to investors’ positive view of the asset class. Smaller buyout funds often post the highest returns, as at purchase they are lower in price and worth significantly more by time of sale. Larger buyout transactions also present opportunities for strong returns, as companies restructure with the aim of improving operations and finances.

Venture capital has one of the highest potential rates of return, particularly for early stage investments. However, the success rate of early-stage companies is highly variable, with some experiencing phenomenal growth and others failing altogether. This creates a wide variation in outcomes for investors in the strategy: less than 20% of venture capital investments deliver positive returns. Later-stage venture capital investments carry lower risk as they are further along in their development, but this makes the potential returns lower too.

Growth capital and turnaround investments also carry a reasonable amount of risk as they rely on growth or improvements in company performance actually being achieved. The returns for growth investments are not as high as buyout transactions due to the non-controlling stakes often taken, whereas in turnaround investments investors tend to buy low and sell high, therefore reaping higher returns.

Investments in fund of funds and secondaries tend to carry the lowest risk. In secondaries funds, risk is minimized as investors already have an indication of performance. In funds of funds, this is because investments are diversified across multiple funds. However, the double layer of fees puts funds of funds at the lower end of the return spectrum.

Private equity is a well-established part of many institutional investor portfolios, as it generates higher absolute returns while also improving portfolio diversification.

In this lesson, we revealed more about the private equity asset class. From its history to the investment strategies available and the risk/return profile, you now know the reasons why investors choose to allocate funds to private equity.

Before addressing venture capital vs private equity, it is necessary to pay some attention to the concept of venture capital investment. In the next step, the difference between the two is defined by the definition of private equity.

Venture capital is a high-risk investment that is usually made on startups. In this article, a startup is a new, technology-based and scalable business. Because of the potential risks to success and the very low probability of great success for startups, the investor at different stages of a startup’s development is called risky or venture.

On the other hand, the amount needed by startups to grow and scale are enormous. For this reason, venture capitalists are usually legal entities; a company or a fund. They raise their available capital from a range of wealthy individuals and entities. The following are some of the examples: pension funds, banks and insurance companies, charities and academia, corporations, etc. The return on this investment can range from absolute zero to 100,000%.

Private markets, compared to the public market, is one of the large and complex financial spaces. It is divided into two sub-categories:

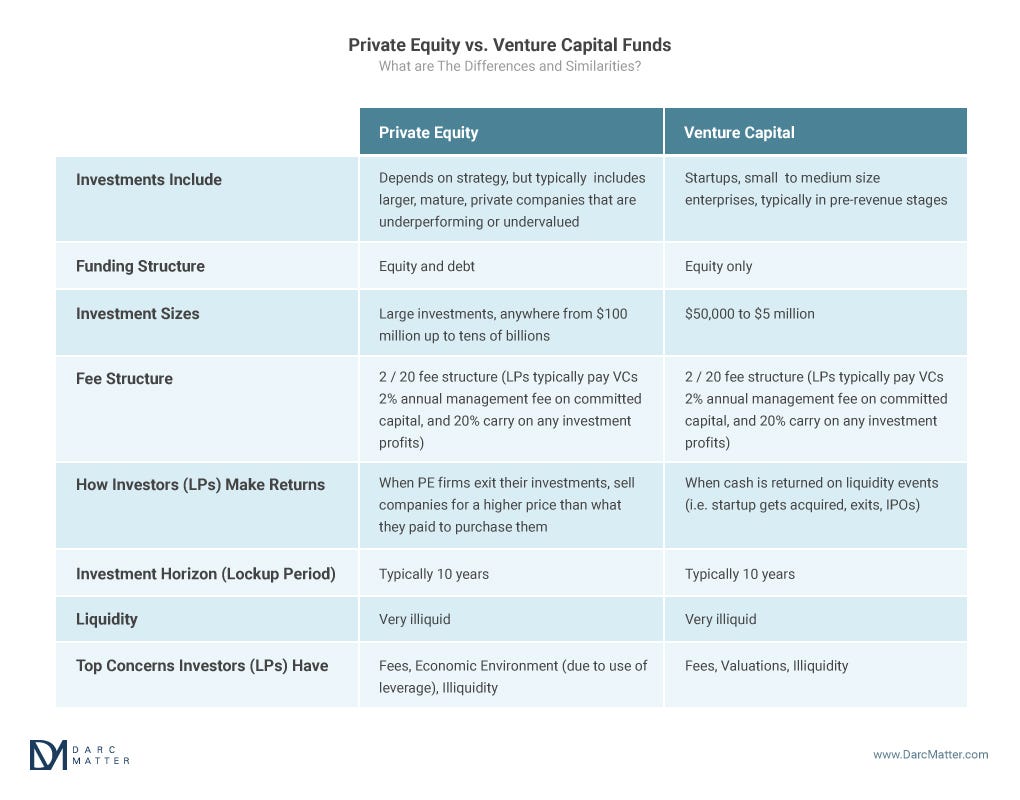

Private equity (PE), like venture capital (VC), provides the money needed for a startup. PE buys the company’s stock in return. These funds raise their required capital from limited partners (LPs).

Unlike venture capital (VC), Private Equity (PE) usually buys 50% or more of the company’s stock. That’s why PE runs a higher risk. These companies typically have a significant stake in several companies at the same time.

Similarities between private equity and venture capital

However, you can see some differences between the two:

In addition, each one invests in a different stage of the corporate life cycle.

To be a little more specific, private equity typically buys half or more of the stock. These funds usually invest in mature companies that are collapsing due to problems. Their assumption in this investment is that the business will continue to be profitable if the issues are solved.

In contrast to private equity, venture capital usually invests the companies in the seed or early stages. VC provides the money needed for their growth. These funds typically buy less than 50 per cent of the capital.

However, this process is changing. In recent years, we have seen private equities invest in companies that have previously been provided by venture capital.

Now that we know the differences and similarities between private equity and venture capital, we will talk more about the impact of startups as well as venture capital-related issues in the following parts. In the next articles, we will deal with private equity.

The results of extensive studies since the 1980s show a positive relationship between startups and the macroeconomic growth of each country. These results are because of the higher average growth rate of startups compared to large and mature companies.

In general, orienting towards technology and knowledge-based activities is one of the competitive advantages of developed economies.

Startups innovate in value creation to rebuild existing industry boundaries or create new ones. In addition, they help increase the dynamism, employment, national income, citizenship welfare, and the broader formation of similar economic activities in society.

The importance of knowledge-based entrepreneurial activities is critical in overall growth. It is so essential that one of the reasons for the superiority of the American economy is the mature and always dynamic entrepreneurial ecosystem in this country.

Just look at the number of startups in this country since 2006. Interestingly, most of them are set up by MIT alumni. There are more than 25,000 businesses so far. These startups have created jobs for more than 3 million people to date and have combined annual revenue of $ 2 trillion. To bring it to light, this figure is equivalent to the gross domestic product of the eighth largest economy in the world! In addition, an average of 900 startups is started annually by this university’s graduates.

However, the story of all startups begins with an idea, the idea that has the potential to grow into a new solution to meet the hidden needs of the customer. In addition, some startup ideas offer unique solutions to meet the old demands of the customer.

A startup needs many financial resources to attract capable human capital, turn an idea into a product, introduce a product to the target market, conquer the target market, grow and scale, and ultimately achieve industry excellence. The average capital raised by US technology-driven startups at various stages of development before the first IPO is $ 239 million.

In fact, if we consider a startup as a new, technology-driven and scalable business, it is not possible to make a change in the industry without the help of venture capitalists or private equity at different stages of growth and scale.

Therefore, the need for an efficient market, at least consisting of venture capitalists, is crucial to providing the startups’ monetary capital. In addition, there are investments such as credit, relationships, operational and strategic consulting, as well as management experience and skills. The

Hairy Mom Masturbation Web

Sex Damashni Skriti Kamera

Young Teens Anal First Time

Two Russian Teens

12 Qizlar Sex

Private Equity vs. Venture Capital: Understanding the ...

Private Equity & Venture Capital | Preqin

Venture Capital vs Private Equity: What Is Venture Capital ...

Private equity vs. venture capital: What’s the difference ...

Private Equity and Venture Capital | Coursera

Private Equity / Venture Capital – Assisting financial ...

Brand Capital Ventures - Private Equity Venture Capital

Private Equity Venture Capital